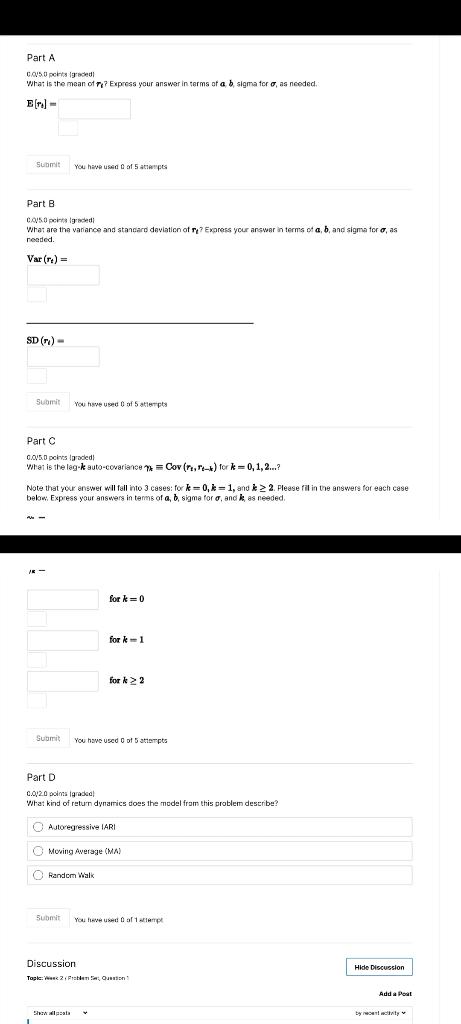

Question 1 A Bookmark this page Homework due Jul 28, 2021 16:00 WAT Suppose the daily returns on a stock are generated by a stationary process defined by the time series model: rt = + at-1 +b where a and b are constants, and the "innovations" t are uncorrelated across time with E [et] = 0 E [64s] = o? 8ts where Ots = 1 ift=s 0 ift+s where o >0. Part A CO50 points graded What is the mean of 77 Express your answer in terms of a b sigma toro, as needed. (1) - Submit You have used of 5 tips Part B COS. What are the variance and standard deviation of r? Express your arswar in terms of a, b, and sigma fora, as needed Var(:) = SD (1) - Suomi You have used of attempts Part C GOV.D portsgraded What is the lag k auto-covariano Cov (n.1-x) for k= 0,1,2...? Note that your answer will fall into 3 cases: for k=0, k = 1, and k > 2. Please fill in the answers for each case below: Express your answers in terms of a, b, sigma fora, and k as needed for k=0 for ki for k> 2 Suomi You have used of attempts Part D C.02.0 points graded What kind of retur dynamics does model from this problem describe? Autoregressive IARI Moving Average (MM Random Walk Submit You have used 0 al 1 lamp Discussion Topic: Week 2 Hide Discussion = Add a Pout Show lata tyret Question 1 A Bookmark this page Homework due Jul 28, 2021 16:00 WAT Suppose the daily returns on a stock are generated by a stationary process defined by the time series model: rt = + at-1 +b where a and b are constants, and the "innovations" t are uncorrelated across time with E [et] = 0 E [64s] = o? 8ts where Ots = 1 ift=s 0 ift+s where o >0. Part A CO50 points graded What is the mean of 77 Express your answer in terms of a b sigma toro, as needed. (1) - Submit You have used of 5 tips Part B COS. What are the variance and standard deviation of r? Express your arswar in terms of a, b, and sigma fora, as needed Var(:) = SD (1) - Suomi You have used of attempts Part C GOV.D portsgraded What is the lag k auto-covariano Cov (n.1-x) for k= 0,1,2...? Note that your answer will fall into 3 cases: for k=0, k = 1, and k > 2. Please fill in the answers for each case below: Express your answers in terms of a, b, sigma fora, and k as needed for k=0 for ki for k> 2 Suomi You have used of attempts Part D C.02.0 points graded What kind of retur dynamics does model from this problem describe? Autoregressive IARI Moving Average (MM Random Walk Submit You have used 0 al 1 lamp Discussion Topic: Week 2 Hide Discussion = Add a Pout Show lata tyret