Answered step by step

Verified Expert Solution

Question

1 Approved Answer

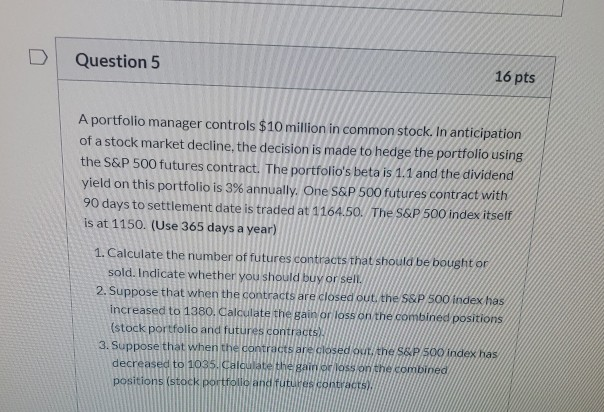

Question 5 16 pts A portfolio manager controls $10 million in common stock. In anticipation of a stock market decline, the decision is made to

Question 5 16 pts A portfolio manager controls $10 million in common stock. In anticipation of a stock market decline, the decision is made to hedge the portfolio using the S&P 500 futures contract. The portfolio's beta is 1.1 and the dividend yield on this portfolio is 3% annually. One S&P 500 futures contract with 90 days to settlement date is traded at 1164.50. The S&P 500 index itself is at 1150. (Use 365 days a year) 1. Calculate the number of futures contracts that should be bought on sold. Indicate whether you should buy or sell. 2. Suppose that when the contracts are closed out the S&P 500 index has increased to 1380. Calculate the gain or loss on the combined positions (stock portfolio and futures contracts) 3. Suppose that when the contracts are closed out, the S&P 500 index has decreased to 1035. Calculate the gain or loss on the combined positions (stock portfolio and future contracts)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Market Audit And Analysis

Authors: Nicole Lorat

1st Edition

3640438892, 978-3640438891