Answered step by step

Verified Expert Solution

Question

1 Approved Answer

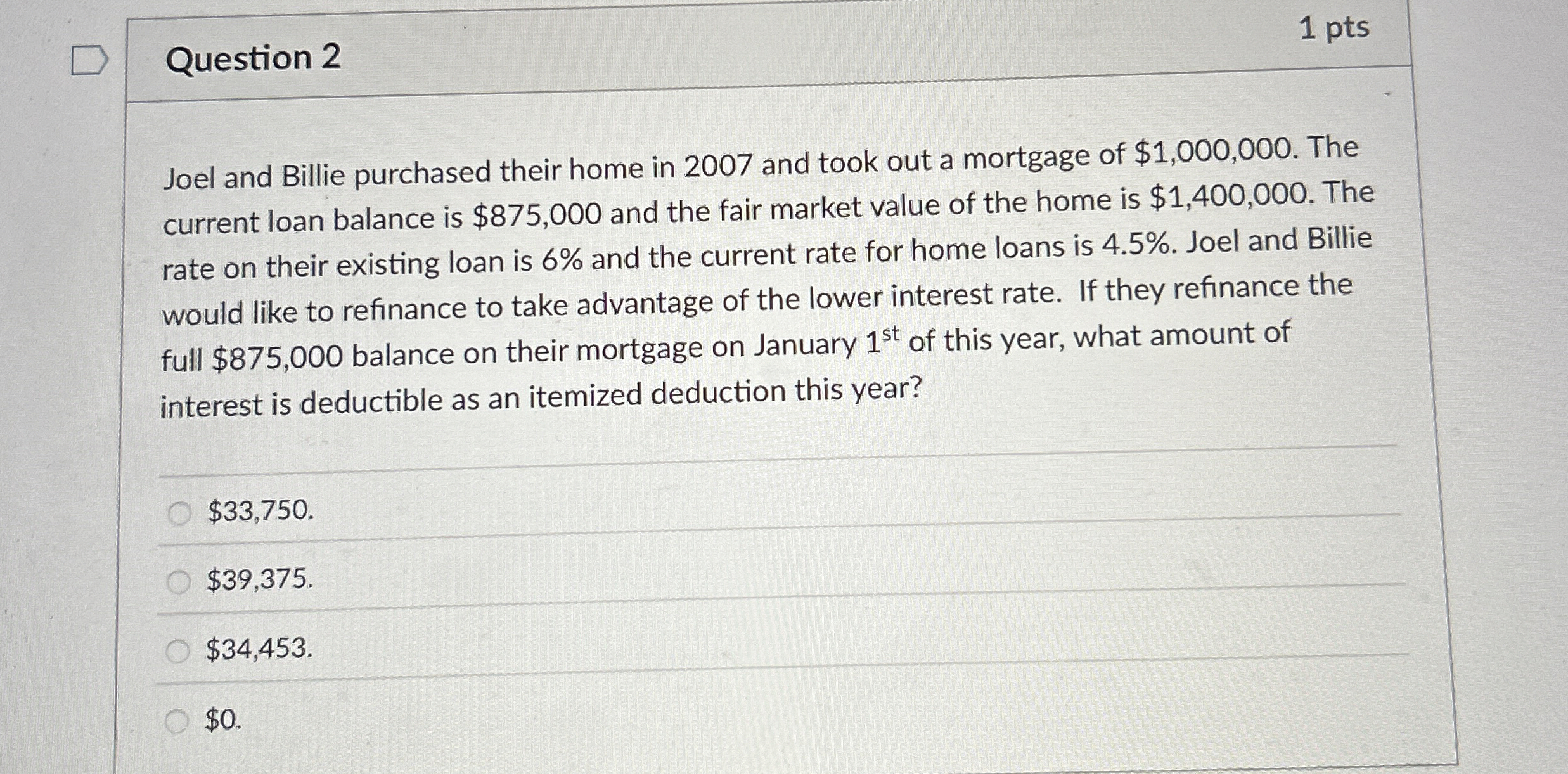

Question 2 Joel and Billie purchased their home in 2 0 0 7 and took out a mortgage of $ 1 , 0 0 0

Question

Joel and Billie purchased their home in and took out a mortgage of $ The

current loan balance is $ and the fair market value of the home is $ The

rate on their existing loan is and the current rate for home loans is Joel and Billie

would like to refinance to take advantage of the lower interest rate. If they refinance the

full $ balance on their mortgage on January of this year, what amount of

interest is deductible as an itemized deduction this year?

$

$

$

$

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cornerstones of Managerial Accounting

Authors: Mowen, Hansen, Heitger

3rd Edition

324660138, 978-0324660135