Question

Question 3(10 marks) Suppose that the risk-free rate is 12% p.a. compounded continuously. The current price ( S 0 ) of a stock is $15.

Question 3(10 marks)

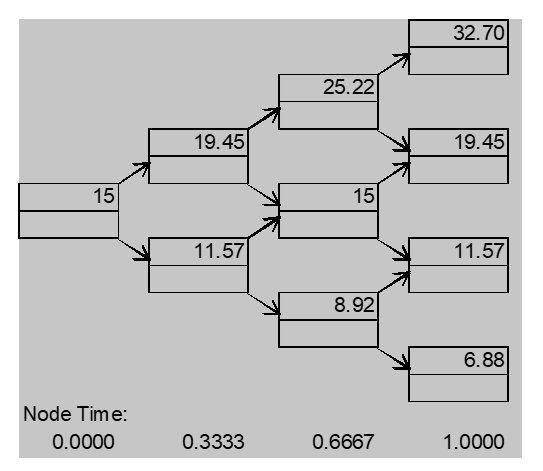

Suppose that the risk-free rate is 12% p.a. compounded continuously. The current price (S0) of a stock is $15. We model the evolution of the stock prices using a 3-step Binomial tree approach. In reality, over any four-month period, there is a 60% chance that the stock price will rise by 29.67% and a 40% chance that the stock price will fall by 22.88%. This is illustrated in the figure attached:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Price theory and applications

Authors: Steven E landsburg

8th edition

538746459, 1133008321, 780538746458, 9781133008323, 978-0538746458