Answered step by step

Verified Expert Solution

Question

1 Approved Answer

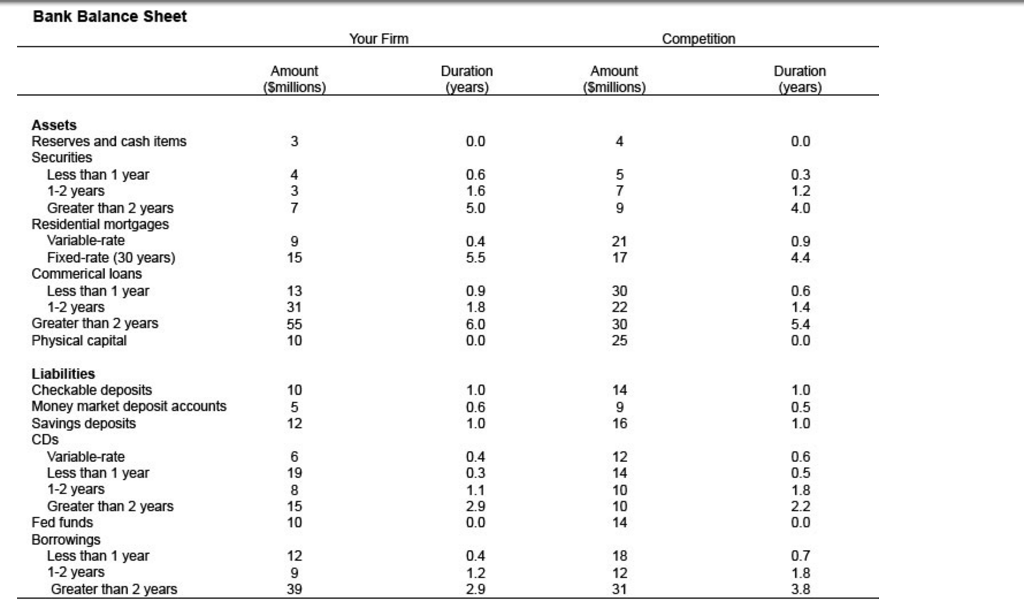

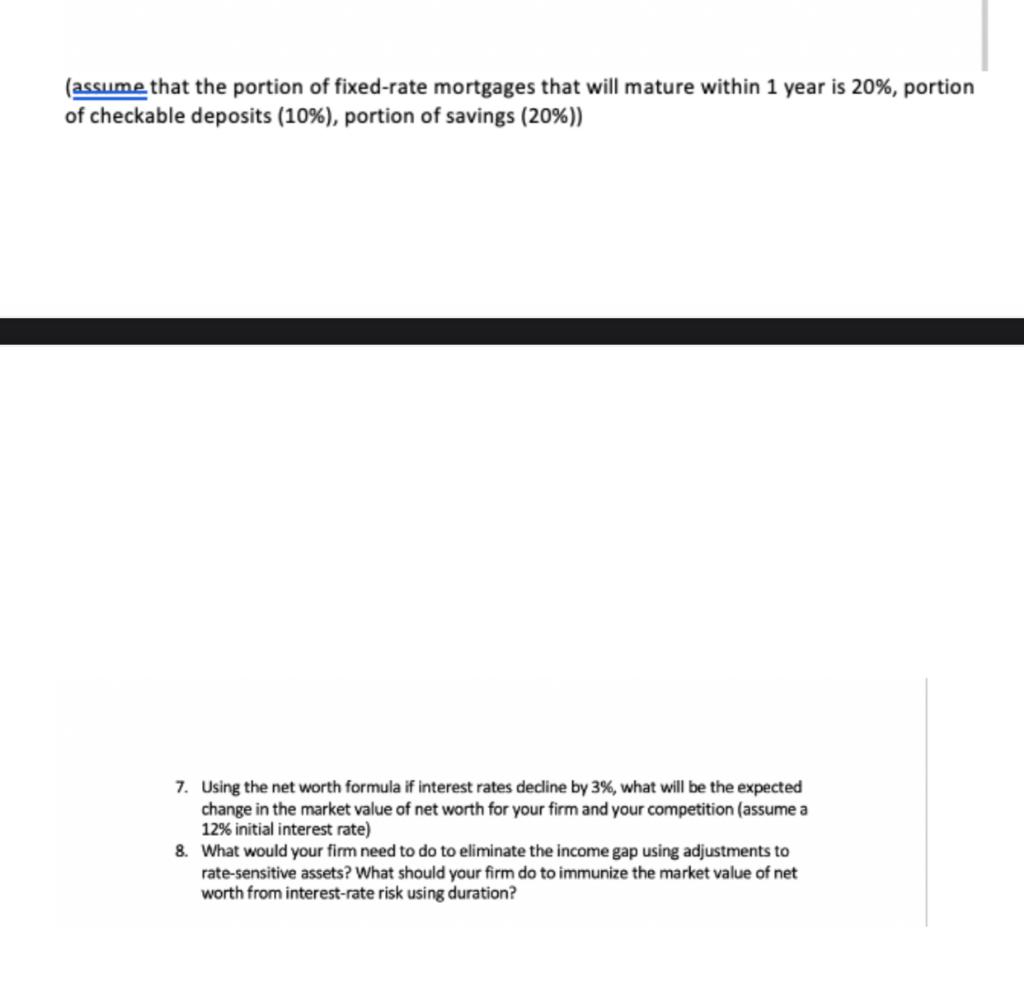

Question 7 PLZ Bank Balance Sheet Assets Reserves and cash items Securities Less than 1 year 1-2 years Greater than 2 years Residential mortgages Variable-rate

Question 7 PLZ

Bank Balance Sheet Assets Reserves and cash items Securities Less than 1 year 1-2 years Greater than 2 years Residential mortgages Variable-rate Fixed-rate (30 years) Commerical loans Less than 1 year 1-2 years Greater than 2 years Physical capital Liabilities Checkable deposits Money market deposit accounts Savings deposits CDS Variable-rate Less than 1 year 1-2 years Greater than 2 years Less than 1 year 1-2 years Greater than 2 years Fed funds Borrowings Amount (Smillions) 3 437 9 15 13 31 55 10 10 5 12 6 19 8 15 10 12 9 39 Your Firm Duration (years) 0.0 0.6 1.6 5.0 0.4 5.5 0.9 1.8 6.0 0.0 1.0 0.6 1.0 0.4 0.3 1.1 2.9 0.0 0.4 1.2 2.9 Amount (Smillions) 4 5 7 9 21 17 30 22 30 25 14 9 16 12 14 10 10 14 18 12 31 Competition Duration (years) 0.0 0.3 1.2 4.0 0.9 4.4 0.6 1.4 5.4 0.0 1.0 0.5 1.0 0.6 0.5 1.8 2.2 0.0 0.7 1.8 3.8 (assume that the portion of fixed-rate mortgages that will mature within 1 year is 20%, portion of checkable deposits (10%), portion of savings (20%)) 7. Using the net worth formula if interest rates decline by 3%, what will be the expected change in the market value of net worth for your firm and your competition (assume a 12% initial interest rate) 8. What would your firm need to do to eliminate the income gap using adjustments to rate-sensitive assets? What should your firm do to immunize the market value of net worth from interest-rate risk using duration? Bank Balance Sheet Assets Reserves and cash items Securities Less than 1 year 1-2 years Greater than 2 years Residential mortgages Variable-rate Fixed-rate (30 years) Commerical loans Less than 1 year 1-2 years Greater than 2 years Physical capital Liabilities Checkable deposits Money market deposit accounts Savings deposits CDS Variable-rate Less than 1 year 1-2 years Greater than 2 years Less than 1 year 1-2 years Greater than 2 years Fed funds Borrowings Amount (Smillions) 3 437 9 15 13 31 55 10 10 5 12 6 19 8 15 10 12 9 39 Your Firm Duration (years) 0.0 0.6 1.6 5.0 0.4 5.5 0.9 1.8 6.0 0.0 1.0 0.6 1.0 0.4 0.3 1.1 2.9 0.0 0.4 1.2 2.9 Amount (Smillions) 4 5 7 9 21 17 30 22 30 25 14 9 16 12 14 10 10 14 18 12 31 Competition Duration (years) 0.0 0.3 1.2 4.0 0.9 4.4 0.6 1.4 5.4 0.0 1.0 0.5 1.0 0.6 0.5 1.8 2.2 0.0 0.7 1.8 3.8 (assume that the portion of fixed-rate mortgages that will mature within 1 year is 20%, portion of checkable deposits (10%), portion of savings (20%)) 7. Using the net worth formula if interest rates decline by 3%, what will be the expected change in the market value of net worth for your firm and your competition (assume a 12% initial interest rate) 8. What would your firm need to do to eliminate the income gap using adjustments to rate-sensitive assets? What should your firm do to immunize the market value of net worth from interest-rate risk using durationStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Chains Of Finance How Investment Management Is Shaped

Authors: Diane-Laure Arjalies, Philip Grant, Iain Hardie, Donald MacKenzie, Ekaterina Svetlova

1st Edition

0198802943, 978-0198802945