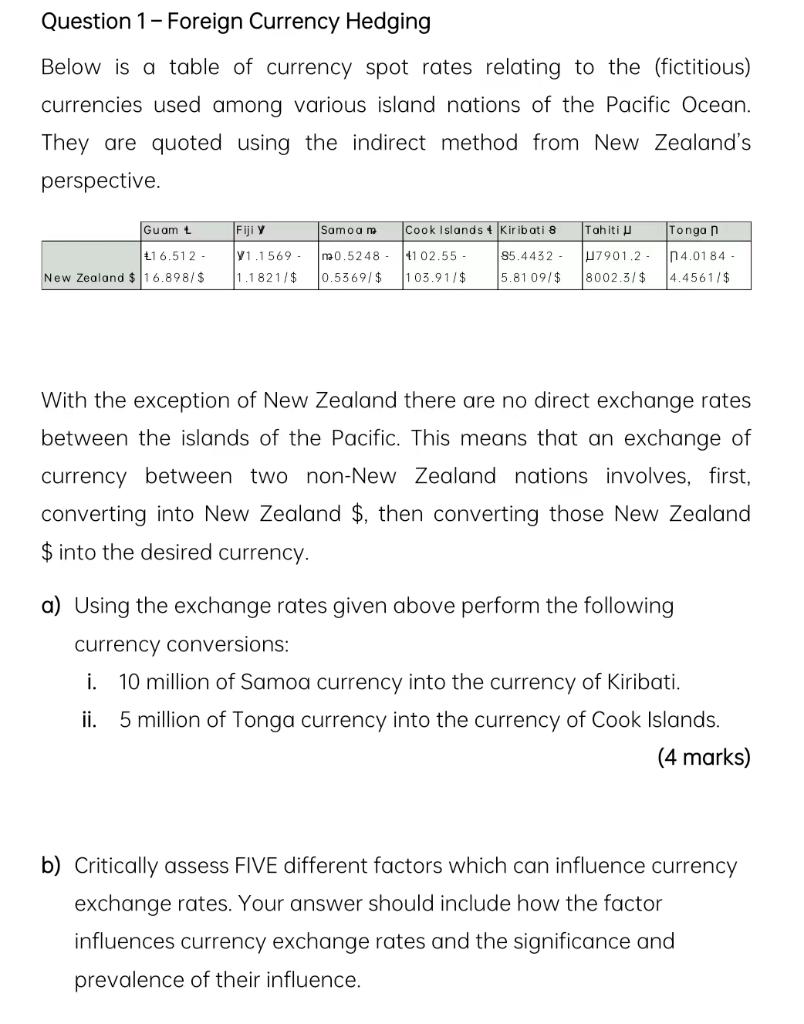

Question: Question 1- Foreign Currency Hedging Below is a table of currency spot rates relating to the (fictitious) currencies used among various island nations of the

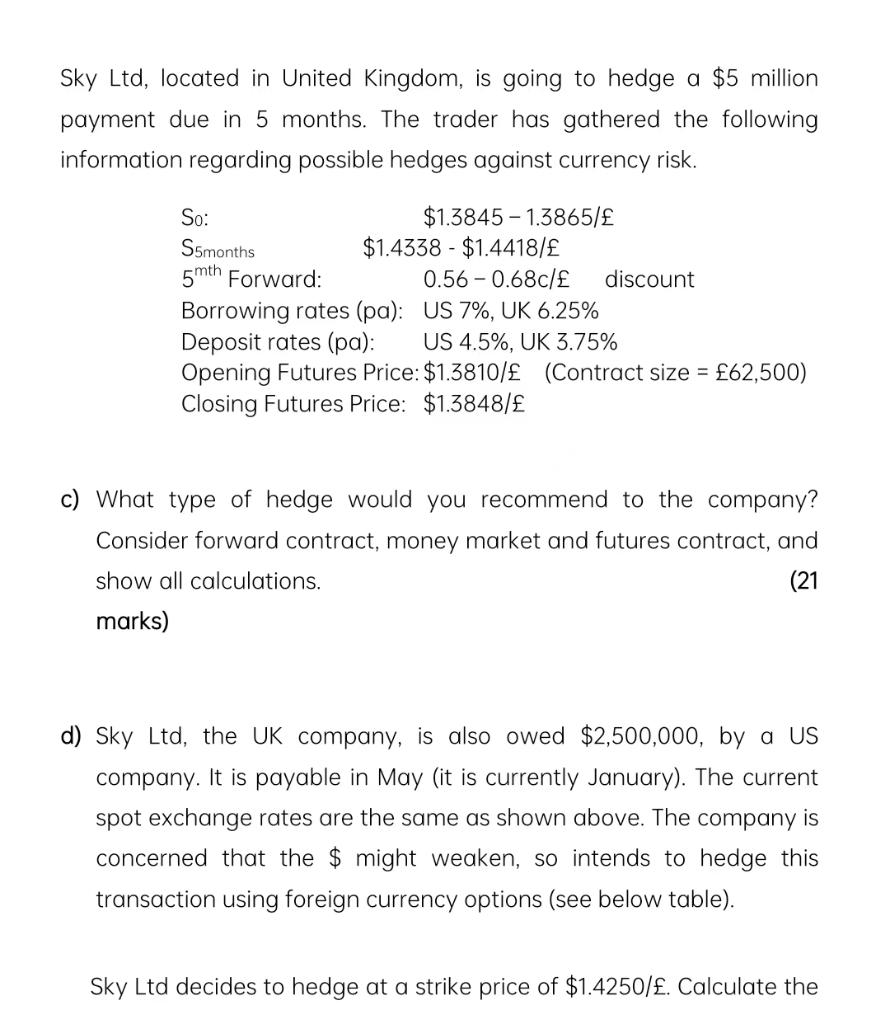

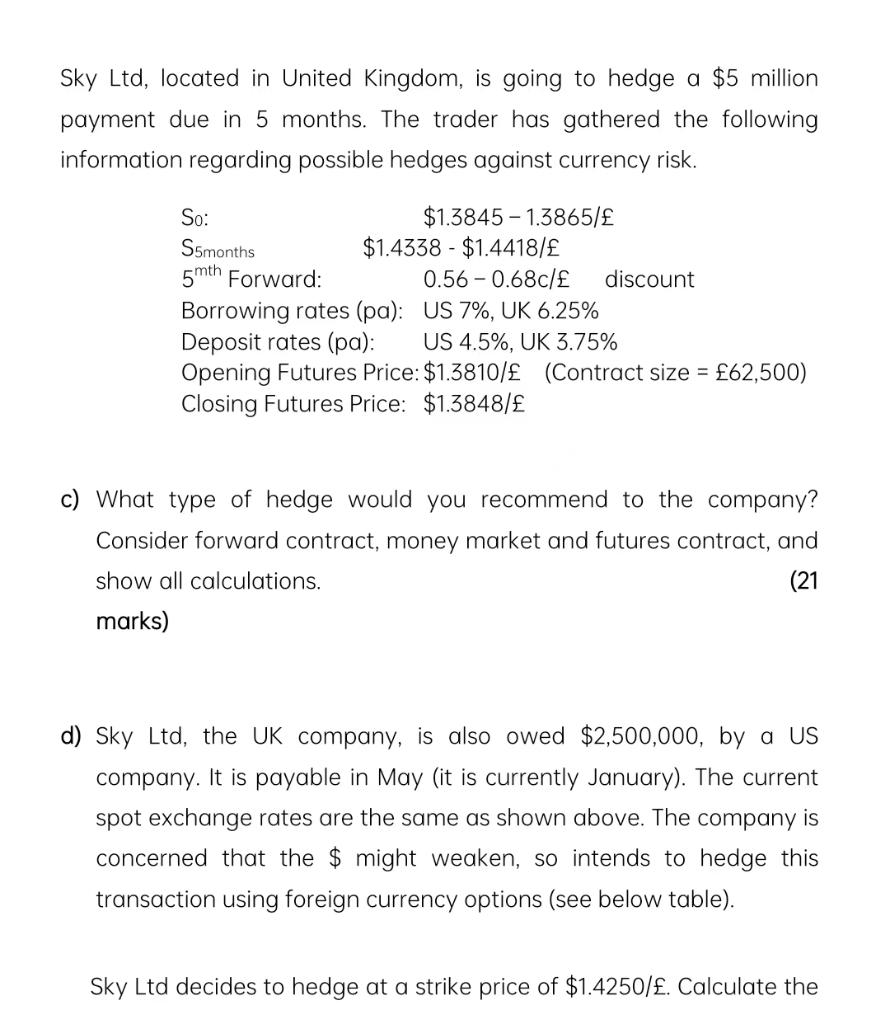

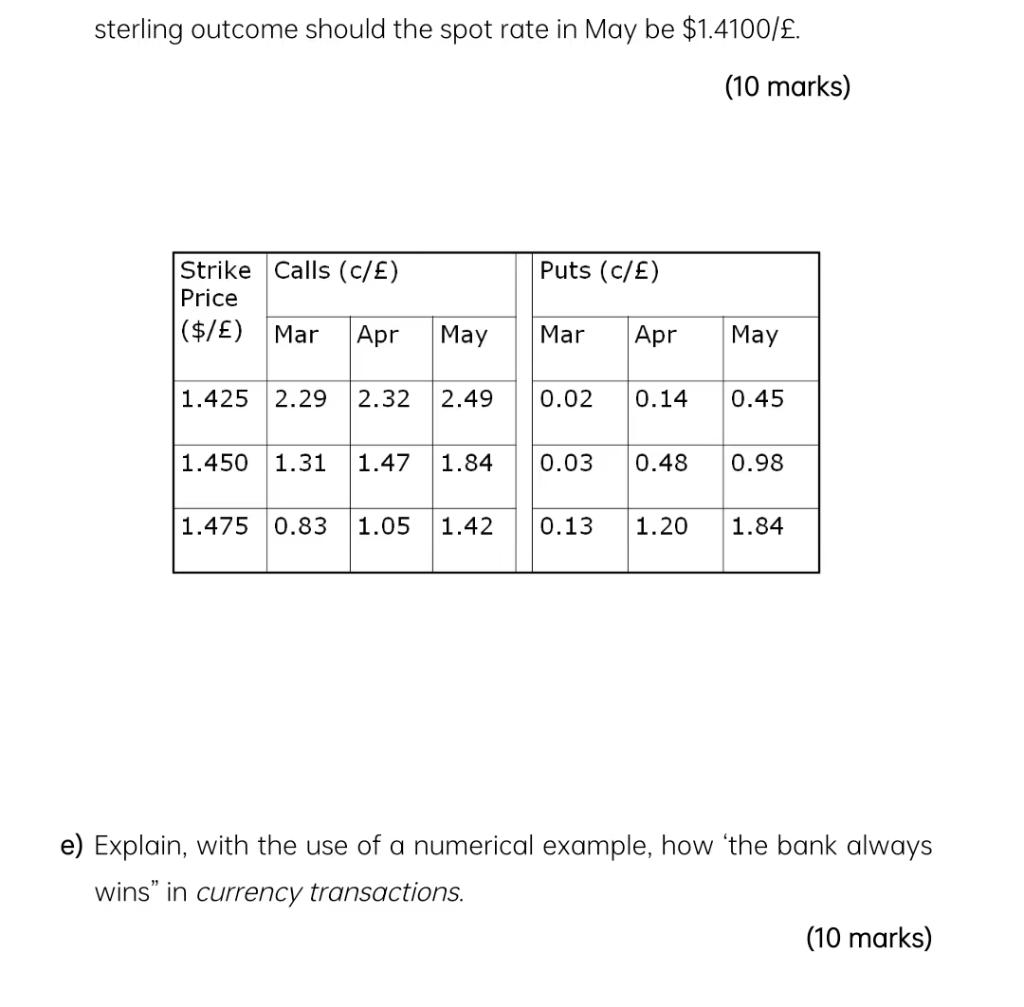

Question 1- Foreign Currency Hedging Below is a table of currency spot rates relating to the (fictitious) currencies used among various island nations of the Pacific Ocean. They are quoted using the indirect method from New Zealand's perspective. Guam L Samoa m Fiji y V1.1569- 16.512- ma0.5248- New Zealand $ 16.898/$ 1.1821/$ 0.5369/$ Cook Islands 4 Kiribati 8 41 02.55- 103.91/$ Tonga n 85.4432- U7901.2- n4.0184- 5.81 09/$ 8002.3/$ 4.4561/$ Tahiti U With the exception of New Zealand there are no direct exchange rates between the islands of the Pacific. This means that an exchange of currency between two non-New Zealand nations involves, first, converting into New Zealand $, then converting those New Zealand $ into the desired currency. a) Using the exchange rates given above perform the following currency conversions: i. 10 million of Samoa currency into the currency of Kiribati. ii. 5 million of Tonga currency into the currency of Cook Islands. (4 marks) b) Critically assess FIVE different factors which can influence currency exchange rates. Your answer should include how the factor influences currency exchange rates and the significance and prevalence of their influence. Sky Ltd, located in United Kingdom, is going to hedge a $5 million payment due in 5 months. The trader has gathered the following information regarding possible hedges against currency risk. So: S5months 5mth Forward: $1.3845-1.3865/ $1.4338 $1.4418/ 0.56 0.68c/ discount US 7%, UK 6.25% US 4.5%, UK 3.75% Borrowing rates (pa): Deposit rates (pa): Opening Futures Price: $1.3810/ (Contract size = 62,500) Closing Futures Price: $1.3848/ c) What type of hedge would you recommend to the company? Consider forward contract, money market and futures contract, and Ishow all calculations. (21 marks) d) Sky Ltd, the UK company, is also owed $2,500,000, by a US company. It is payable in May (it is currently January). The current spot exchange rates are the same as shown above. The company is concerned that the $ might weaken, so intends to hedge this transaction using foreign currency options (see below table). Sky Ltd decides to hedge at a strike price of $1.4250/. Calculate the Sky Ltd, located in United Kingdom, is going to hedge a $5 million payment due in 5 months. The trader has gathered the following information regarding possible hedges against currency risk. So: S5months 5mth Forward: $1.3845-1.3865/ $1.4338 $1.4418/ 0.56 0.68c/ discount US 7%, UK 6.25% US 4.5%, UK 3.75% Borrowing rates (pa): Deposit rates (pa): Opening Futures Price: $1.3810/ (Contract size = 62,500) Closing Futures Price: $1.3848/ c) What type of hedge would you recommend to the company? Consider forward contract, money market and futures contract, and Ishow all calculations. (21 marks) d) Sky Ltd, the UK company, is also owed $2,500,000, by a US company. It is payable in May (it is currently January). The current spot exchange rates are the same as shown above. The company is concerned that the $ might weaken, so intends to hedge this transaction using foreign currency options (see below table). Sky Ltd decides to hedge at a strike price of $1.4250/. Calculate the sterling outcome should the spot rate in May be $1.4100/. (10 marks) Strike Calls (c/) Price ($/ ) Mar Apr 1.425 May 2.29 2.32 2.49 Puts (c/) Mar Apr May 0.02 0.14 0.45 1.450 ..31 1.47 1.84 0.03 0.48 0.98 1.475 0.83 1.05 1.42 0.13 1.20 1.84 e) Explain, with the use of a numerical example, how 'the bank always wins" in currency transactions. (10 marks) Question 1- Foreign Currency Hedging Below is a table of currency spot rates relating to the (fictitious) currencies used among various island nations of the Pacific Ocean. They are quoted using the indirect method from New Zealand's perspective. Guam L Samoa m Fiji y V1.1569- 16.512- ma0.5248- New Zealand $ 16.898/$ 1.1821/$ 0.5369/$ Cook Islands 4 Kiribati 8 41 02.55- 103.91/$ Tonga n 85.4432- U7901.2- n4.0184- 5.81 09/$ 8002.3/$ 4.4561/$ Tahiti U With the exception of New Zealand there are no direct exchange rates between the islands of the Pacific. This means that an exchange of currency between two non-New Zealand nations involves, first, converting into New Zealand $, then converting those New Zealand $ into the desired currency. a) Using the exchange rates given above perform the following currency conversions: i. 10 million of Samoa currency into the currency of Kiribati. ii. 5 million of Tonga currency into the currency of Cook Islands. (4 marks) b) Critically assess FIVE different factors which can influence currency exchange rates. Your answer should include how the factor influences currency exchange rates and the significance and prevalence of their influence. Sky Ltd, located in United Kingdom, is going to hedge a $5 million payment due in 5 months. The trader has gathered the following information regarding possible hedges against currency risk. So: S5months 5mth Forward: $1.3845-1.3865/ $1.4338 $1.4418/ 0.56 0.68c/ discount US 7%, UK 6.25% US 4.5%, UK 3.75% Borrowing rates (pa): Deposit rates (pa): Opening Futures Price: $1.3810/ (Contract size = 62,500) Closing Futures Price: $1.3848/ c) What type of hedge would you recommend to the company? Consider forward contract, money market and futures contract, and Ishow all calculations. (21 marks) d) Sky Ltd, the UK company, is also owed $2,500,000, by a US company. It is payable in May (it is currently January). The current spot exchange rates are the same as shown above. The company is concerned that the $ might weaken, so intends to hedge this transaction using foreign currency options (see below table). Sky Ltd decides to hedge at a strike price of $1.4250/. Calculate the Sky Ltd, located in United Kingdom, is going to hedge a $5 million payment due in 5 months. The trader has gathered the following information regarding possible hedges against currency risk. So: S5months 5mth Forward: $1.3845-1.3865/ $1.4338 $1.4418/ 0.56 0.68c/ discount US 7%, UK 6.25% US 4.5%, UK 3.75% Borrowing rates (pa): Deposit rates (pa): Opening Futures Price: $1.3810/ (Contract size = 62,500) Closing Futures Price: $1.3848/ c) What type of hedge would you recommend to the company? Consider forward contract, money market and futures contract, and Ishow all calculations. (21 marks) d) Sky Ltd, the UK company, is also owed $2,500,000, by a US company. It is payable in May (it is currently January). The current spot exchange rates are the same as shown above. The company is concerned that the $ might weaken, so intends to hedge this transaction using foreign currency options (see below table). Sky Ltd decides to hedge at a strike price of $1.4250/. Calculate the sterling outcome should the spot rate in May be $1.4100/. (10 marks) Strike Calls (c/) Price ($/ ) Mar Apr 1.425 May 2.29 2.32 2.49 Puts (c/) Mar Apr May 0.02 0.14 0.45 1.450 ..31 1.47 1.84 0.03 0.48 0.98 1.475 0.83 1.05 1.42 0.13 1.20 1.84 e) Explain, with the use of a numerical example, how 'the bank always wins" in currency transactions. (10 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts