Answered step by step

Verified Expert Solution

Question

1 Approved Answer

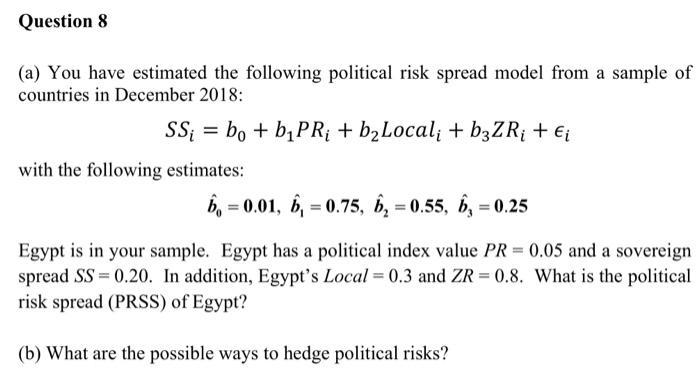

Question 8 (a) You have estimated the following political risk spread model from a sample of countries in December 2018: SS = bo +

Question 8 (a) You have estimated the following political risk spread model from a sample of countries in December 2018: SS = bo + bPR + b Local + b3ZR + Ei with the following estimates: b=0.01, 6, = 0.75, 6, = 0.55, 6, = 0.25 Egypt is in your sample. Egypt has a political index value PR = 0.05 and a sovereign spread SS=0.20. In addition, Egypt's Local = 0.3 and ZR=0.8. What is the political risk spread (PRSS) of Egypt? (b) What are the possible ways to hedge political risks?

Step by Step Solution

★★★★★

3.46 Rating (162 Votes )

There are 3 Steps involved in it

Step: 1

a The political risk spread PRSS of Egypt is 021 This can be calculated by plugging in the values for SS PR Local and ZR into the estimated model PRSS ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Theory and Corporate Policy

Authors: Thomas E. Copeland, J. Fred Weston, Kuldeep Shastri

4th edition

321127218, 978-0321179548, 321179544, 978-0321127211