Answered step by step

Verified Expert Solution

Question

1 Approved Answer

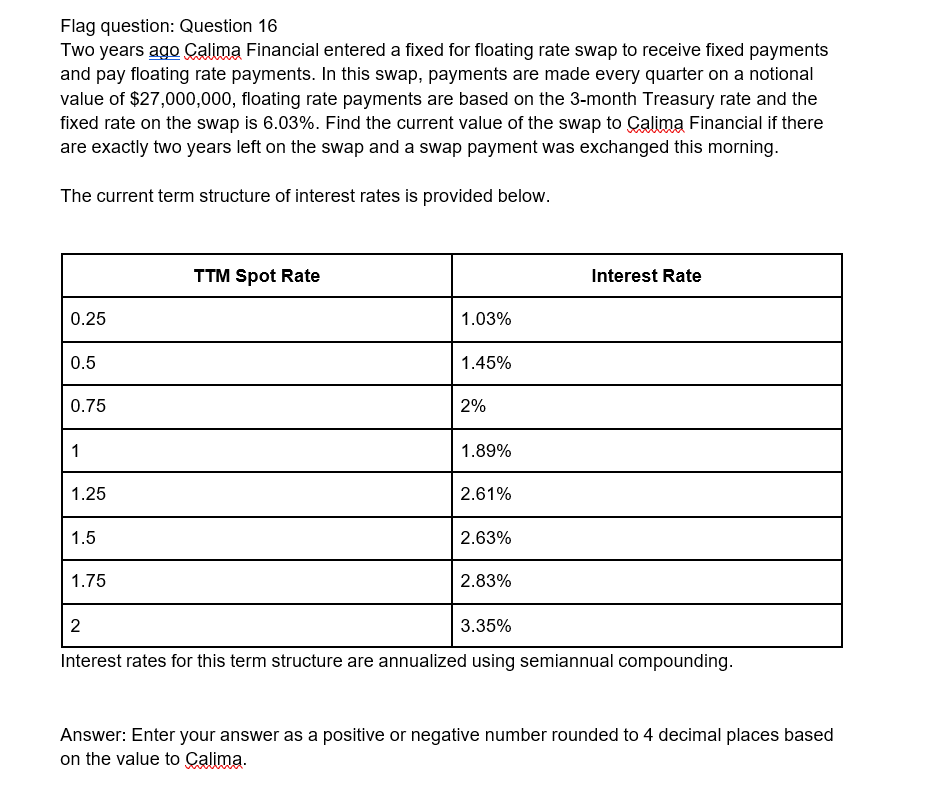

Question 1 6 Two years ago Calima Financial entered a fixed for floating rate swap to receive fixed payments and pay floating rate payments. In

Question

Two years ago Calima Financial entered a fixed for floating rate swap to receive fixed payments and pay floating rate payments. In this swap, payments are made every quarter on a notional value of $ floating rate payments are based on the month Treasury rate and the fixed rate on the swap is Find the current value of the swap to Calima Financial if there are exactly two years left on the swap and a swap payment was exchanged this morning.

The current term structure of interest rates is provided below.

tableTTM Spot Rate,Interest Rate

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of The Equity Risk Premium

Authors: Rajnish Mehra

1st Edition

0444508996, 978-0444508997