Answered step by step

Verified Expert Solution

Question

1 Approved Answer

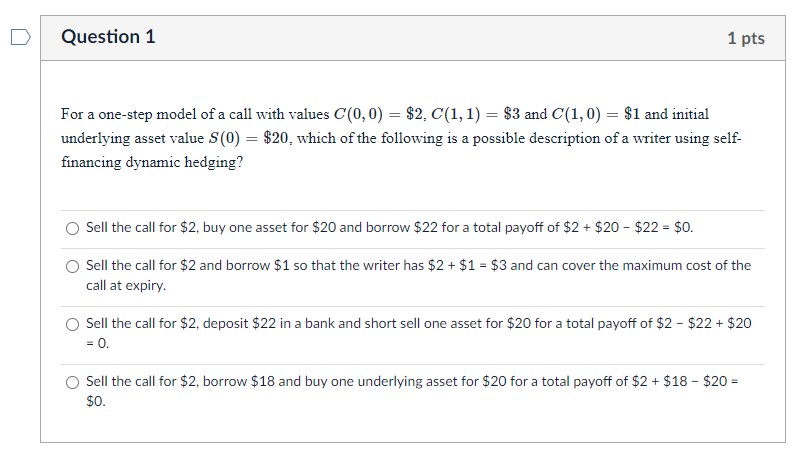

Question 1 1 pts For a one-step model of a call with values c(0,0) = $2. C(1,1)= $3 and C(1,0) = $1 and initial underlying

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Good Financial Advisor Will Tell You Everything You Need To Know About Retirement Generating Lifetime Income And Planning Your Legacy

Authors: Jeremy A. Kisner CFP, Robert J. Luna CIMA

1st Edition

1935586491, 978-1935586494