Answered step by step

Verified Expert Solution

Question

1 Approved Answer

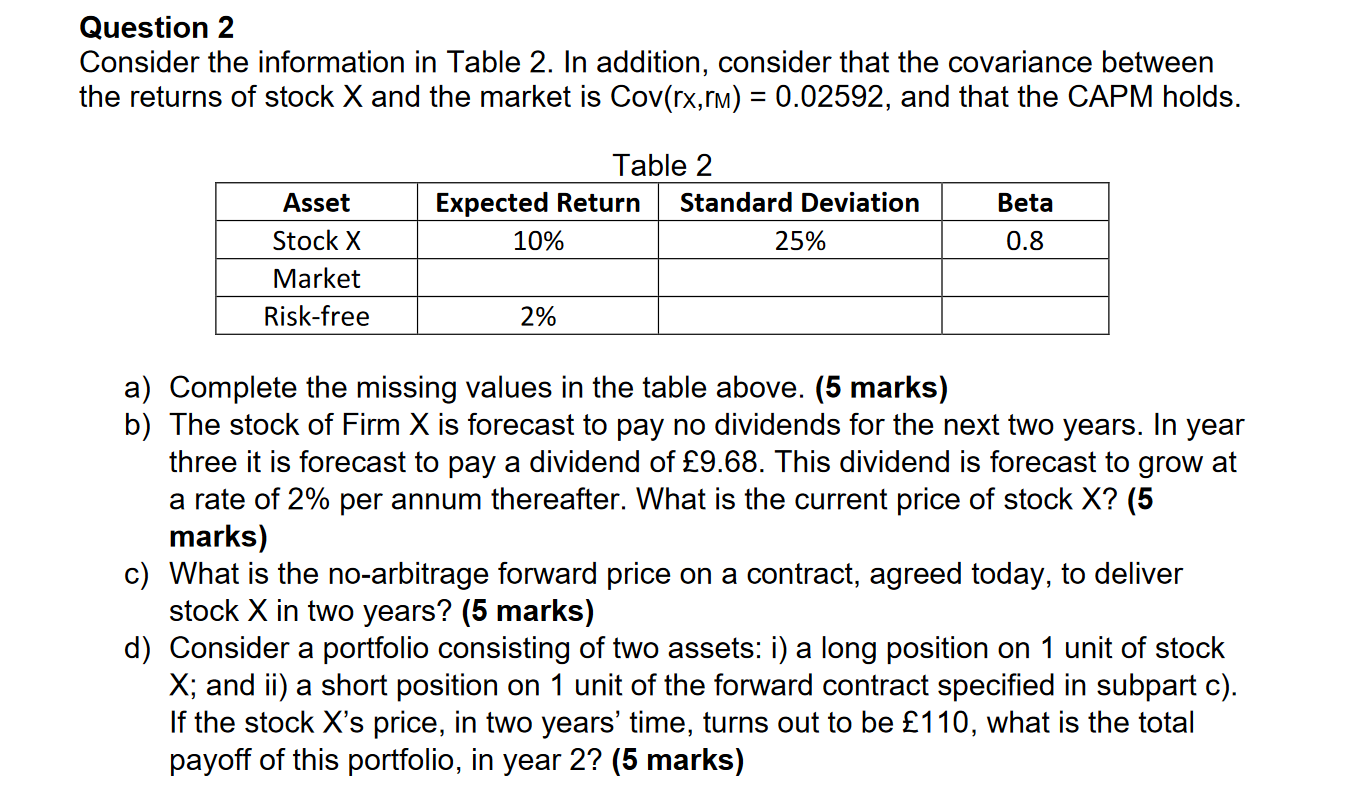

Question 2 Consider the information in Table 2. In addition, consider that the covariance between the returns of stock X and the market is Cov(rx,rM)=0.02592,

Question 2 Consider the information in Table 2. In addition, consider that the covariance between the returns of stock X and the market is Cov(rx,rM)=0.02592, and that the CAPM holds. a) Complete the missing values in the table above. (5 marks) b) The stock of Firm X is forecast to pay no dividends for the next two years. In year three it is forecast to pay a dividend of 9.68. This dividend is forecast to grow at a rate of 2% per annum thereafter. What is the current price of stock X ? (5 marks) c) What is the no-arbitrage forward price on a contract, agreed today, to deliver stock X in two years? (5 marks) d) Consider a portfolio consisting of two assets: i) a long position on 1 unit of stock X; and ii ) a short position on 1 unit of the forward contract specified in subpart c ). If the stock X's price, in two years' time, turns out to be 110, what is the total payoff of this portfolio, in year 2

Question 2 Consider the information in Table 2. In addition, consider that the covariance between the returns of stock X and the market is Cov(rx,rM)=0.02592, and that the CAPM holds. a) Complete the missing values in the table above. (5 marks) b) The stock of Firm X is forecast to pay no dividends for the next two years. In year three it is forecast to pay a dividend of 9.68. This dividend is forecast to grow at a rate of 2% per annum thereafter. What is the current price of stock X ? (5 marks) c) What is the no-arbitrage forward price on a contract, agreed today, to deliver stock X in two years? (5 marks) d) Consider a portfolio consisting of two assets: i) a long position on 1 unit of stock X; and ii ) a short position on 1 unit of the forward contract specified in subpart c ). If the stock X's price, in two years' time, turns out to be 110, what is the total payoff of this portfolio, in year 2 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Finance With Excel

Authors: Simon Benninga

1st Edition

0195301501, 978-0195301502