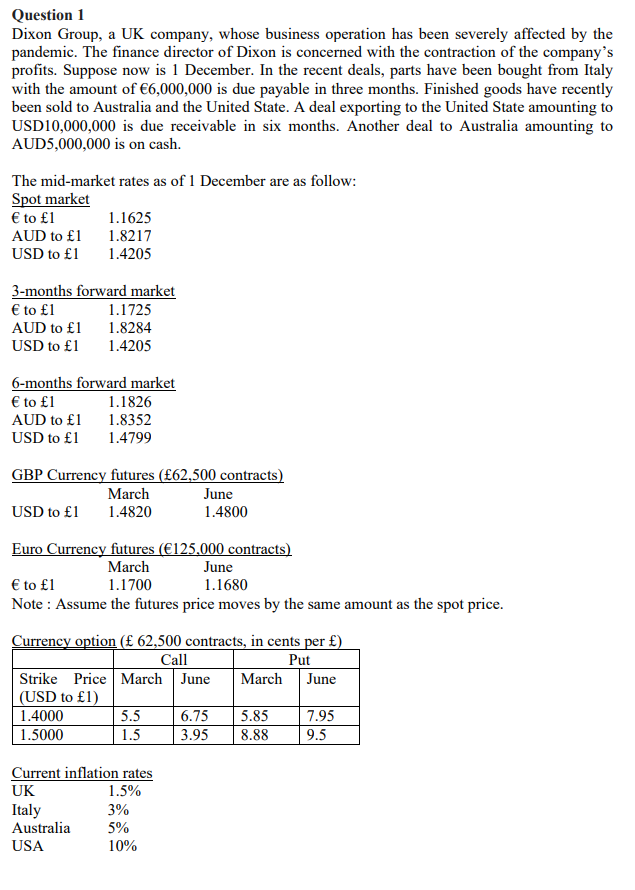

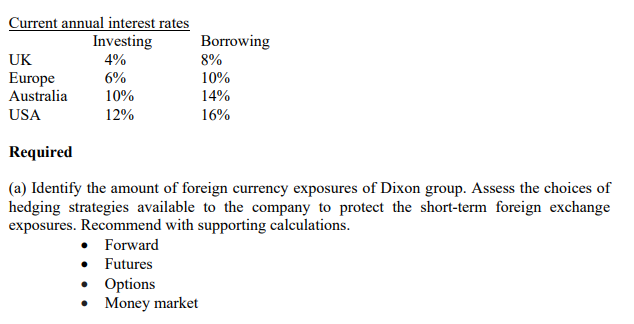

Question 1 Dixon Group, a UK company, whose business operation has been severely affected by the pandemic. The finance director of Dixon is concerned with the contraction of the company's profits. Suppose now is 1 December. In the recent deals, parts have been bought from Italy with the amount of 6,000,000 is due payable in three months. Finished goods have recently been sold to Australia and the United State. A deal exporting to the United State amounting to USD10,000,000 is due receivable in six months. Another deal to Australia amounting to AUD5,000,000 is on cash. The mid-market rates as of 1 December are as follow: Spot market to 1 1.1625 AUD to 1 1.8217 USD to 1 1.4205 3-months forward market to 1 1.1725 AUD to 1 1.8284 USD to 1 1.4205 6-months forward market to 1 1.1826 AUD to 1 1.8352 USD to 1 1.4799 GBP Currency futures (62,500 contracts) March June USD to 1 1.4820 1.4800 Euro Currency futures (125,000 contracts) March June to 1 1.1700 1.1680 Note : Assume the futures price moves by the same amount as the spot price. Currency option ( 62,500 contracts, in cents per ) Call Put Strike Price March June March June (USD to 1) 1.4000 5.5 6.75 5.85 7.95 1.5000 1.5 3.95 8.88 9.5 Current inflation rates UK 1.5% Italy 3% Australia 5% USA 10% Current annual interest rates Investing UK 4% Europe 6% Australia 10% USA 12% Borrowing 8% 10% 14% 16% Required (a) Identify the amount of foreign currency exposures of Dixon group. Assess the choices of hedging strategies available to the company to protect the short-term foreign exchange exposures. Recommend with supporting calculations. Forward Futures Options Money market Question 1 Dixon Group, a UK company, whose business operation has been severely affected by the pandemic. The finance director of Dixon is concerned with the contraction of the company's profits. Suppose now is 1 December. In the recent deals, parts have been bought from Italy with the amount of 6,000,000 is due payable in three months. Finished goods have recently been sold to Australia and the United State. A deal exporting to the United State amounting to USD10,000,000 is due receivable in six months. Another deal to Australia amounting to AUD5,000,000 is on cash. The mid-market rates as of 1 December are as follow: Spot market to 1 1.1625 AUD to 1 1.8217 USD to 1 1.4205 3-months forward market to 1 1.1725 AUD to 1 1.8284 USD to 1 1.4205 6-months forward market to 1 1.1826 AUD to 1 1.8352 USD to 1 1.4799 GBP Currency futures (62,500 contracts) March June USD to 1 1.4820 1.4800 Euro Currency futures (125,000 contracts) March June to 1 1.1700 1.1680 Note : Assume the futures price moves by the same amount as the spot price. Currency option ( 62,500 contracts, in cents per ) Call Put Strike Price March June March June (USD to 1) 1.4000 5.5 6.75 5.85 7.95 1.5000 1.5 3.95 8.88 9.5 Current inflation rates UK 1.5% Italy 3% Australia 5% USA 10% Current annual interest rates Investing UK 4% Europe 6% Australia 10% USA 12% Borrowing 8% 10% 14% 16% Required (a) Identify the amount of foreign currency exposures of Dixon group. Assess the choices of hedging strategies available to the company to protect the short-term foreign exchange exposures. Recommend with supporting calculations. Forward Futures Options Money market