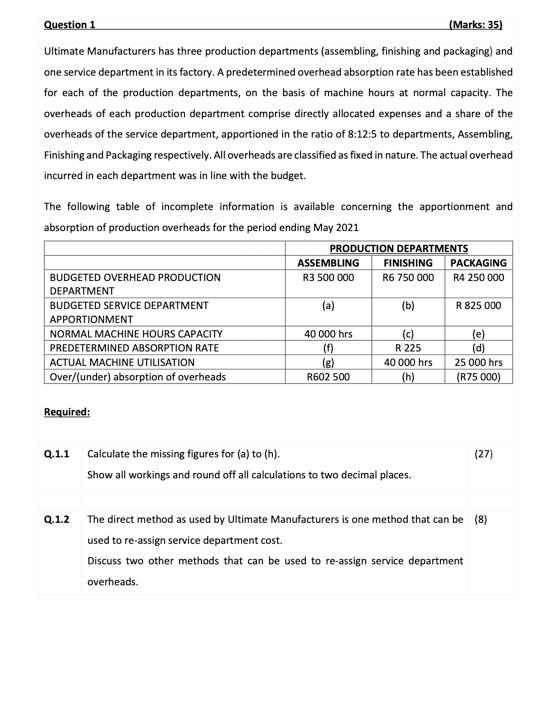

Question 1 (Marks: 35) Ultimate Manufacturers has three production departments (assembling, finishing and packaging) and one service department in its factory. A predetermined overhead absorption rate has been established for each of the production departments, on the basis of machine hours at normal capacity. The overheads of each production department comprise directly allocated expenses and a share of the overheads of the service department, apportioned in the ratio of 8:12:5 to departments, Assembling, Finishing and Packaging respectively. All overheads are classified as fixed in nature. The actual overhead incurred in each department was in line with the budget. The following table of incomplete information is available concerning the apportionment and absorption of production overheads for the period ending May 2021 PRODUCTION DEPARTMENTS ASSEMBLING FINISHING PACKAGING BUDGETED OVERHEAD PRODUCTION R3 500 000 R6 750 000 R4 250 000 DEPARTMENT BUDGETED SERVICE DEPARTMENT (a) (b) R 825 000 APPORTIONMENT NORMAL MACHINE HOURS CAPACITY 40 000 hrs (c) (e) PREDETERMINED ABSORPTION RATE R 225 (d) ACTUAL MACHINE UTILISATION (g) 40 000 hrs 25 000 hrs Over/(under) absorption of overheads R602 500 (h) (R75 000) Required: Q.1.1 (27) Calculate the missing figures for (a) to (h). Show all workings and round off all calculations to two decimal places. Q.1.2 The direct method as used by Ultimate Manufacturers is one method that can be (8) used to re-assign service department cost. Discuss two other methods that can be used to re-assign service department overheads. Question 1 (Marks: 35) Ultimate Manufacturers has three production departments (assembling, finishing and packaging) and one service department in its factory. A predetermined overhead absorption rate has been established for each of the production departments, on the basis of machine hours at normal capacity. The overheads of each production department comprise directly allocated expenses and a share of the overheads of the service department, apportioned in the ratio of 8:12:5 to departments, Assembling, Finishing and Packaging respectively. All overheads are classified as fixed in nature. The actual overhead incurred in each department was in line with the budget. The following table of incomplete information is available concerning the apportionment and absorption of production overheads for the period ending May 2021 PRODUCTION DEPARTMENTS ASSEMBLING FINISHING PACKAGING BUDGETED OVERHEAD PRODUCTION R3 500 000 R6 750 000 R4 250 000 DEPARTMENT BUDGETED SERVICE DEPARTMENT (a) (b) R 825 000 APPORTIONMENT NORMAL MACHINE HOURS CAPACITY 40 000 hrs (c) (e) PREDETERMINED ABSORPTION RATE R 225 (d) ACTUAL MACHINE UTILISATION (g) 40 000 hrs 25 000 hrs Over/(under) absorption of overheads R602 500 (h) (R75 000) Required: Q.1.1 (27) Calculate the missing figures for (a) to (h). Show all workings and round off all calculations to two decimal places. Q.1.2 The direct method as used by Ultimate Manufacturers is one method that can be (8) used to re-assign service department cost. Discuss two other methods that can be used to re-assign service department overheads