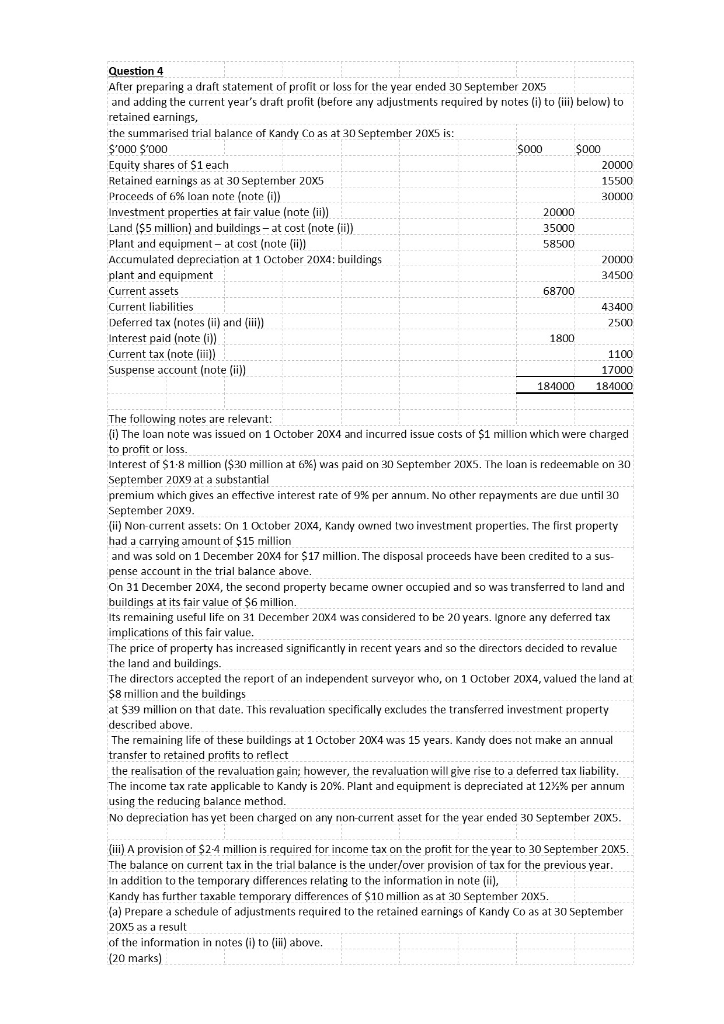

Question 4 After preparing a draft statement of profit and adding the current year's draft profit (before any adjustments required by notes (i) to (iii) below) to r loss for the year ended 30 September 20X5 retained earnings, the summarised trial balance of Kandy Co as at 30 September 20X5 is $000 $000 000.S 000.S Equity shares of $1 each Retained earnings as at 30 September 20X5 Proceeds of 6 % loan note ( note (i) Investment properties at fair value (note (ii)) Land ($5 million) and buildings-at cost (note (ii) Plant and equipment at cost (note (ii) Accumulated depreciation at 1 October 20X4: buildings 20000 15500 30000 20000 35000 58500 20000 plant and equipment 34500 68700 Current assets Current liabilities 43400 Deferred tax (notes (ii) and (ii) Interest paid (note (i)) Current tax (note (ii) Suspense account (note (ii) 2500 1800 1100 17000 184000 184000 The following notes are relevant: i The loan note was issued on 1 October 20x4 and incurred issue costs of $1 million which were chareed to proft or lo5s. million ($30 million 6%) was paid on 30 September 20X5. The loan is redeemable on 30 Interest of $1 September 20x9 at a substantial premium which gives an effective interest rate of 9% per annum. No other repayments are due until 30 September 20X9. (ii) Non-current assets: On 1 October 20X4, Kandy owned two investment properties. The first property 1 December 20X4 for $17 million. The disposal proceeds have been credited to a sus- pense account in the trial balance above. On 31 December 20X4, the second property became owner occupied and so was transferred to land and buildings at its fair value of $6 million. Its remaining useful life on 31 December 20x4 was considered to be 20 years. Ignore any deferred tax implications of this fair value. The price of property has increased significantly in recent years and the land and buildings. the directors decided to revalue The directors accepted the report of an independent surveyor who, on 1 October 20X4, valued the land at: $8 million and the buildings at $39 million on that date. This revaluation specifically excludes the transferred investment property described above. The remaining life of these buildings at 1October 20x4 was 15 years. Kandy does not make an annual transfer to retained protits to reflect the realisation of the revaluation gain; however, the revaluation will give rise to a deferred tax liability. The income tax rate applicable to Kandy is 20 %. Plant and equipment is depreciated at 12% % per annum using the reducing balance method. No depreciation has yet been charged on any non-current asset for the year ended 30 September 20x5. ii)A provision of $2-4 million is required for income tax on the profit for the year to 30 September 20X5. The balance on current tax in the trial balance is the under/over provision of tax for the previous year. In addition to the temporary differences relating to the information in note (i) Kandy has further taxable temporary differences of $10 million as at 30 September 20X5 a) Prepare a schedule adjustments required to the retained earnings of Kandy Co as at 30 September 20X5 as a result of the information in notes (i) to (iii) above. (20 marks) Question 4 After preparing a draft statement of profit and adding the current year's draft profit (before any adjustments required by notes (i) to (iii) below) to r loss for the year ended 30 September 20X5 retained earnings, the summarised trial balance of Kandy Co as at 30 September 20X5 is $000 $000 000.S 000.S Equity shares of $1 each Retained earnings as at 30 September 20X5 Proceeds of 6 % loan note ( note (i) Investment properties at fair value (note (ii)) Land ($5 million) and buildings-at cost (note (ii) Plant and equipment at cost (note (ii) Accumulated depreciation at 1 October 20X4: buildings 20000 15500 30000 20000 35000 58500 20000 plant and equipment 34500 68700 Current assets Current liabilities 43400 Deferred tax (notes (ii) and (ii) Interest paid (note (i)) Current tax (note (ii) Suspense account (note (ii) 2500 1800 1100 17000 184000 184000 The following notes are relevant: i The loan note was issued on 1 October 20x4 and incurred issue costs of $1 million which were chareed to proft or lo5s. million ($30 million 6%) was paid on 30 September 20X5. The loan is redeemable on 30 Interest of $1 September 20x9 at a substantial premium which gives an effective interest rate of 9% per annum. No other repayments are due until 30 September 20X9. (ii) Non-current assets: On 1 October 20X4, Kandy owned two investment properties. The first property 1 December 20X4 for $17 million. The disposal proceeds have been credited to a sus- pense account in the trial balance above. On 31 December 20X4, the second property became owner occupied and so was transferred to land and buildings at its fair value of $6 million. Its remaining useful life on 31 December 20x4 was considered to be 20 years. Ignore any deferred tax implications of this fair value. The price of property has increased significantly in recent years and the land and buildings. the directors decided to revalue The directors accepted the report of an independent surveyor who, on 1 October 20X4, valued the land at: $8 million and the buildings at $39 million on that date. This revaluation specifically excludes the transferred investment property described above. The remaining life of these buildings at 1October 20x4 was 15 years. Kandy does not make an annual transfer to retained protits to reflect the realisation of the revaluation gain; however, the revaluation will give rise to a deferred tax liability. The income tax rate applicable to Kandy is 20 %. Plant and equipment is depreciated at 12% % per annum using the reducing balance method. No depreciation has yet been charged on any non-current asset for the year ended 30 September 20x5. ii)A provision of $2-4 million is required for income tax on the profit for the year to 30 September 20X5. The balance on current tax in the trial balance is the under/over provision of tax for the previous year. In addition to the temporary differences relating to the information in note (i) Kandy has further taxable temporary differences of $10 million as at 30 September 20X5 a) Prepare a schedule adjustments required to the retained earnings of Kandy Co as at 30 September 20X5 as a result of the information in notes (i) to (iii) above. (20 marks)