Answered step by step

Verified Expert Solution

Question

1 Approved Answer

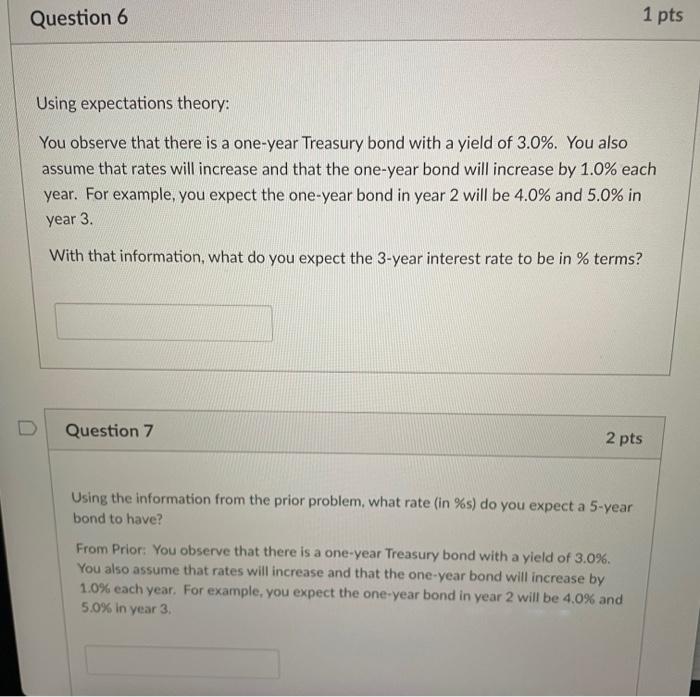

Question 6 Using expectations theory: You observe that there is a one-year Treasury bond with a yield of 3.0%. You also assume that rates will

Question 6 Using expectations theory: You observe that there is a one-year Treasury bond with a yield of 3.0%. You also assume that rates will increase and that the one-year bond will increase by 1.0% each year. For example, you expect the one-year bond in year 2 will be 4.0% and 5.0% in year 3. With that information, what do you expect the 3-year interest rate to be in % terms? Question 7 2 pts Using the information from the prior problem, what rate (in %s) do you expect a 5-year bond to have? 1 pts From Prior: You observe that there is a one-year Treasury bond with a yield of 3.0%. You also assume that rates will increase and that the one-year bond will increase by 1.0% each year. For example, you expect the one-year bond in year 2 will be 4.0% and 5.0% in year 3.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Tidy Finance With R

Authors: Christoph Scheuch, Stefan Voigt, Patrick Weiss

1st Edition

1032389346, 978-1032389349