Answered step by step

Verified Expert Solution

Question

1 Approved Answer

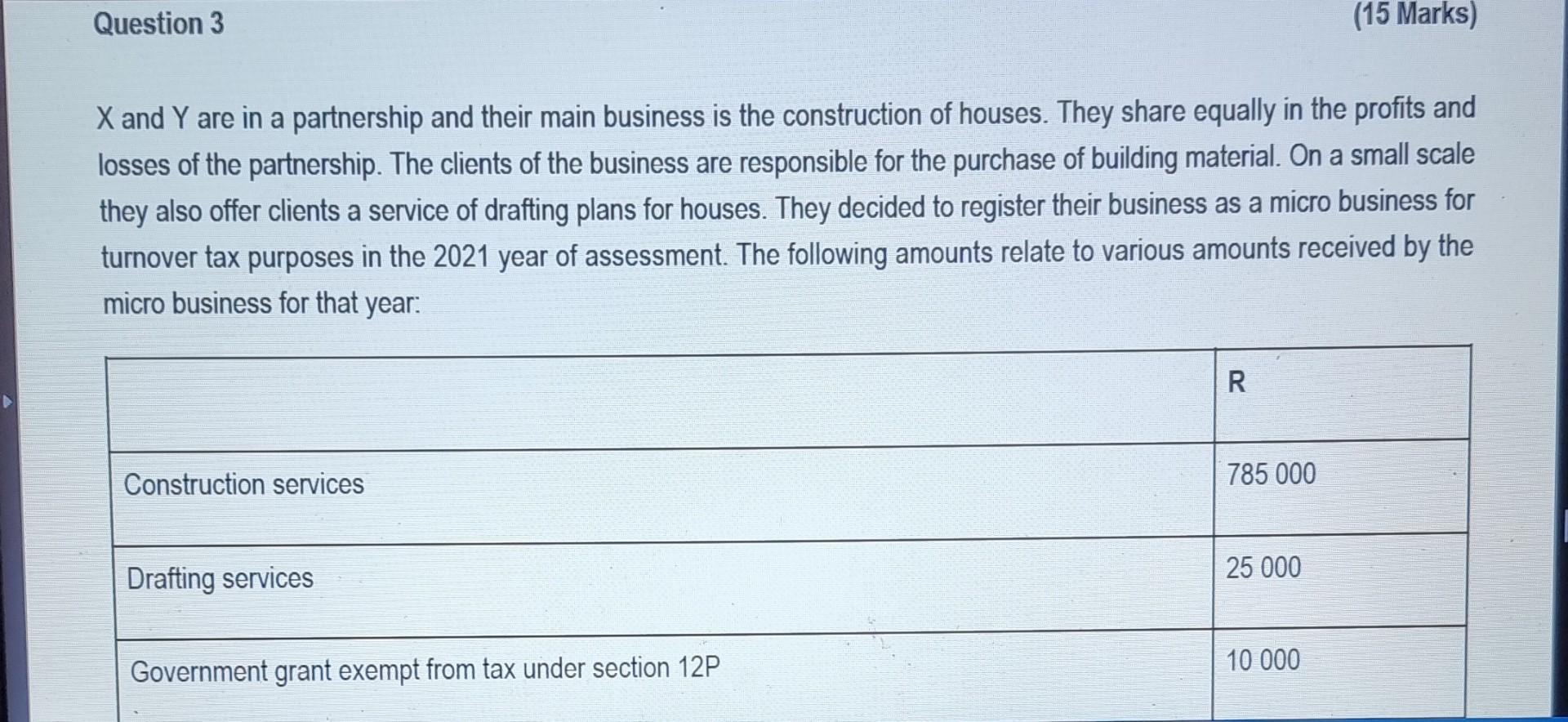

Question 3 (15 Marks) X and Y are in a partnership and their main business is the construction of houses. They share equally in the

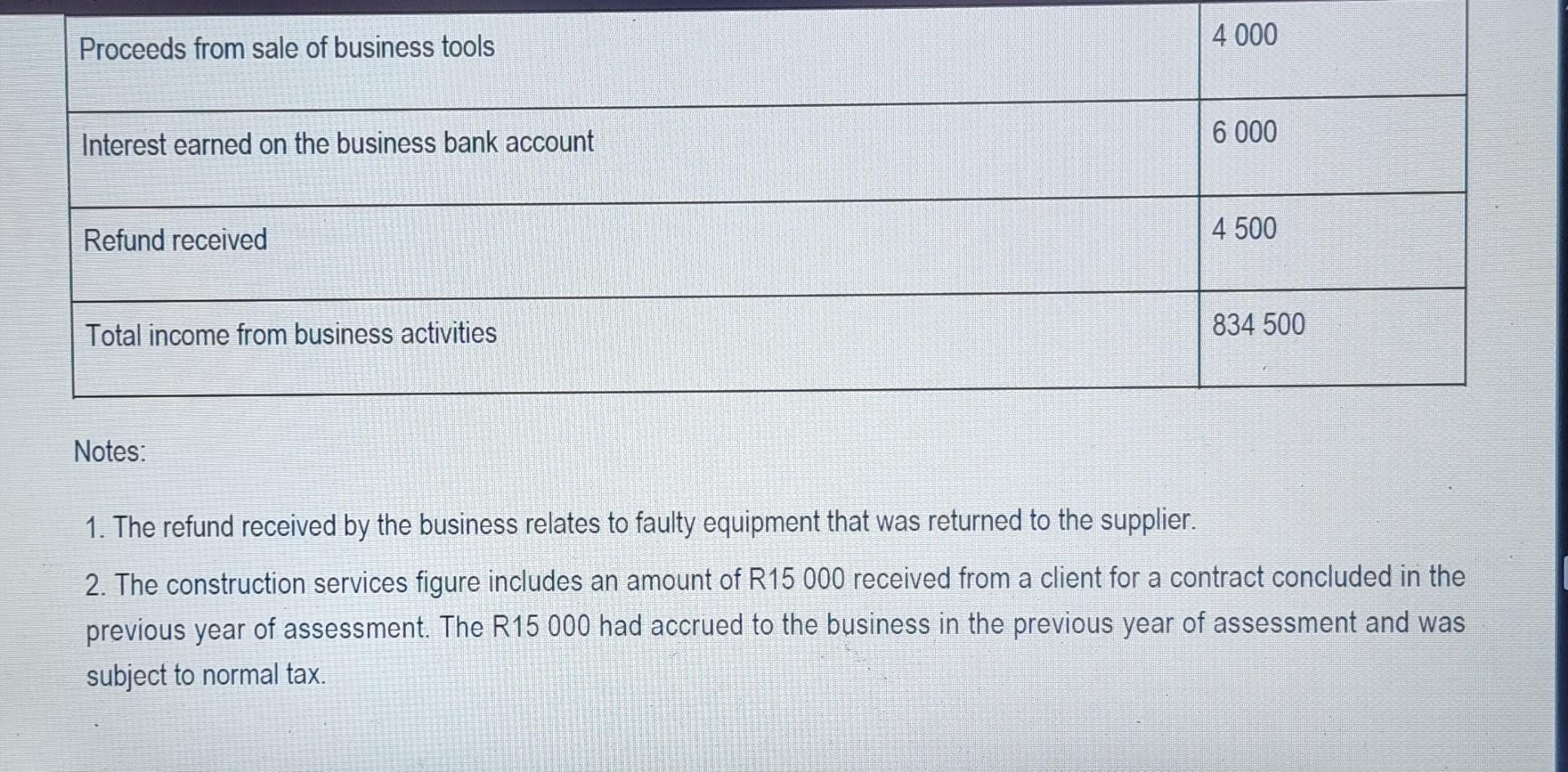

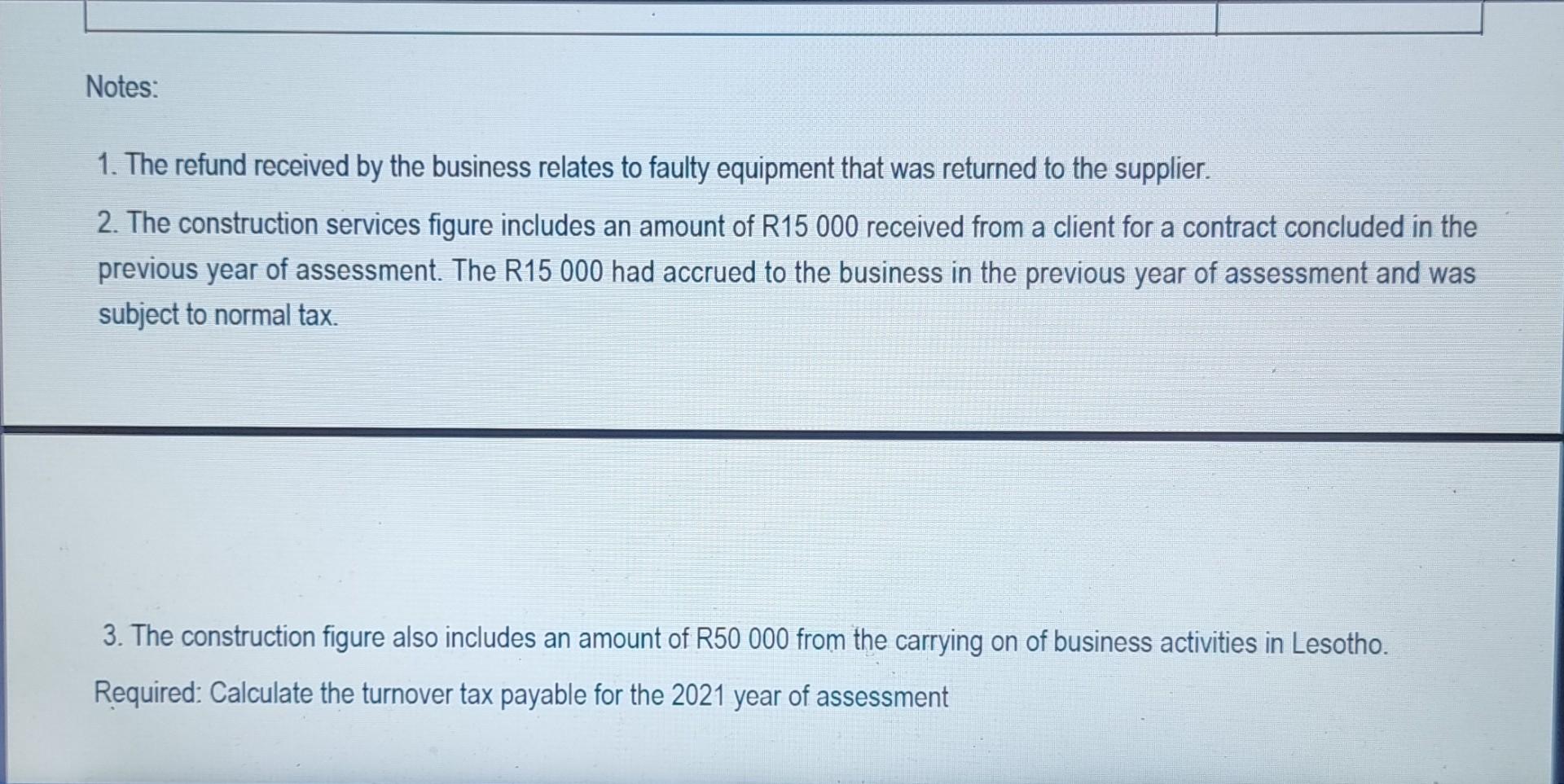

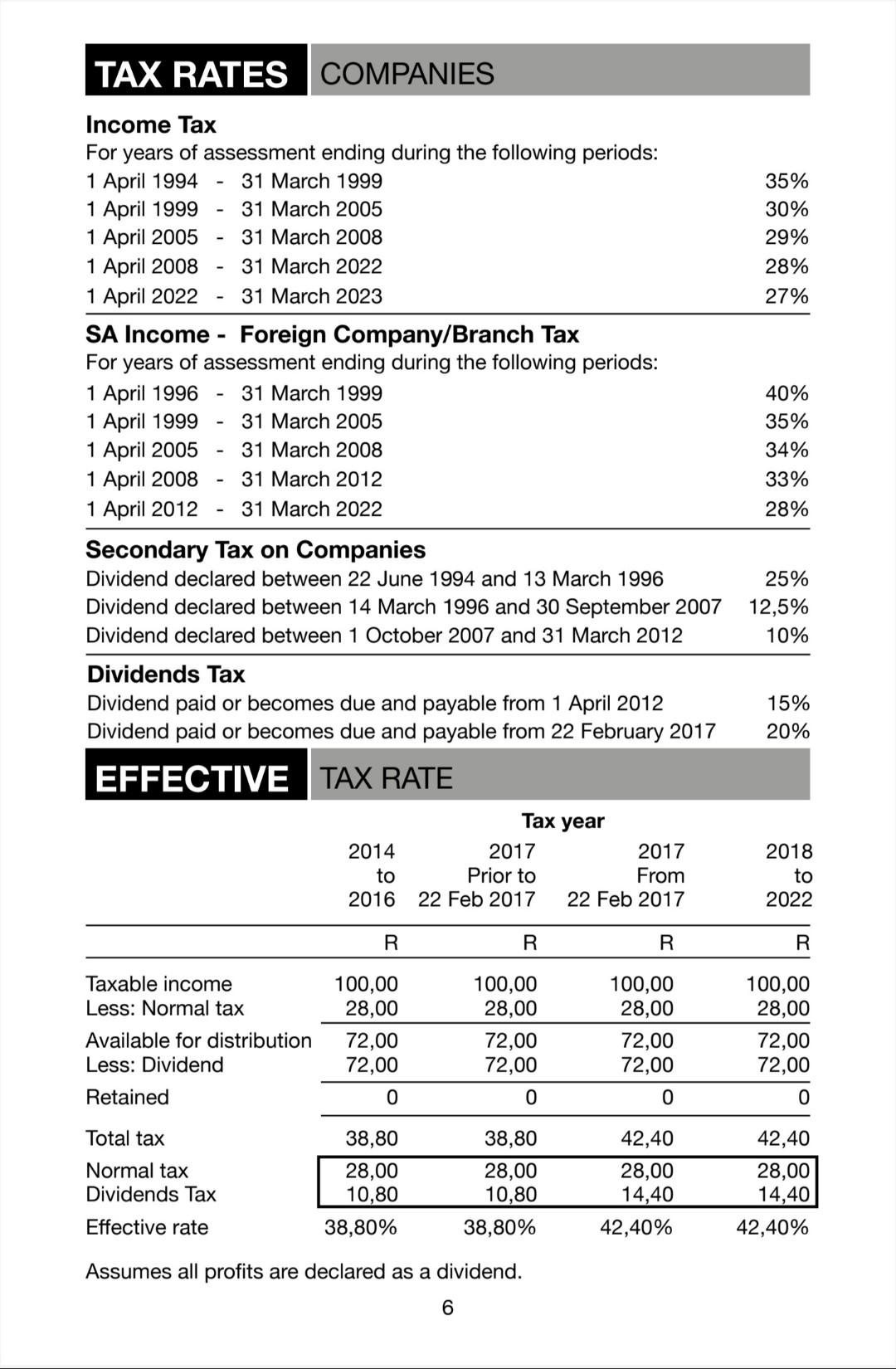

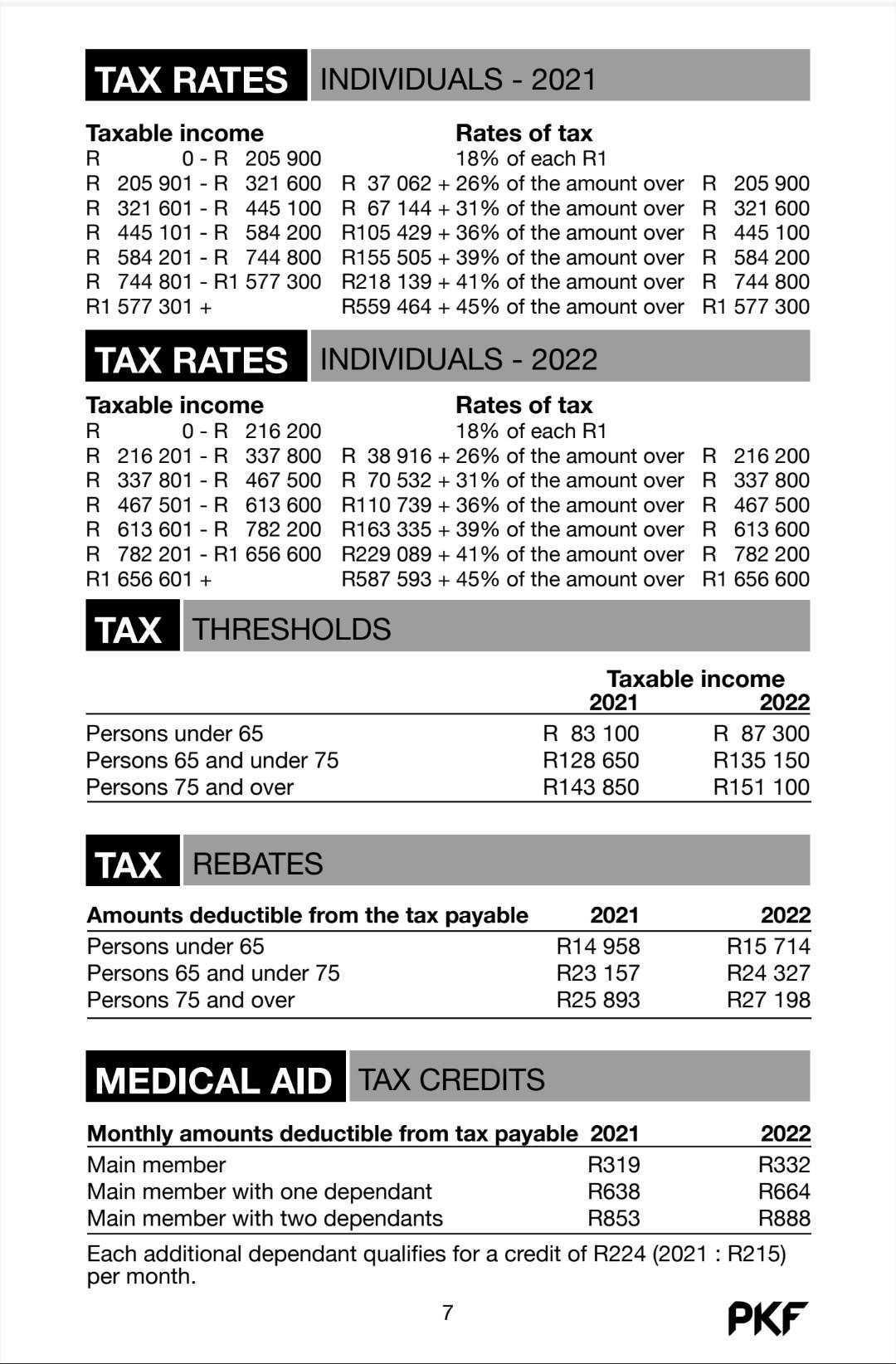

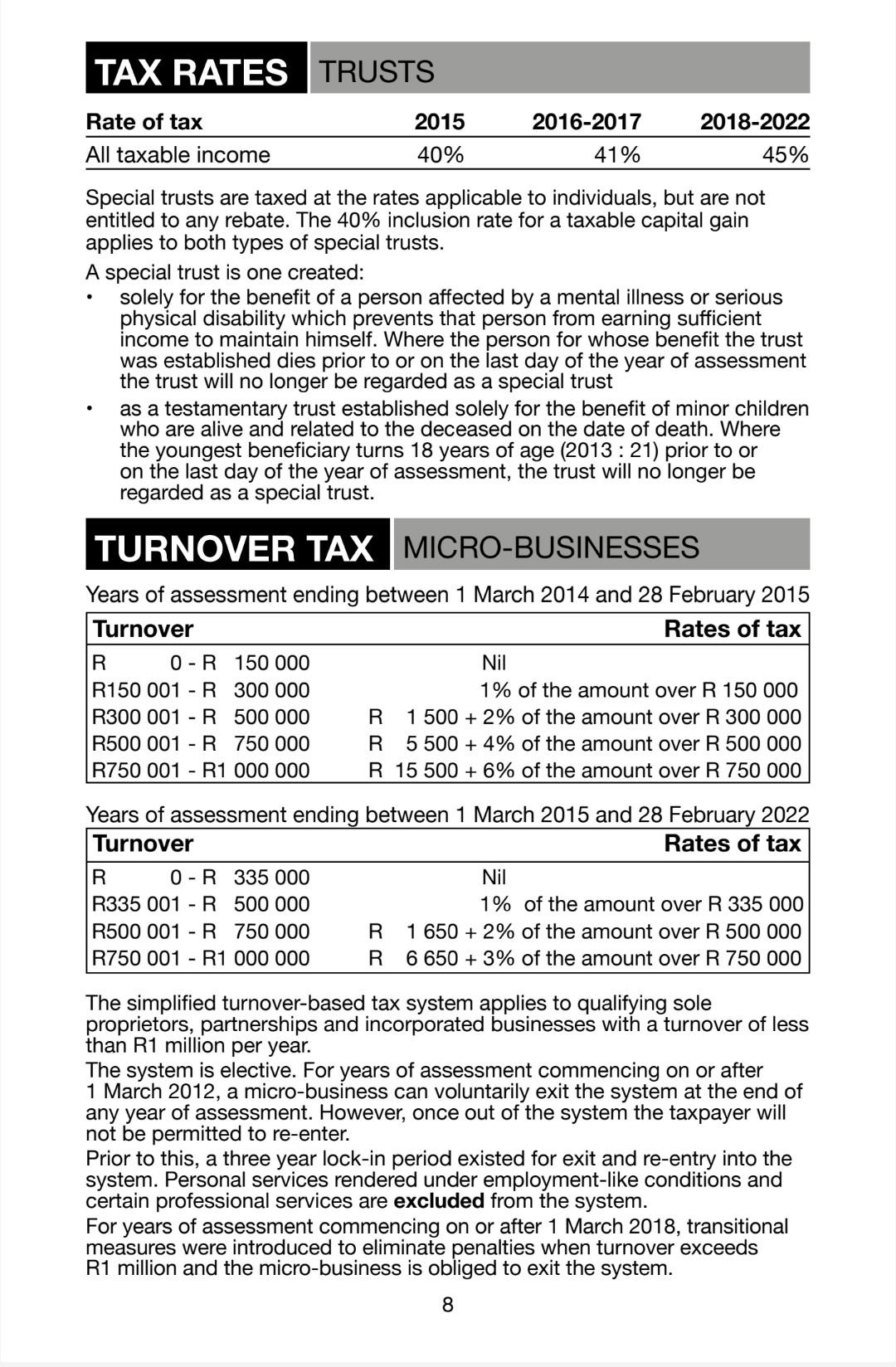

Question 3 (15 Marks) X and Y are in a partnership and their main business is the construction of houses. They share equally in the profits and losses of the partnership. The clients of the business are responsible for the purchase of building material. On a small scale they also offer clients a service of drafting plans for houses. They decided to register their business as a micro business for turnover tax purposes in the 2021 year of assessment. The following amounts relate to various amounts received by the micro business for that year: R Construction services 785 000 Drafting services 25 000 10 000 Government grant exempt from tax under section 12P 4 000 Proceeds from sale of business tools Interest earned on the business bank account 6 000 Refund received 4 500 Total income from business activities 834 500 Notes: 1. The refund received by the business relates to faulty equipment that was returned to the supplier. 2. The construction services figure includes an amount of R15 000 received from a client for a contract concluded in the previous year of assessment. The R15 000 had accrued to the business in the previous year of assessment and was subject to normal tax. Notes: 1. The refund received by the business relates to faulty equipment that was returned to the supplier. 2. The construction services figure includes an amount of R15 000 received from a client for a contract concluded in the previous year of assessment. The R15 000 had accrued to the business in the previous year of assessment and was subject to normal tax. 3. The construction figure also includes an amount of R50 000 from the carrying on of business activities in Lesotho. Required: Calculate the turnover tax payable for the 2021 year of assessment TAX RATES COMPANIES 35% 30% 29% 28% 27% Income Tax For years of assessment ending during the following periods: 1 April 1994 31 March 1999 1 April 1999 31 March 2005 1 April 2005 31 March 2008 1 April 2008 31 March 2022 1 April 2022 31 March 2023 SA Income Foreign Company/Branch Tax For years of assessment ending during the following periods: 1 April 1996 31 March 1999 1 April 1999 31 March 2005 1 April 2005 31 March 2008 1 April 2008 31 March 2012 1 April 2012 31 March 2022 40% 35% 34% 33% 28% 25% 12,5% 10% Secondary Tax on Companies Dividend declared between 22 June 1994 and 13 March 1996 Dividend declared between 14 March 1996 and 30 September 2007 Dividend declared between 1 October 2007 and 31 March 2012 Dividends Tax Dividend paid or becomes due and payable from 1 April 2012 Dividend paid or becomes due and payable from 22 February 2017 EFFECTIVE TAX RATE 15% 20% Tax year 2014 to 2016 2017 Prior to 22 Feb 2017 2017 From 22 Feb 2017 2018 to 2022 R R R R Taxable income Less: Normal tax Available for distribution Less: Dividend 100,00 28,00 72,00 72,00 100,00 28,00 72,00 72,00 0 100,00 28,00 72,00 72,00 0 100,00 28,00 72,00 72,00 0 Retained 0 Total tax Normal tax Dividends Tax 38,80 28,00 10,80 38,80% 38,80 28,00 10,80 38,80% 42,40 28,00 14,40 42,40% 42,40 28,00 14,40 42,40% Effective rate Assumes all profits are declared as a dividend. 6 TAX RATES INDIVIDUALS - 2021 Taxable income Rates of tax R 0 - R205 900 18% of each R1 R 205 901 - R 321 600 R 37 062 +26% of the amount over R 205 900 R 321 601 - R 445 100 R 67 144 + 31% of the amount over R 321 600 R 445 101 - R 584 200 R105 429 + 36% of the amount over R 445 100 R 584 201 - R 744 800 R155 505 + 39% of the amount over R 584 200 R 744 801 - R1 577 300 R218 139 + 41% of the amount over R 744 800 R1 577 301 + R559 464 + 45% of the amount over R1 577 300 TAX RATES INDIVIDUALS - 2022 Taxable income Rates of tax R 0 - R 216 200 18% of each R1 R 216 201 - R 337 800 R 38 916 +26% of the amount over R 216 200 R 337 801 - R 467 500 R 70 532 + 31% of the amount over R 337 800 R 467 501 - R 613 600 R110 739 + 36% of the amount over R 467 500 R613 601 - R 782 200 R163 335 + 39% of the amount over R 613 600 R 782 201 - R1 656 600 R229 089 +41% of the amount over R 782 200 R1 656 601 + R587 593 + 45% of the amount over R1 656 600 TAX THRESHOLDS Persons under 65 Persons 65 and under 75 Persons 75 and over Taxable income 2021 2022 R 83 100 R 87 300 R128 650 R135 150 R143 850 R151 100 TAX REBATES 2021 Amounts deductible from the tax payable Persons under 65 Persons 65 and under 75 Persons 75 and over R14 958 R23 157 R25 893 2022 R15 714 R24 327 R27 198 MEDICAL AID TAX CREDITS Monthly amounts deductible from tax payable 2021 2022 Main member R319 R332 Main member with one dependant R638 R664 Main member with two dependants R853 R888 Each additional dependant qualifies for a credit of R224 (2021 : R215) per month. 7 PKF TAX RATES TRUSTS Rate of tax 2016-2017 2015 40% 2018-2022 45% All taxable income 41% Special trusts are taxed at the rates applicable to individuals, but are not entitled to any rebate. The 40% inclusion rate for a taxable capital gain applies to both types of special trusts. A special trust is one created: solely for the benefit of a person affected by a mental illness or serious physical disability which prevents that person from earning sufficient income to maintain himself. Where the person for whose benefit the trust was established dies prior to or on the last day of the year of assessment the trust will no longer be regarded as a special trust as a testamentary trust established solely for the benefit of minor children who are alive and related to the deceased on the date of death. Where the youngest beneficiary turns 18 years of age (2013: 21) prior to or on the last day of the year of assessment, the trust will no longer be regarded as a special trust. TURNOVER TAX MICRO-BUSINESSES Years of assessment ending between 1 March 2014 and 28 February 2015 Turnover Rates of tax R 0-R150 000 Nil R150 001 - R300 000 1% of the amount over R 150 000 R300 001 - R500 000 R 1500 + 2% of the amount over R 300 000 R500 001 - R 750 000 R 5 500 + 4% of the amount over R 500 000 R750 001 - R1 000 000 R 15 500 + 6% of the amount over R 750 000 Years of assessment ending between 1 March 2015 and 28 February 2022 Turnover Rates of tax R 0 - R 335 000 Nil R335 001 - R500 000 1% of the amount over R 335 000 R500 001 - R 750 000 R 1 650 + 2% of the amount over R 500 000 R750 001 - R1 000 000 R 6 650 + 3% of the amount over R 750 000 The simplified turnover-based tax system applies to qualifying sole proprietors, partnerships and incorporated businesses with a turnover of less than R1 million per year. The system is elective. For years of assessment commencing on or after 1 March 2012, a micro-business can voluntarily exit the system at the end of any year of assessment. However, once out of the system the taxpayer will not be permitted to re-enter. Prior to this, a three year lock-in period existed for exit and re-entry into the system. Personal services rendered under employment-like conditions and certain professional services are excluded from the system. For years of assessment commencing on or after 1 March 2018, transitional measures were introduced to eliminate penalties when turnover exceeds R1 million and the micro-business is obliged to exit the system. 8

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Case Studies In Strategic ManagementHow Executive Input Enables Students Development

Authors: Gunther Friedl, Andreas Biagosch

1st Edition

3319955543, 9783319955544