Question

Question 2 210 days ago you purchased a newly issued bond with a maturity of 10 years. The bond carries a coupon rate of 8%

Question 2

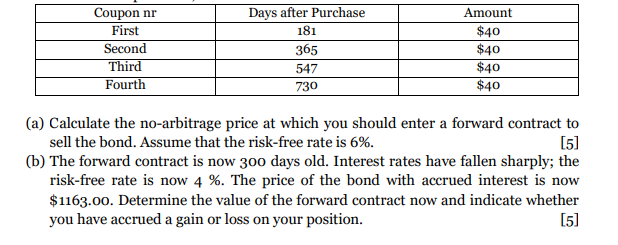

210 days ago you purchased a newly issued bond with a maturity of 10 years. The bond carries a coupon rate of 8% paid semi-annually and has a face value of $1,000. The price of the bond with accrued interest is currently $1106.84. You plan to sell the bond 395 days from now. The schedule of coupon payments over the first two years, from the date of purchase, is as follows:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Dividend Stocks For Dummies

Authors: Lawrence Carrel

1st Edition

0470466014, 978-0470466018