Answered step by step

Verified Expert Solution

Question

1 Approved Answer

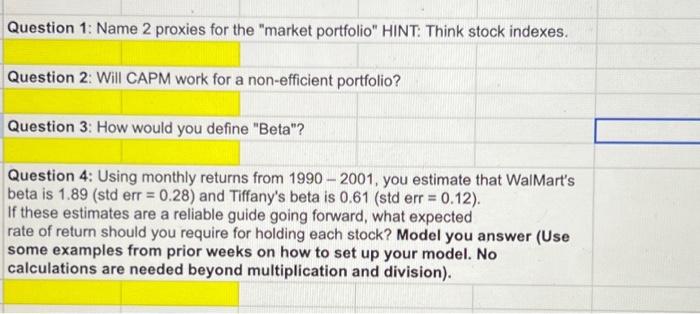

Question 1: Name 2 proxies for the market portfolio HINT: Think stock indexes. Question 2: Will CAPM work for a non-efficient portfolio? Question 3: How

Question 1: Name 2 proxies for the "market portfolio" HINT: Think stock indexes. Question 2: Will CAPM work for a non-efficient portfolio? Question 3: How would you define "Beta"? Question 4: Using monthly returns from 1990 - 2001, you estimate that WalMart's beta is 1.89 (std err = 0.28) and Tiffany's beta is 0.61 (std err = 0.12). If these estimates are a reliable guide going forward, what expected rate of return should you require for holding each stock? Model you answer (Use some examples from prior weeks on how to set up your model. No calculations are needed beyond multiplication and division).

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial And Insurance Formulas

Authors: Tomas Cipra

2010th Edition

3790829013, 978-3790829013