Answered step by step

Verified Expert Solution

Question

1 Approved Answer

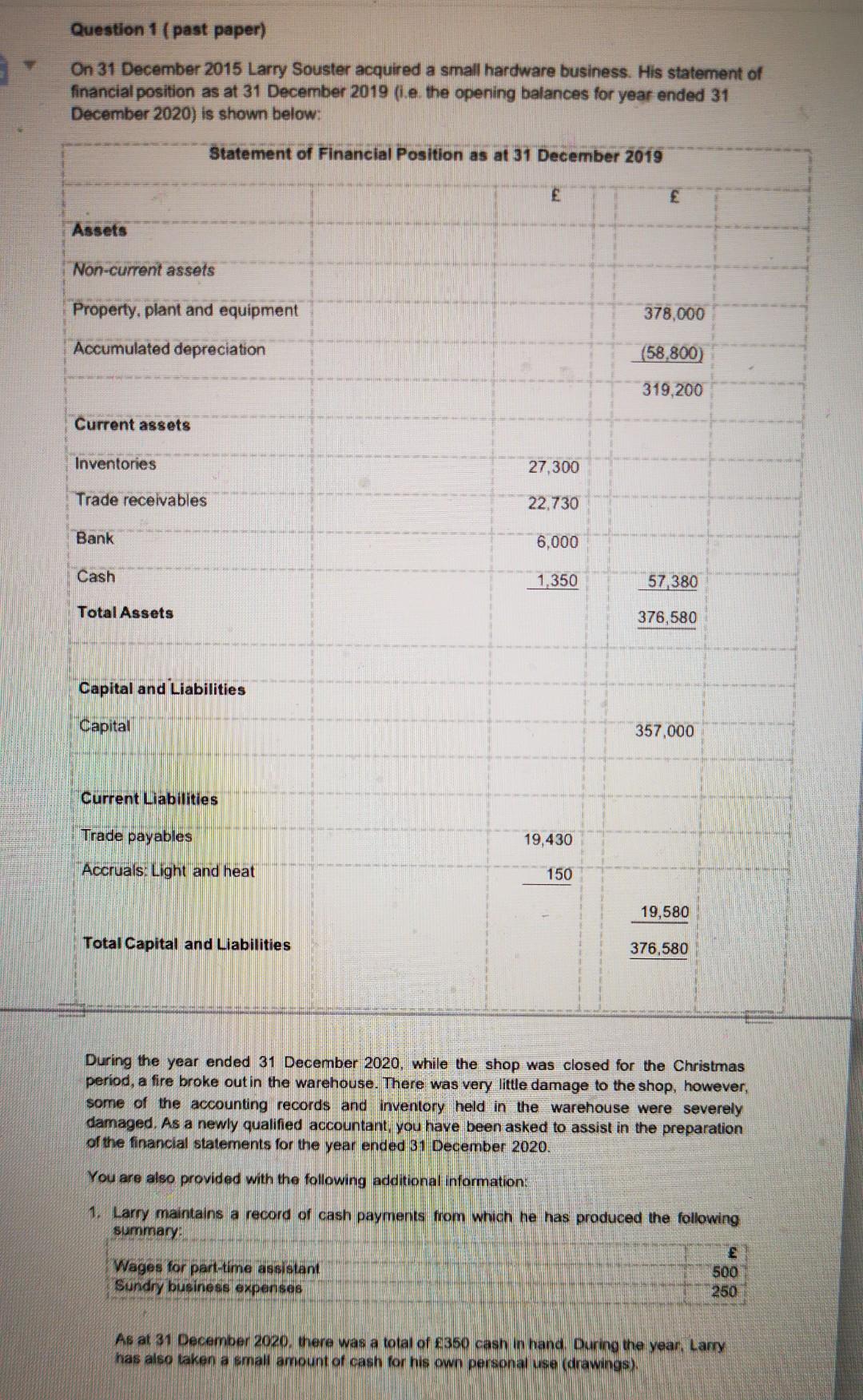

Question 1 (past paper) On 31 December 2015 Larry Souster acquired a small hardware business. His statement of financial position as at 31 December 2019

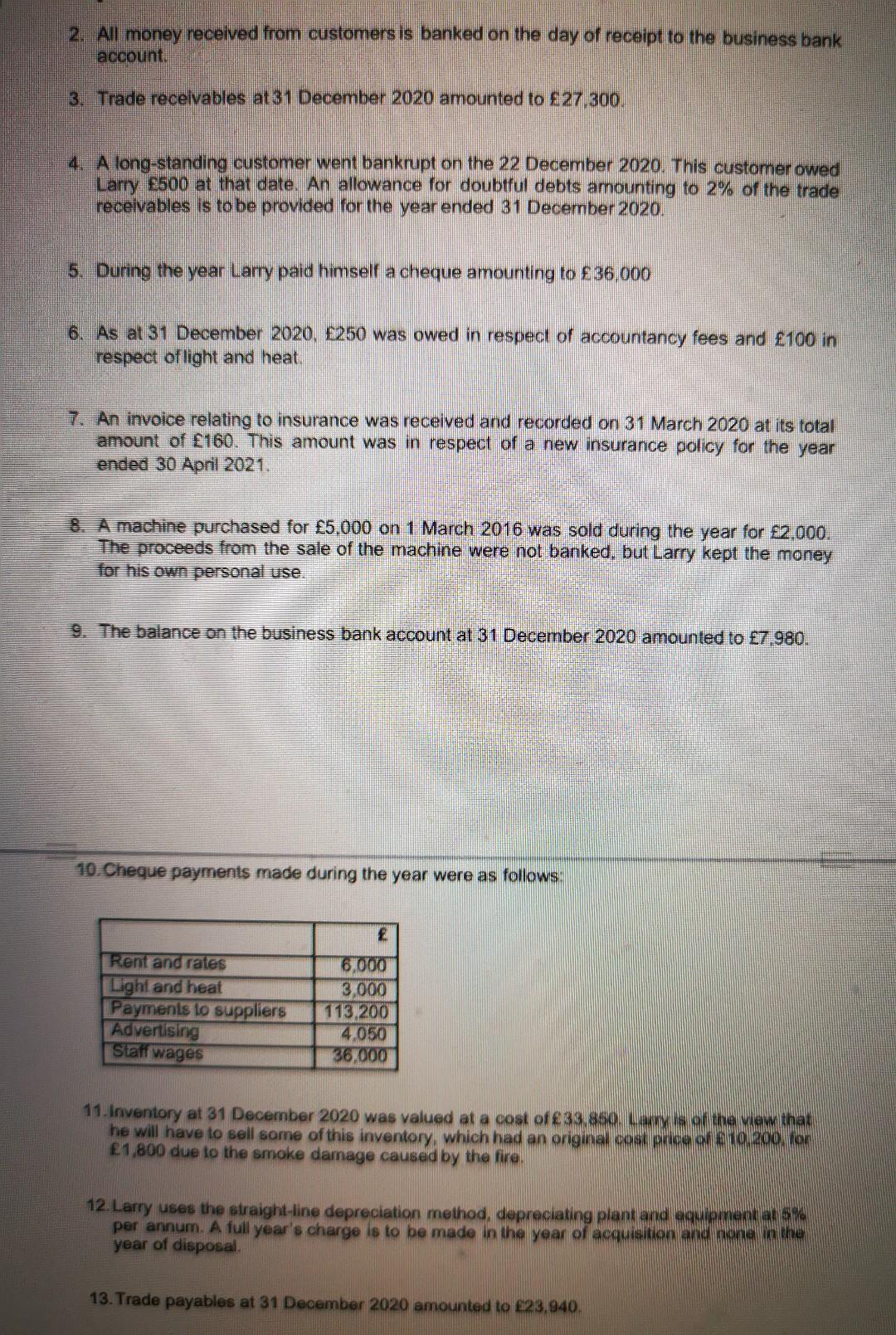

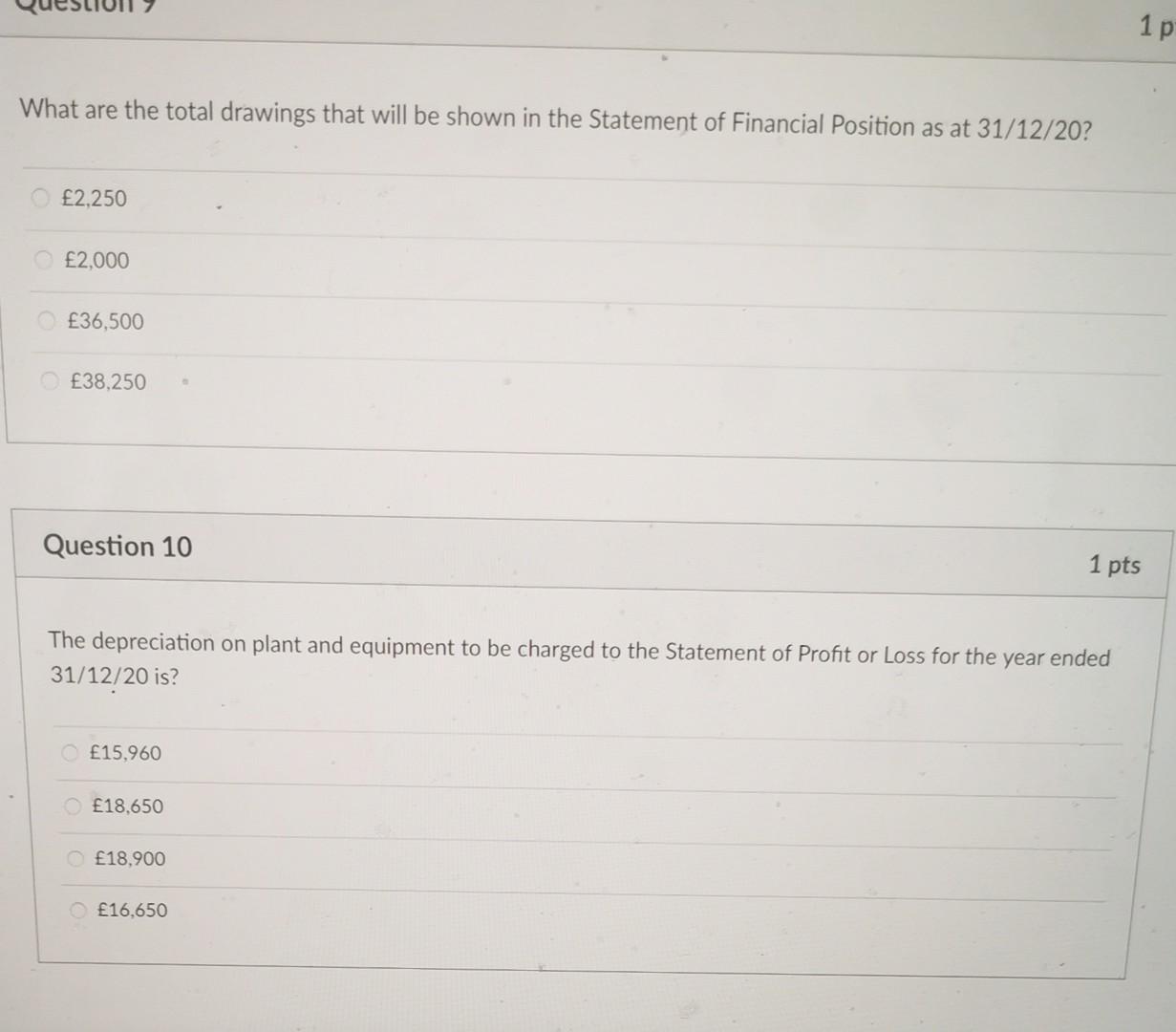

Question 1 (past paper) On 31 December 2015 Larry Souster acquired a small hardware business. His statement of financial position as at 31 December 2019 (i.e. the opening balances for year ended 31 December 2020) is shown below: During the year ended 31 December 2020, while the shop was closed for the Christmas period, a fire broke out in the warehouse. There was very little damage to the shop, however, some of the accounting records and inventory held in the warehouse were severely damaged. As a newly qualified accountant, you have been asked to assist in the preparation of the financial statements for the year ended 31 December 2020. You are also provided with the following additional information: 1. Larry maintains a record of cash payments from which he has produced the following summary: Wages for part time assistant Sundry business expenses As at 31 December 2020, there was a total of 350 cash in hand. During the year, Lary has also laken a small amount of cash for his own personal use (drawings). 2. All money received from customers is banked on the day of receipt to the business bank account. 3. Trade receivables at31 December 2020 amounted to 27,300. 4. A long-standing customer went bankrupt on the 22 December 2020. This customer owed Larry 500 at that date. An allowance for doubtful debts amounting to 2% of the trade receivables is to be provided for the year ended 31 December 2020 . 5. During the year Larry paid himself a cheque amounting to 36,000 6. As at 31 December 2020, 250 was owed in respect of accountancy fees and 100 in respect of light and heat. 7. An invoice relating to insurance was received and recorded on 31 March 2020 at its total amount of 160. This amount was in respect of a new insurance policy for the year ended 30 April 2021. 8. A machine purchased for 5,000 on 1 March 2016 was sold during the year for 2,000. The proceeds from the sale of the machine were not banked, but Larry kept the money for his own personal use. 9. The balance on the business bank account at 31 December 2020 amounted to 7,980. 10. Cheque payments made during the year were as follows: 11. Inventory at 31 December 2020 was valued at a cost of 33,850. Lamy is of the view that he will have to sell some of this inventory, which had an original cost prica or A fio 200, for 1,800 due to the smoke damage caused by the fire. 12. Larry uses the straight-line depreciation method, depreciating plant and aquipment at 5% per annum. A full year's charge is to be made in the year of acquisition and none in the year of disposal. 13. Trade payables at 31 December 2020 amounted to E23.940. What are the total drawings that will be shown in the Statement of Financial Position as at 31/12/20 ? 2,250 2,000 36,500 38,250 Question 10 The depreciation on plant and equipment to be charged to the Statement of Profit or Loss for the year ended 31/12/20 is? 15,960 18,650 18,900 16,650

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Audit Education

Authors: Karen Van Peursem, Elizabeth Monk, Richard M.S. Wilson, Ralph Adler

1st Edition

1138192856, 978-1138192850