Answered step by step

Verified Expert Solution

Question

1 Approved Answer

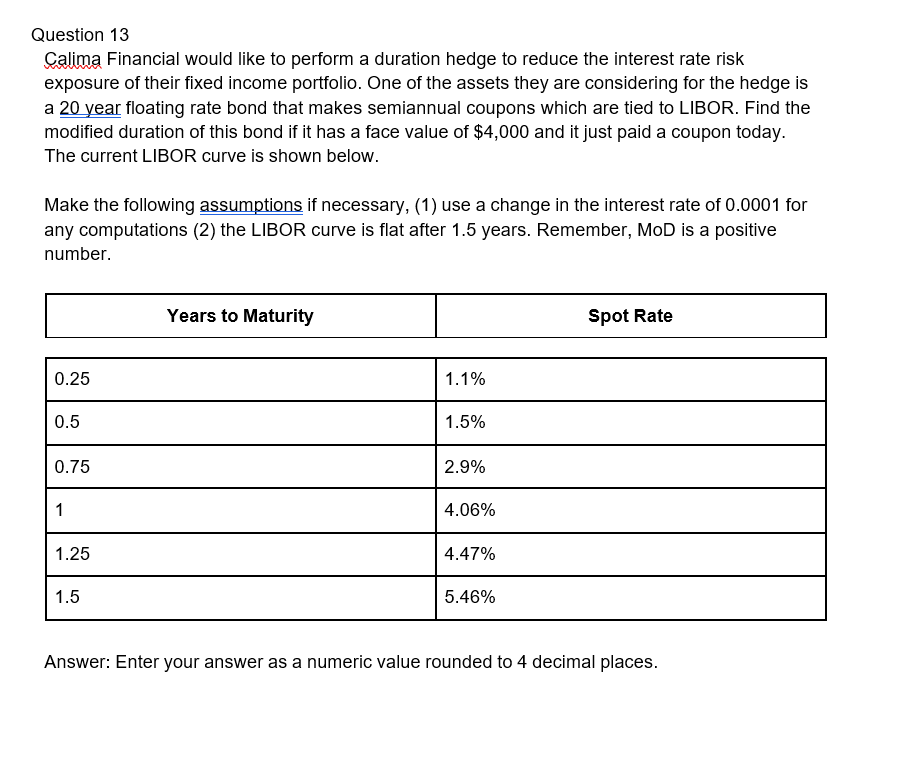

Question 1 3 Calima Financial would like to perform a duration hedge to reduce the interest rate risk exposure of their fixed income portfolio. One

Question

Calima Financial would like to perform a duration hedge to reduce the interest rate risk exposure of their fixed income portfolio. One of the assets they are considering for the hedge is a year floating rate bond that makes semiannual coupons which are tied to LIBOR. Find the modified duration of this bond if it has a face value of $ and it just paid a coupon today. The current LIBOR curve is shown below.

Make the following assumptions if necessary, use a change in the interest rate of for any computations the LIBOR curve is flat after years. Remember, MoD is a positive number.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Wall Street Journal Complete Personal Finance Guidebook

Authors: Jeff D. Opdyke

1st Edition

030733600X, 978-0274804573