Answered step by step

Verified Expert Solution

Question

1 Approved Answer

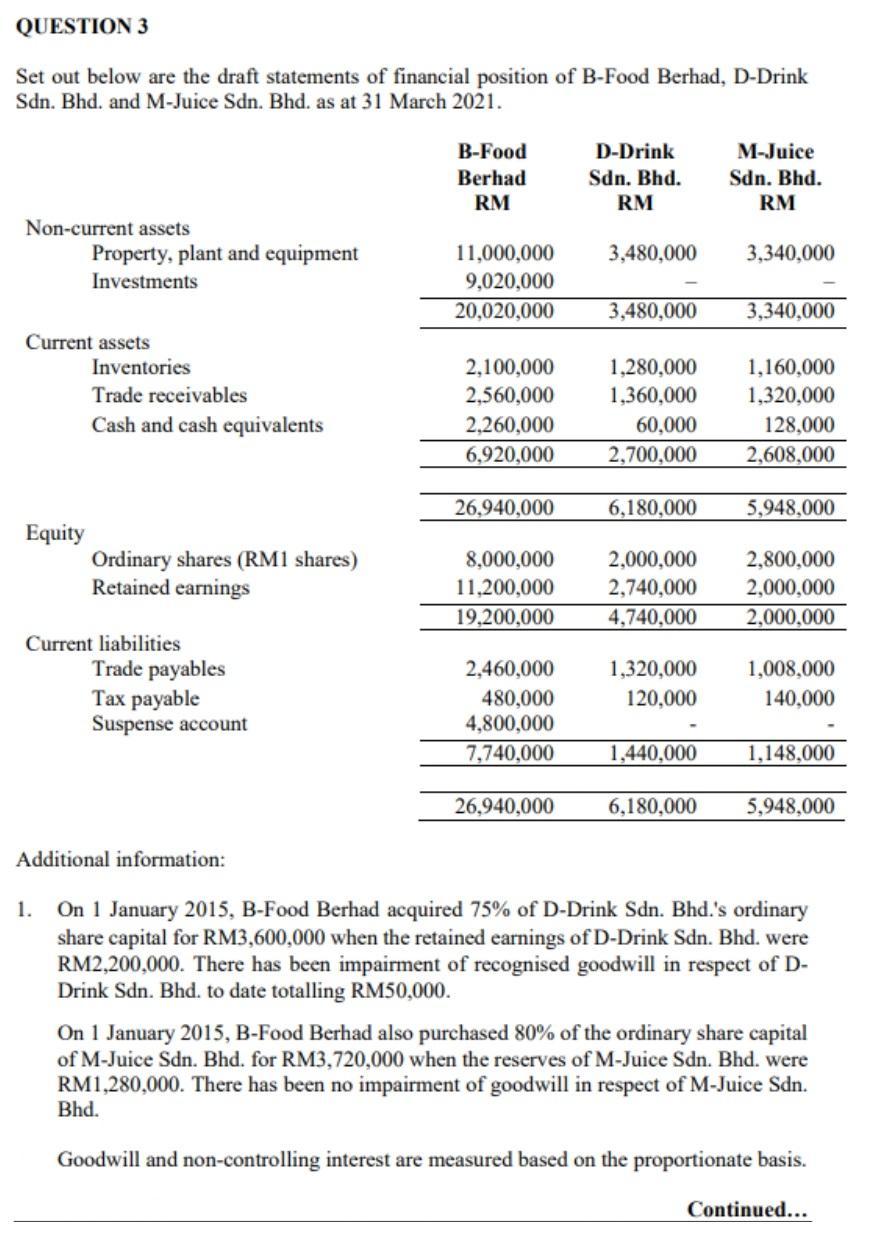

QUESTION 3 Set out below are the draft statements of financial position of B-Food Berhad, D-Drink Sdn. Bhd. and M-Juice Sdn. Bhd. as at

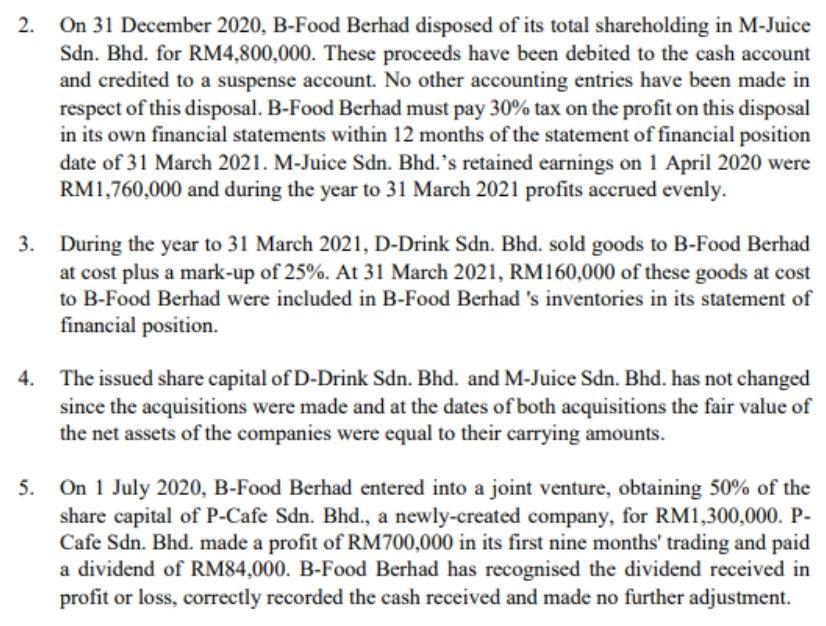

QUESTION 3 Set out below are the draft statements of financial position of B-Food Berhad, D-Drink Sdn. Bhd. and M-Juice Sdn. Bhd. as at 31 March 2021. B-Food D-Drink M-Juice Sdn. Bhd. Sdn. Bhd. Berhad RM RM RM Non-current assets Property, plant and equipment 11,000,000 3,480,000 3,340,000 Investments 9,020,000 20,020,000 3,480,000 3,340,000 Current assets Inventories 2,100,000 1,280,000 1,160,000 Trade receivables 2,560,000 1,360,000 1,320,000 Cash and cash equivalents 2,260,000 60,000 128,000 6,920,000 2,700,000 2,608,000 26,940,000 6,180,000 5,948,000 Ordinary shares (RM1 shares) 8,000,000 2,000,000 2,800,000 Retained earnings 11,200,000 2,740,000 2,000,000 19,200,000 4,740,000 2,000,000 Trade payables 2,460,000 1,320,000 1,008,000 480,000 120,000 140,000 Tax payable Suspense account 4,800,000 7,740,000 1,440,000 1,148,000 26,940,000 6,180,000 5,948,000 Additional information: 1. On 1 January 2015, B-Food Berhad acquired 75% of D-Drink Sdn. Bhd.'s ordinary share capital for RM3,600,000 when the retained earnings of D-Drink Sdn. Bhd. were RM2,200,000. There has been impairment of recognised goodwill in respect of D- Drink Sdn. Bhd. to date totalling RM50,000. On 1 January 2015, B-Food Berhad also purchased 80% of the ordinary share capital of M-Juice Sdn. Bhd. for RM3,720,000 when the reserves of M-Juice Sdn. Bhd. were RM1,280,000. There has been no impairment of goodwill in respect of M-Juice Sdn. Bhd. Goodwill and non-controlling interest are measured based on the proportionate basis. Continued... Equity Current liabilities 2. On 31 December 2020, B-Food Berhad disposed of its total shareholding in M-Juice Sdn. Bhd. for RM4,800,000. These proceeds have been debited to the cash account and credited to a suspense account. No other accounting entries have been made in respect of this disposal. B-Food Berhad must pay 30% tax on the profit on this disposal in its own financial statements within 12 months of the statement of financial position date of 31 March 2021. M-Juice Sdn. Bhd.'s retained earnings on 1 April 2020 were RM1,760,000 and during the year to 31 March 2021 profits accrued evenly. 3. During the year to 31 March 2021, D-Drink Sdn. Bhd. sold goods to B-Food Berhad at cost plus a mark-up of 25%. At 31 March 2021, RM160,000 of these goods at cost to B-Food Berhad were included in B-Food Berhad 's inventories in its statement of financial position. 4. The issued share capital of D-Drink Sdn. Bhd. and M-Juice Sdn. Bhd. has not changed since the acquisitions were made and at the dates of both acquisitions the fair value of the net assets of the companies were equal to their carrying amounts. 5. On 1 July 2020, B-Food Berhad entered into a joint venture, obtaining 50% of the share capital of P-Cafe Sdn. Bhd., a newly-created company, for RM1,300,000. P- Cafe Sdn. Bhd. made a profit of RM700,000 in its first nine months' trading and paid a dividend of RM84,000. B-Food Berhad has recognised the dividend received in profit or loss, correctly recorded the cash received and made no further adjustment. Required: a) Compute the gain or loss on disposal after tax of the investment in M-Juice Sdn. Bhd. that will be shown in: i) B-Food Berhad's separate financial statements

Step by Step Solution

★★★★★

3.39 Rating (158 Votes )

There are 3 Steps involved in it

Step: 1

Assuming that the tax rate is 30 the gain or loss is Gain or loss on disposal of investment ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting for Decision Makers

Authors: Peter Atrill, Eddie McLaney

6th Edition

273763451, 273763458, 978-0273763451