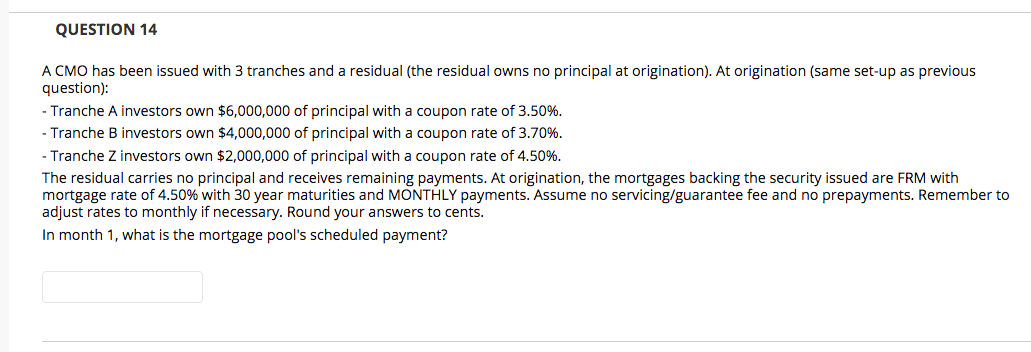

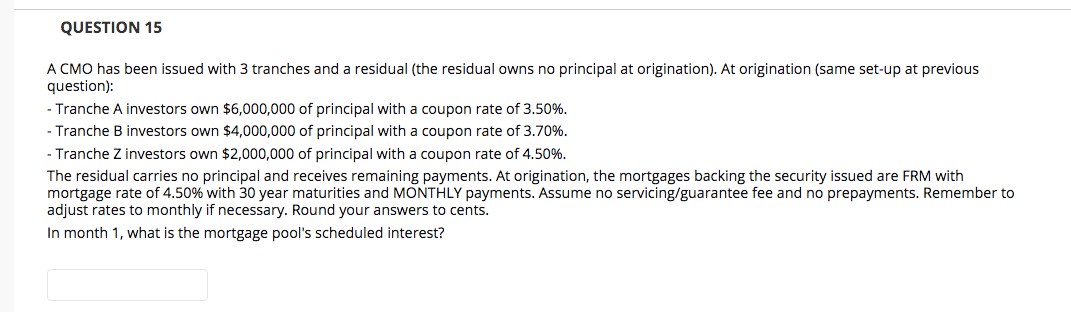

QUESTION 14 A CMO has been issued with 3 tranches and a residual (the residual owns no principal at origination). At origination (same set-up as previous question): - Tranche A investors own $6,000,000 of principal with a coupon rate of 3.50%. - Tranche B investors own $4,000,000 of principal with a coupon rate of 3.70%. - Tranche Z investors own $2,000,000 of principal with a coupon rate of 4.50%. The residual carries no principal and receives remaining payments. At origination, the mortgages backing the security issued are FRM with mortgage rate of 4.50% with 30 year maturities and MONTHLY payments. Assume no servicing/guarantee fee and no prepayments. Remember to adjust rates to monthly if necessary. Round your answers to cents. In month 1, what is the mortgage pool's scheduled payment? QUESTION 15 A CMO has been issued with 3 tranches and a residual (the residual owns no principal at origination). At origination (same set-up at previous question): - Tranche A investors own $6,000,000 of principal with a coupon rate of 3.50%. - Tranche B investors own $4,000,000 of principal with a coupon rate of 3.70%. - Tranche Z investors own $2,000,000 of principal with a coupon rate of 4.50%. The residual carries no principal and receives remaining payments. At origination, the mortgages backing the security issued are FRM with mortgage rate of 4.50% with 30 year maturities and MONTHLY payments. Assume no servicing/guarantee fee and no prepayments. Remember to adjust rates to monthly if necessary. Round your answers to cents. In month 1, what is the mortgage pool's scheduled interest? QUESTION 14 A CMO has been issued with 3 tranches and a residual (the residual owns no principal at origination). At origination (same set-up as previous question): - Tranche A investors own $6,000,000 of principal with a coupon rate of 3.50%. - Tranche B investors own $4,000,000 of principal with a coupon rate of 3.70%. - Tranche Z investors own $2,000,000 of principal with a coupon rate of 4.50%. The residual carries no principal and receives remaining payments. At origination, the mortgages backing the security issued are FRM with mortgage rate of 4.50% with 30 year maturities and MONTHLY payments. Assume no servicing/guarantee fee and no prepayments. Remember to adjust rates to monthly if necessary. Round your answers to cents. In month 1, what is the mortgage pool's scheduled payment? QUESTION 15 A CMO has been issued with 3 tranches and a residual (the residual owns no principal at origination). At origination (same set-up at previous question): - Tranche A investors own $6,000,000 of principal with a coupon rate of 3.50%. - Tranche B investors own $4,000,000 of principal with a coupon rate of 3.70%. - Tranche Z investors own $2,000,000 of principal with a coupon rate of 4.50%. The residual carries no principal and receives remaining payments. At origination, the mortgages backing the security issued are FRM with mortgage rate of 4.50% with 30 year maturities and MONTHLY payments. Assume no servicing/guarantee fee and no prepayments. Remember to adjust rates to monthly if necessary. Round your answers to cents. In month 1, what is the mortgage pool's scheduled interest