Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Apple just issued US$200 million 10 year bond at PAR with an annual coupon of 2% attached with a 3 year warrants on Apple

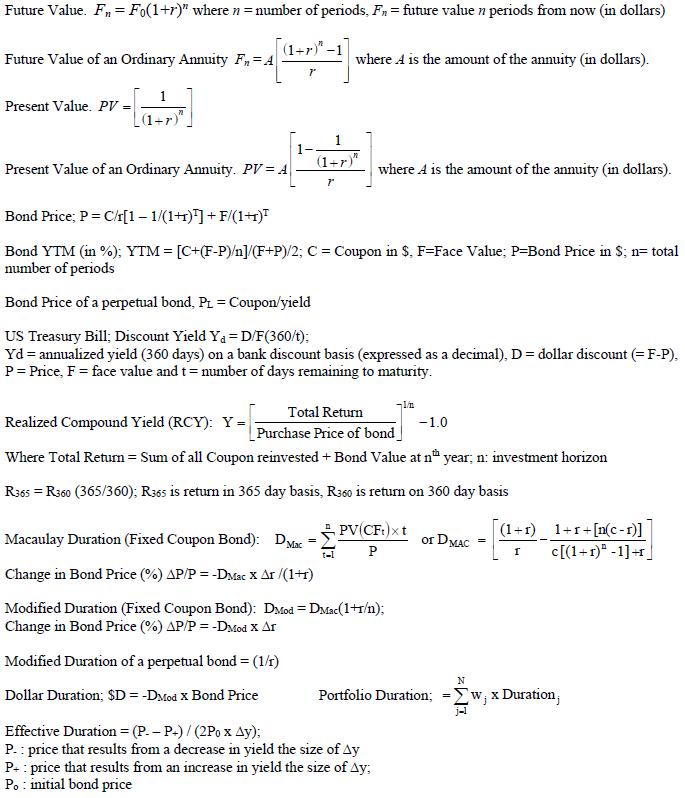

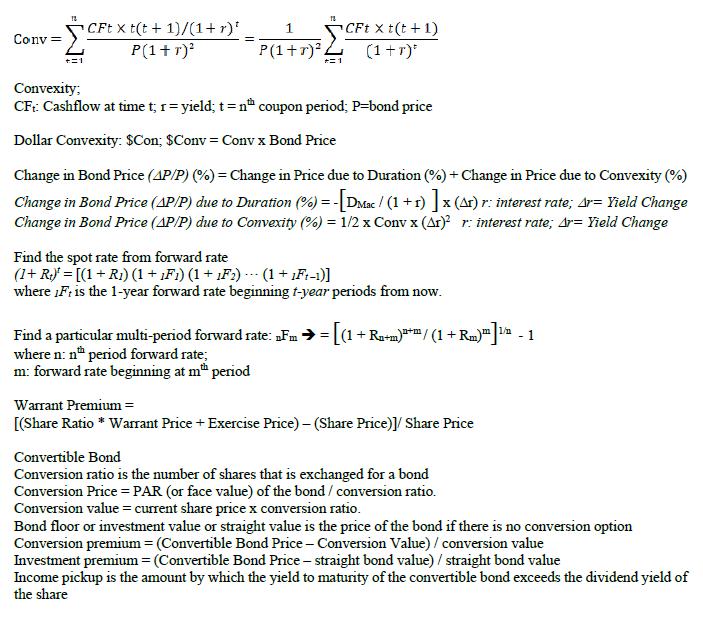

Apple just issued US$200 million 10 year bond at PAR with an annual coupon of 2% attached with a 3 year warrants on Apple shares. Each bond has a US$10,000 denomination and has 500 detachable warrants. 1 warrant allows bondholder to purchase one Apple share at an exercise price of US52. Currently the Apple share is quoted at US$40 and the Yield to Maturity (YTM) of a similar fixed coupon bond issued by Apple is 4%. (a) If the market has a standard that if a warrant has a premium greater than 20%, the warrant is then expensive. Given the issuance terms, would you recommend investors to buy this issue? Hint: Calculate the $ value per warrant to evaluation the warrant premium in %. (8 Marks) (b) At the same time as (a), Apple also issued a Convertible Bond (CB) with a zero coupon with a Conversion Price that gives the Conversion Premium the same Warrant Premium as Bond cum Warrant in (a). If investors have an extremely bullish view on Apple over the next 10 years, what would you recommend to investors between this CB and the "Bond with Warrants" described in (a). Explain the rationale between your recommendation. (2 Marks) (c) Apple is considered issuing a callable fixed coupon bond. The issuing terms are 6 year maturity with 8% annual coupon callable at year 3 and every year thereafter at a Call Price of $110. The issue price is at PAR with the yield to maturity (YTM) is 7%. A similar 6 year government bond yields 4%. If the call option part of this Callable Bond is valued at 7. The market has a comparable non callable fixed coupon bond by another issuer (EAF) that has a 3% YTM. Can you review the attractiveness of Apple callable bond's credit (or yield) spread comparing with the EAF bond? Hint: Analyze the Call Adjusted Yield spread (CAS) to assess. (5 Marks)- (d) An investor is assessing the Callable Bond in (c) with the market is expected the YTM to fall significantly. The investor wants to estimate the rough YTM level that Apple will call the bonds. Explain how the investor would work it out? (5 Marks) Future Value. F, = Fo(1+r)" where n = number of periods, Fn = future value n periods from now (in dollars) (1+r)"-1] Future Value of an Ordinary Annuity F, = A where A is the amount of the annuity (in dollars). Present Value. PV = (1+r) 1- (1+r)" Present Value of an Ordinary Annuity. PV = A where A is the amount of the annuity (in dollars). Bond Price; P = C/r[1 1/(1+1)] + F/(1+r)F Bond YTM (in %); YTM = [C+(F-P)/n]/(F+P)/2; C = Coupon in $. F=Face Value; P=Bond Price in S; n= total number of periods Bond Price of a perpetual bond, Pr = Coupon/yield US Treasury Bill; Discount Yield Ya = D/F(360/t); Yd = annualized yield (360 days) on a bank discount basis (expressed as a decimal), D= dollar discount (= F-P). P= Price, F = face value and t= number of days remaining to maturity. Total Return Realized Compound Yield (RCY): Y = -1.0 Purchase Price of bond_ Where Total Retum = Sum of all Coupon reinvested + Bond Value at n year; n: investment horizon R365 = R360 (365/360); R365 is return in 365 day basis, R360 is retum on 360 day basis [(1+r)_ 1+r+[n(c-1)] c[(1+r)" -1]-r] PV(CF:)xt Macaulay Duration (Fixed Coupon Bond): DMae or DMAC P Change in Bond Price (%) AP/P = -DMac x Ar /(1+1) Modified Duration (Fixed Coupon Bond): DMod = DMac(1+r/n); Change in Bond Price (%) AP/P = -Dcod X Ar Modified Duration of a perpetual bond = (1/t) N Dollar Duration; $D = -DMod X Bond Price Portfolio Duration; =Ew, x Duration, %3D Effective Duration = (P. - P-)/ (2Po x Ay): P. : price that results from a decrease in yield the size of Ay P. : price that results from an increase in yield the size of Ay; Po : initial bond price CFt X t(t + 1)/(1+r)' P(1+r) CFt X t(t +1) (1+r)* Conv %3D P(1+r), Convexity; CF: Cashflow at time t; 1= yield; t=n coupon period; P=bond price Dollar Convexity: $Con; $Conv = Conv x Bond Price Change in Bond Price (AP/P) (%) = Change in Price due to Duration (%) + Change in Price due to Convexity (%) Change in Bond Price (AP/P) due to Duration (%) = -[DMac / (1 + r) ]x (Ar) r: interest rate; Ar= Yield Change Change in Bond Price (AP/P) due to Convexity (%) = 1/2 x Conv x (Ar) r: interest rate; Ar= Yield Change Find the spot rate from forward rate (1+ R) = [(1 + R1) (1 + Fi) (1+ 1F1) - (1 + 1F:-1)] where iF: is the 1-year forward rate beginning t-year periods from now. Find a particular multi-period forward rate: Fm >= (1+ Ra+m)*/(1+Rm) where n: n period forward rate; m: forward rate beginning at m period m 1 Warrant Premium = [(Share Ratio * Warrant Price + Exercise Price) (Share Price)y Share Price Convertible Bond Conversion ratio is the number of shares that is exchanged for a bond Conversion Price = PAR (or face value) of the bond / conversion ratio. Conversion value = current share price x conversion ratio. Bond floor or investment value or straight value is the price of the bond if there is no conversion option Conversion premium = (Convertible Bond Price- Conversion Value) / conversion value Investment premium (Convertible Bond Price - straight bond value) / straight bond value Income pickup is the amount by which the yield to maturity of the convertible bond exceeds the dividend yield of the share

Step by Step Solution

★★★★★

3.54 Rating (157 Votes )

There are 3 Steps involved in it

Step: 1

a Calculation of Theoretical Market Price of bond at the ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Markets And Institutions

Authors: Frederic S. Mishkin, Stanley G. Eakins

7th Edition

013213683X, 978-0132136839