Answered step by step

Verified Expert Solution

Question

1 Approved Answer

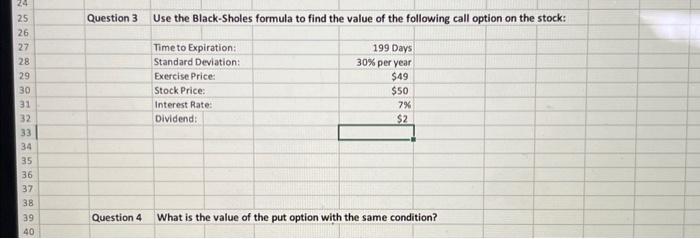

Question 3 Use the Black-Sholes formula to find the value of the following call option on the stock: begin{tabular}{|l|r|} hline Time to Expiration: & 199

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Coping With Financial Accounting 1 For Senior Secondary Schools And Undergraduate Studies

Authors: Festus Chukwunwendu Akpotohwo ,Stella Alfred-Jaja Wellington-Igonibo ,Cletus Ogeibiri

1st Edition

3659611034, 978-3659611032