Answered step by step

Verified Expert Solution

Question

1 Approved Answer

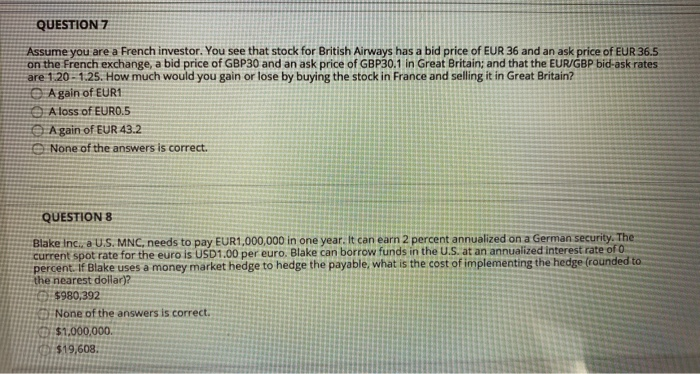

QUESTION 7 Assume you are a French investor. You see that stock for British Airways has a bid price of EUR 36 and an ask

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Short Term Rental Success Guide From Host To Hospitality Expert

Authors: Alexandra Hartwell

1st Edition

979-8860876309