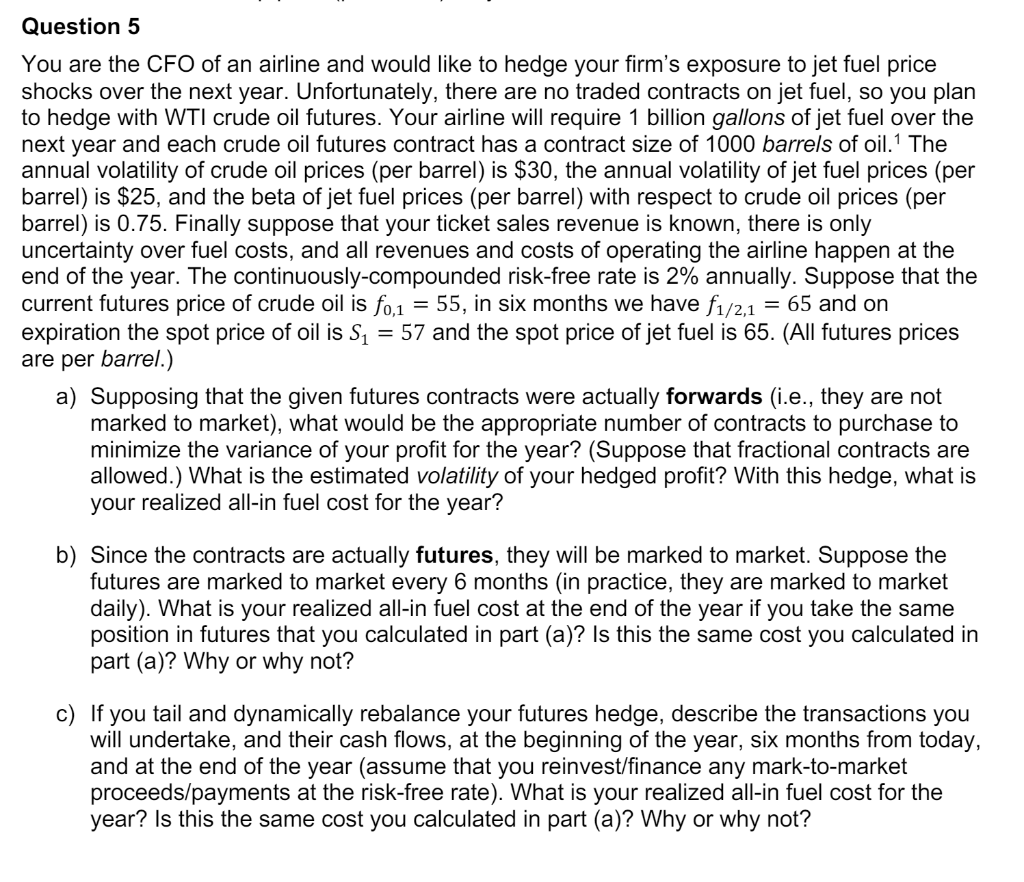

Question 5 You are the CFO of an airline and would like to hedge your firm's exposure to jet fuel price shocks over the next year. Unfortunately, there are no traded contracts on jet fuel, so you plan to hedge with WTI crude oil futures. Your airline will require 1 billion gallons of jet fuel over the next year and each crude oil futures contract has a contract size of 1000 barrels of oil. The annual volatility of crude oil prices (per barrel) is $30, the annual volatility of jet fuel prices (per barrel) is $25, and the beta of jet fuel prices (per barrel) with respect to crude oil prices (per barrel) is 0.75. Finally suppose that your ticket sales revenue is known, there is only uncertainty over fuel costs, and all revenues and costs of operating the airline happen at the end of the year. The continuously-compounded risk-free rate is 2% annually. Suppose that the current futures price of crude oil is f0,1 = 55, in six months we have f1/2,1 = 65 and on expiration the spot price of oil is S1 = 57 and the spot price of jet fuel is 65. (All futures prices are per barrel.) a) Supposing that the given futures contracts were actually forwards (i.e., they are not marked to market), what would be the appropriate number of contracts to purchase to minimize the variance of your profit for the year? (Suppose that fractional contracts are allowed.) What is the estimated volatility of your hedged profit? With this hedge, what is your realized all-in fuel cost for the year? b) Since the contracts are actually futures, they will be marked to market. Suppose the futures are marked to market every 6 months (in practice, they are marked to market daily). What is your realized all-in fuel cost at the end of the year if you take the same position in futures that you calculated in part (a)? Is this the same cost you calculated in part (a)? Why or why not? c) If you tail and dynamically rebalance your futures hedge, describe the transactions you will undertake, and their cash flows, at the beginning of the year, six months from today, and at the end of the year (assume that you reinvest/finance any mark-to-market proceeds/payments at the risk-free rate). What is your realized all-in fuel cost for the year? Is this the same cost you calculated in part (a)? Why or why not? Question 5 You are the CFO of an airline and would like to hedge your firm's exposure to jet fuel price shocks over the next year. Unfortunately, there are no traded contracts on jet fuel, so you plan to hedge with WTI crude oil futures. Your airline will require 1 billion gallons of jet fuel over the next year and each crude oil futures contract has a contract size of 1000 barrels of oil. The annual volatility of crude oil prices (per barrel) is $30, the annual volatility of jet fuel prices (per barrel) is $25, and the beta of jet fuel prices (per barrel) with respect to crude oil prices (per barrel) is 0.75. Finally suppose that your ticket sales revenue is known, there is only uncertainty over fuel costs, and all revenues and costs of operating the airline happen at the end of the year. The continuously-compounded risk-free rate is 2% annually. Suppose that the current futures price of crude oil is f0,1 = 55, in six months we have f1/2,1 = 65 and on expiration the spot price of oil is S1 = 57 and the spot price of jet fuel is 65. (All futures prices are per barrel.) a) Supposing that the given futures contracts were actually forwards (i.e., they are not marked to market), what would be the appropriate number of contracts to purchase to minimize the variance of your profit for the year? (Suppose that fractional contracts are allowed.) What is the estimated volatility of your hedged profit? With this hedge, what is your realized all-in fuel cost for the year? b) Since the contracts are actually futures, they will be marked to market. Suppose the futures are marked to market every 6 months (in practice, they are marked to market daily). What is your realized all-in fuel cost at the end of the year if you take the same position in futures that you calculated in part (a)? Is this the same cost you calculated in part (a)? Why or why not? c) If you tail and dynamically rebalance your futures hedge, describe the transactions you will undertake, and their cash flows, at the beginning of the year, six months from today, and at the end of the year (assume that you reinvest/finance any mark-to-market proceeds/payments at the risk-free rate). What is your realized all-in fuel cost for the year? Is this the same cost you calculated in part (a)? Why or why not