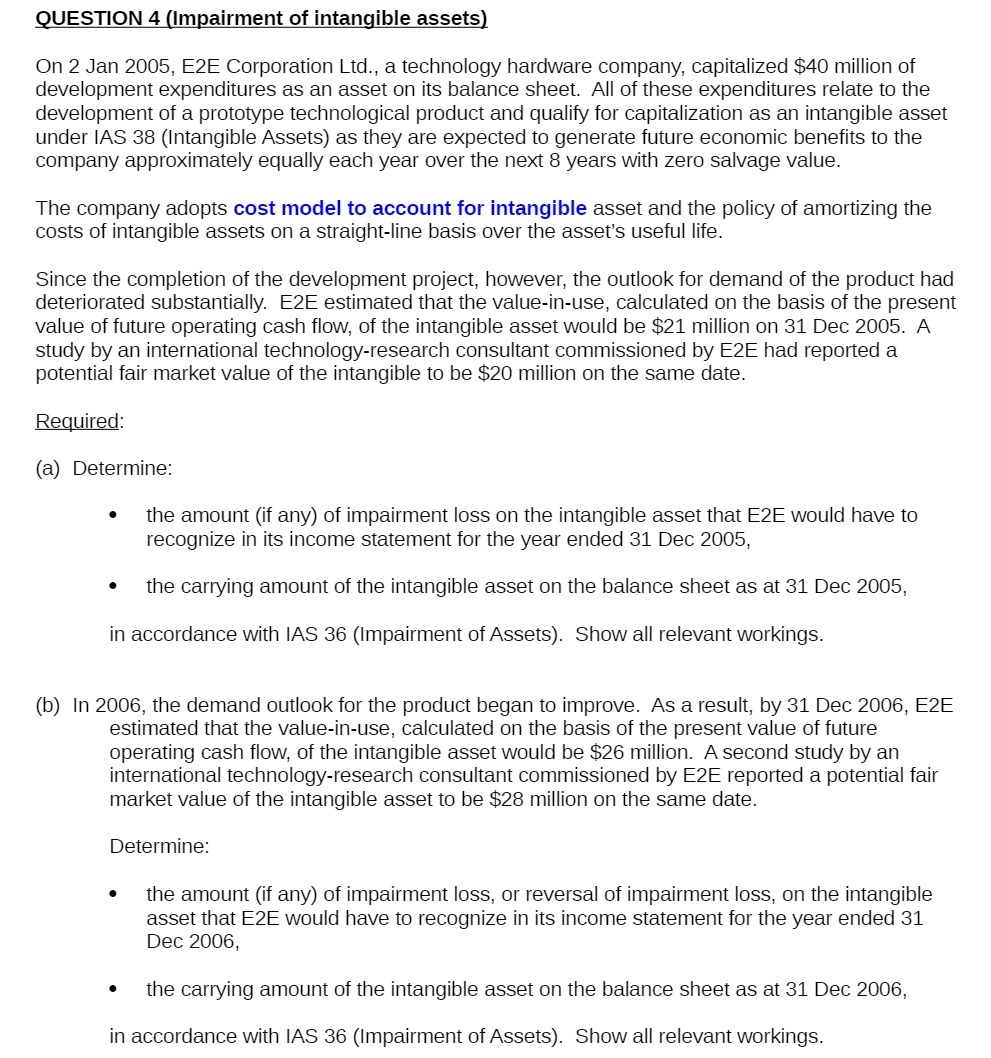

QUES'HON 4 {Impairment of intangible assets) On 2 Jan 2005, E2E Corporation Ltd., a technology hardware company, capitalized $40 million of development expenditures as an

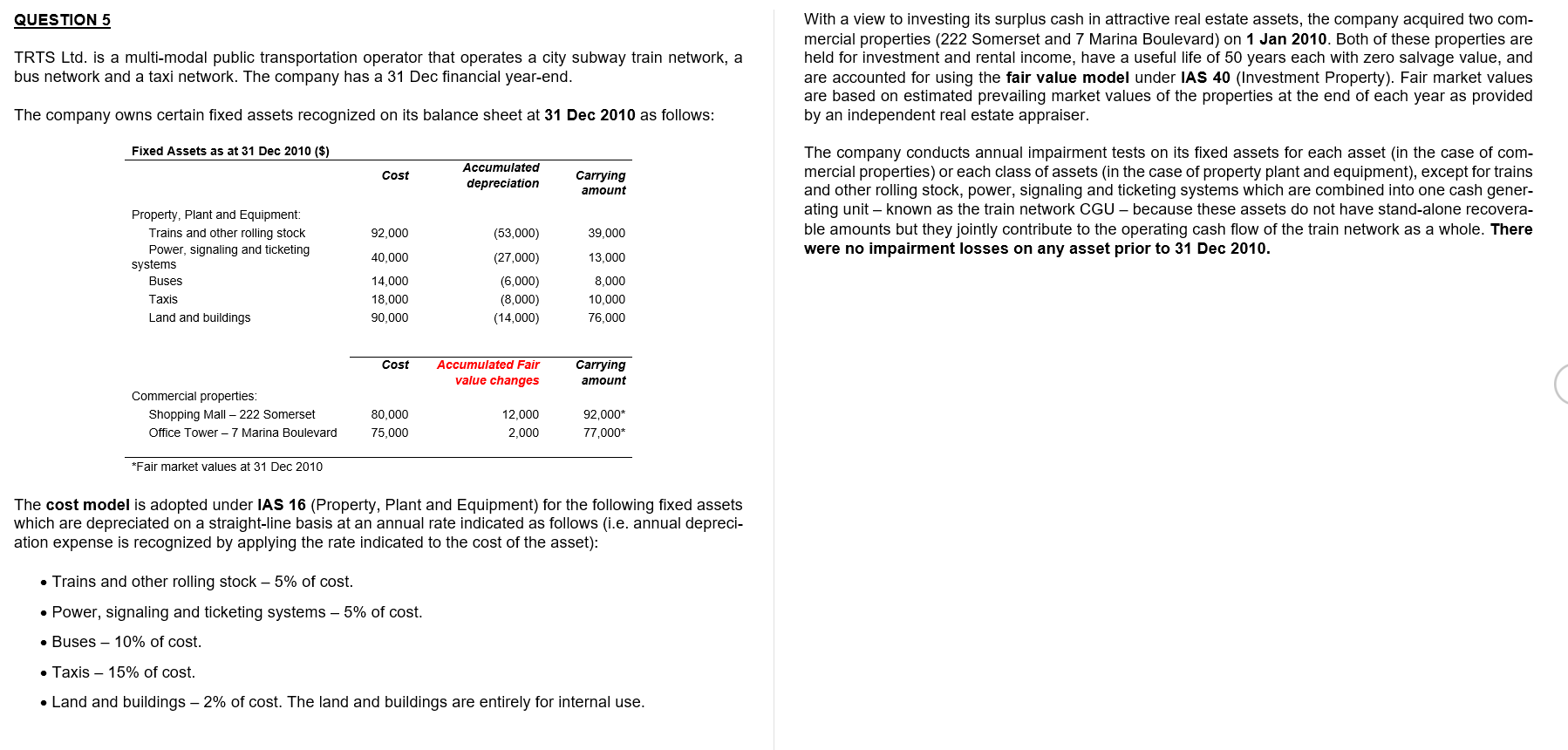

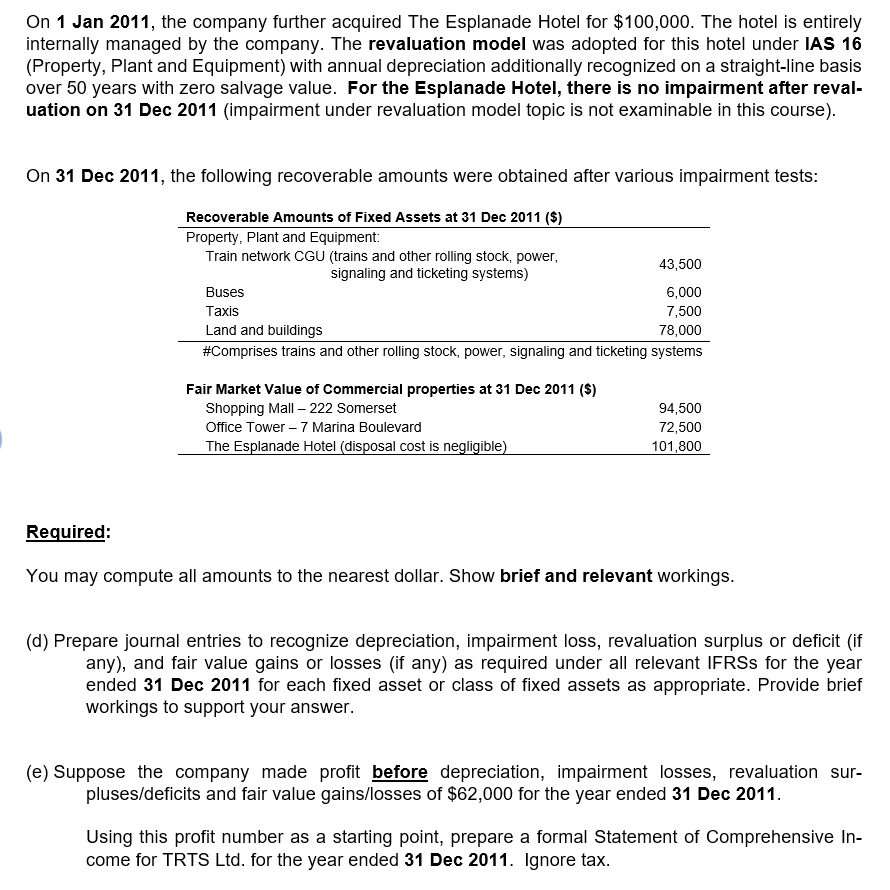

QUES'HON 4 {Impairment of intangible assets) On 2 Jan 2005, E2E Corporation Ltd., a technology hardware company, capitalized $40 million of development expenditures as an asset on its balance sheet. All of these expenditures relate to the development of a prototype technological product and qualify for capitalization as an intangible asset under EAS 38 (Intangible Assets) as they are expected to generate future economic benefits to the company approximately equally each year over the next 8 years with zero salvage value. The company adopts cost model to account for intangible asset and the policy of amortizing the costs of intangible assets on a straight-line basis over the asset's useful life. Since the completion of the development project, however, the outlook for demand of the product had deteriorated substantially. E2E estimated that the value-inuse, calculated on the basis of the present value of future operating cash flow, of the intangible assetwould be $21 million on 31 Dec 2005. A study by an international technology-research consultant commissioned by E2E had reported a potential fair market value of the intangible to be $20 million on the same date. Required: (a) Determine: 0 the amount (if any) of impairment loss on the intangible asset that E2E would have to recognize in its income statement for the year ended 31 Dec 2005, ' the carrying amount of the intangible asset on the balance sheet as at 31 Dec 2005, in accordance with IAS 36 (Impairment of Assets). Show all relevant workings. (b) In 2006, the demand outlook for the product began to improve. As a result, by 31 Dec 2006, E2E estimated that the vaiue-in-use, calculated on the basis of the present value of future operating cash flow, of the intangible asset would be $26 million. A second study by an international technology-research consultant commissioned by E2E reported a potential fair market value of the intangible asset to be $28 million on the same date. Determine: ' the amount (if any) of impairment loss, or reversal of impairment loss, on the intangible asset that E2E would have to recognize in its income statement for the year ended 31 Dec 2006, 0 the carrying amount of the intangible asset on the balance sheet as at 31 Dec 2006, in accordance with IAS 36 (Impairment of Assets). Show all relevant workings. QUESTION 5 With a view to investing its surplus cash in attractive real estate assets, the company acquired two com- mercial properties (222 Somerset and 7 Marina Boulevard) on 1 Jan 2010. Both of these properties are TRTS Ltd. is a multi-modal public transportation operator that operates a city subway train network, a held for investment and rental income, have a useful life of 50 years each with zero salvage value, and bus network and a taxi network. The company has a 31 Dec financial year-end. are accounted for using the fair value model under IAS 40 (Investment Property). Fair market values are based on estimated prevailing market values of the properties at the end of each year as provided The company owns certain fixed assets recognized on its balance sheet at 31 Dec 2010 as follows: by an independent real estate appraiser. Fixed Assets as at 31 Dec 2010 ($) The company conducts annual impairment tests on its fixed assets for each asset (in the case of com- Cost Accumulated mercial properties) or each class of assets (in the case of property plant and equipment), except for trains depreciation Carrying amount and other rolling stock, power, signaling and ticketing systems which are combined into one cash gener- Property, Plant and Equipment: ating unit - known as the train network CGU - because these assets do not have stand-alone recovera- Trains and other rolling stock 92,000 (53,000) 39,000 ble amounts but they jointly contribute to the operating cash flow of the train network as a whole. There Power, signaling and ticketing systems 40,000 (27,000) 13,000 were no impairment losses on any asset prior to 31 Dec 2010. Buses 14,000 (6,000) 8.000 Taxis 18,000 (8,000) 10,000 Land and buildings 90,000 (14,000) 76,000 Cost Accumulated Fair Carrying value changes amount Commercial properties: Shopping Mall - 222 Somerset 80,000 12,000 92,000* Office Tower - 7 Marina Boulevard 75,000 2,000 77,000* *Fair market values at 31 Dec 2010 The cost model is adopted under IAS 16 (Property, Plant and Equipment) for the following fixed assets which are depreciated on a straight-line basis at an annual rate indicated as follows (i.e. annual depreci- ation expense is recognized by applying the rate indicated to the cost of the asset): . Trains and other rolling stock - 5% of cost. . Power, signaling and ticketing systems - 5% of cost. . Buses - 10% of cost. . Taxis - 15% of cost. . Land and buildings - 2% of cost. The land and buildings are entirely for internal use.0n 1 Jan 2011, the company further acquired The Esplanade Hotel for $100,000. The hotel is entirely internally managed by the company. The revaluation model was adopted for this hotel under IAS 16 (Property, Plant and Equipment) with annual depreciation additionally recognized on a straight-line basis over 50 years with zero salvage value. For the Esplanade Hotel, there is no impairment after reval- uation on 31 Dec 2011 (impairment under revaluation model topic is not examinable in this course}. On 31 Dec 2011, the following recoverable amounts were obtained after various impairment tests: Recoverable Amounts of Fixed Assets at 31 Dec 2011 [3} Property, Plant and Equipment: Train network CGU {trains and other rolling stock, power, signaling and ticketing systems) 43'500 Buses 6,000 Taxis 7,500 Land and buildings ?3,DUU #Comprises trains and other rolling stock, power, signaling and ticketing systems Fair Market Value of Commercial properties at 31 Dec 2011 (5] shopping Mall 22 Somerset 94,500 Ofce Tower 7 Marina Boulevard 72,500 The Esplanade Hotel gdisgosal cost is negligible} 101,300 Reguired: You may compute all amounts to the nearest dollar. Show brief and relevant workings. (d) Prepare journal entries to recognize depreciation, impairment loss, revaluation surplus or deficit (if any), and fair value gains or losses (if any) as required under all relevant lFRSs for the year ended 31 Dec 2011 for each fixed asset or class of xed assets as appropriate. Provide brief workings to support your answer. (e) Suppose the company made prot before depreciation, impairment losses, revaluation sur- plusesideficits and fair value gainsl'losses of $62,000 for the year ended 31 Dec 2011. Using this profit number as a starting point, prepare a formal Statement of Comprehensive In- come for TRTS Ltd. for the year ended 31 Dec 2011. Ignore tax

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance