Answered step by step

Verified Expert Solution

Question

1 Approved Answer

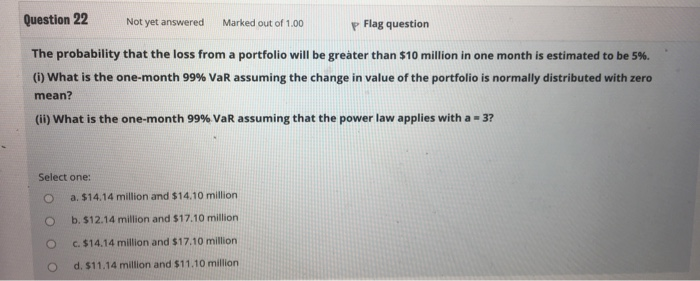

Question 22 Not yet answered Marked out of 1.00 p Flag question The probability that the loss from a portfolio will be greater than $10

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Management

Authors: Geert Bekaert, Robert J. Hodrick

2nd edition

013299755X, 132162768, 9780132997553, 978-0132162760