Answered step by step

Verified Expert Solution

Question

1 Approved Answer

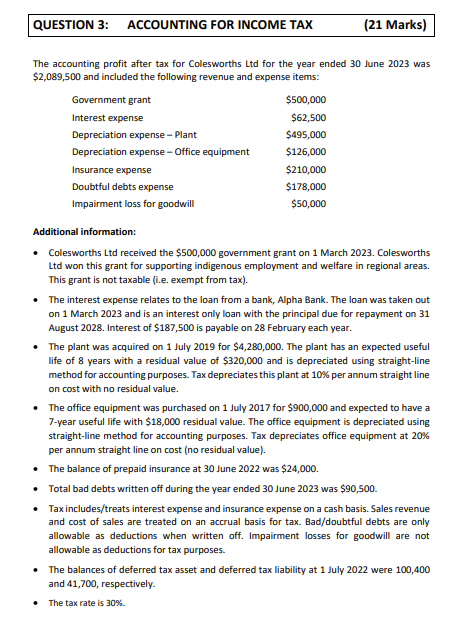

QUESTION 3: ACCOUNTING FOR INCOME TAX The accounting profit after tax for Colesworths Ltd for the year ended 30 June 2023 was $2,089,500 and

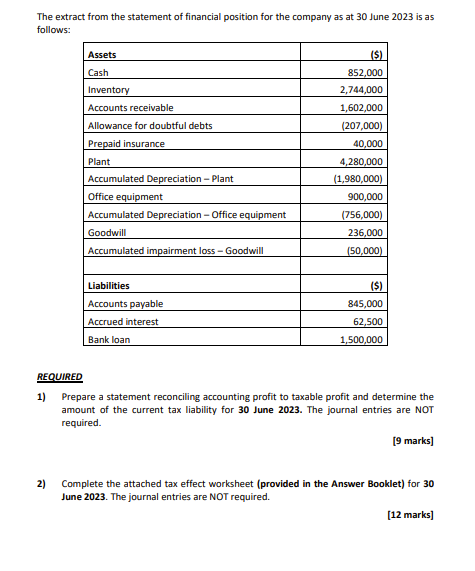

QUESTION 3: ACCOUNTING FOR INCOME TAX The accounting profit after tax for Colesworths Ltd for the year ended 30 June 2023 was $2,089,500 and included the following revenue and expense items: Government grant Interest expense Depreciation expense - Plant Depreciation expense - Office equipment Insurance expense Doubtful debts expense Impairment loss for goodwill $500,000 $62,500 $495,000 $126,000 $210,000 $178,000 $50,000 (21 Marks) Additional information: Colesworths Ltd received the $500,000 government grant on 1 March 2023. Colesworths Ltd won this grant for supporting indigenous employment and welfare in regional areas. This grant is not taxable (i.e. exempt from tax). The interest expense relates to the loan from a bank, Alpha Bank. The loan was taken out on 1 March 2023 and is an interest only loan with the principal due for repayment on 31 August 2028. Interest of $187,500 is payable on 28 February each year. The plant was acquired on 1 July 2019 for $4,280,000. The plant has an expected useful life of 8 years with a residual value of $320,000 and is depreciated using straight-line method for accounting purposes. Tax depreciates this plant at 10% per annum straight line on cost with no residual value. The office equipment was purchased on 1 July 2017 for $900,000 and expected to have a 7-year useful life with $18,000 residual value. The office equipment is depreciated using straight-line method for accounting purposes. Tax depreciates office equipment at 20% per annum straight line on cost (no residual value). The balance of prepaid insurance at 30 June 2022 was $24,000. Total bad debts written off during the year ended 30 June 2023 was $90,500. Tax includes/treats interest expense and insurance expense on a cash basis. Sales revenue and cost of sales are treated on an accrual basis for tax. Bad/doubtful debts are only allowable as deductions when written off. Impairment losses for goodwill are not allowable as deductions for tax purposes. The balances of deferred tax asset and deferred tax liability at 1 July 2022 were 100,400 and 41,700, respectively. The tax rate is 30%. The extract from the statement of financial position for the company as at 30 June 2023 is as follows: REQUIRED 1) 2) Assets Cash Inventory Accounts receivable Allowance for doubtful debts Prepaid insurance Plant Accumulated Depreciation - Plant Office equipment Accumulated Depreciation - Office equipment Goodwill Accumulated impairment loss - Goodwill Liabilities Accounts payable Accrued interest Bank loan ($) 852,000 2,744,000 1,602,000 (207,000) 40,000 4,280,000 (1,980,000) 900,000 (756,000) 236,000 (50,000) ($) 845,000 62,500 1,500,000 Prepare a statement reconciling accounting profit to taxable profit and determine the amount of the current tax liability for 30 June 2023. The journal entries are NOT required. [9 marks] Complete the attached tax effect worksheet (provided in the Answer Booklet) for 30 June 2023. The journal entries are NOT required. [12 marks]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

ANSWER 1 Reconciliation of Accounting Profit to Taxable Profit and Current Tax Liability Description ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting and Reporting

Authors: Barry Elliott, Jamie Elliott

14th Edition

978-0273744535, 273744445, 273744534, 978-0273744443