Answered step by step

Verified Expert Solution

Question

1 Approved Answer

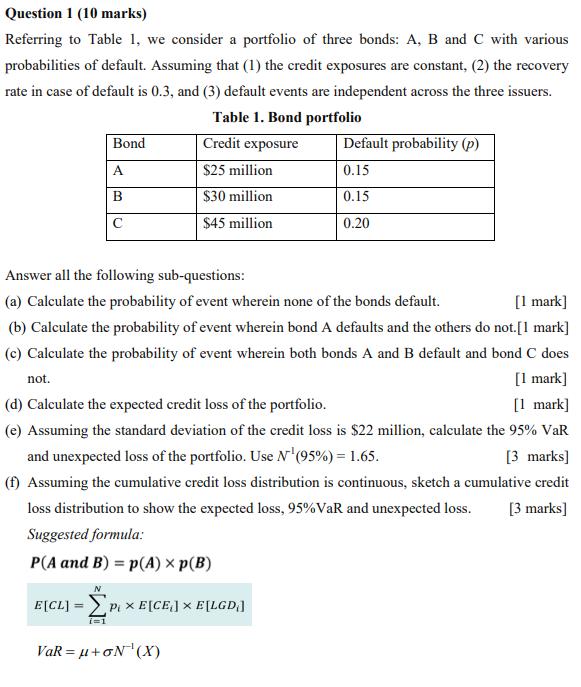

Question 1 (10 marks) Referring to Table 1, we consider a portfolio of three bonds: A, B and C with various probabilities of default.

Question 1 (10 marks) Referring to Table 1, we consider a portfolio of three bonds: A, B and C with various probabilities of default. Assuming that (1) the credit exposures are constant, (2) the recovery rate in case of default is 0.3, and (3) default events are independent across the three issuers. Table 1. Bond portfolio Credit exposure $25 million $30 million $45 million Bond A B C Answer all the following sub-questions: (a) Calculate the probability of event wherein none of the bonds default. [1 mark] (b) Calculate the probability of event wherein bond A defaults and the others do not.[1 mark] (c) Calculate the probability of event wherein both bonds A and B default and bond C does not. [1 mark] [1 mark] (d) Calculate the expected credit loss of the portfolio. (e) Assuming the standard deviation of the credit loss is $22 million, calculate the 95% VaR and unexpected loss of the portfolio. Use N (95%) = 1.65. [3 marks] (f) Assuming the cumulative credit loss distribution is continuous, sketch a cumulative credit loss distribution to show the expected loss, 95% VaR and unexpected loss. [3 marks] Suggested formula: P(A and B) = P(A) > p(B) E[CL] = P x E[CE] E[LGD}] i=1 Default probability (p) 0.15 0.15 0.20 VaR=u+oN'(X)

Step by Step Solution

★★★★★

3.37 Rating (153 Votes )

There are 3 Steps involved in it

Step: 1

a To calculate the probability of none of the bonds defaulting we need to find the complement of the event where at least one bond defaults Since the default events are independent we can calculate th...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Business Statistics In Practice

Authors: Bruce Bowerman, Richard O'Connell

6th Edition

0073401838, 978-0073401836