Answered step by step

Verified Expert Solution

Question

1 Approved Answer

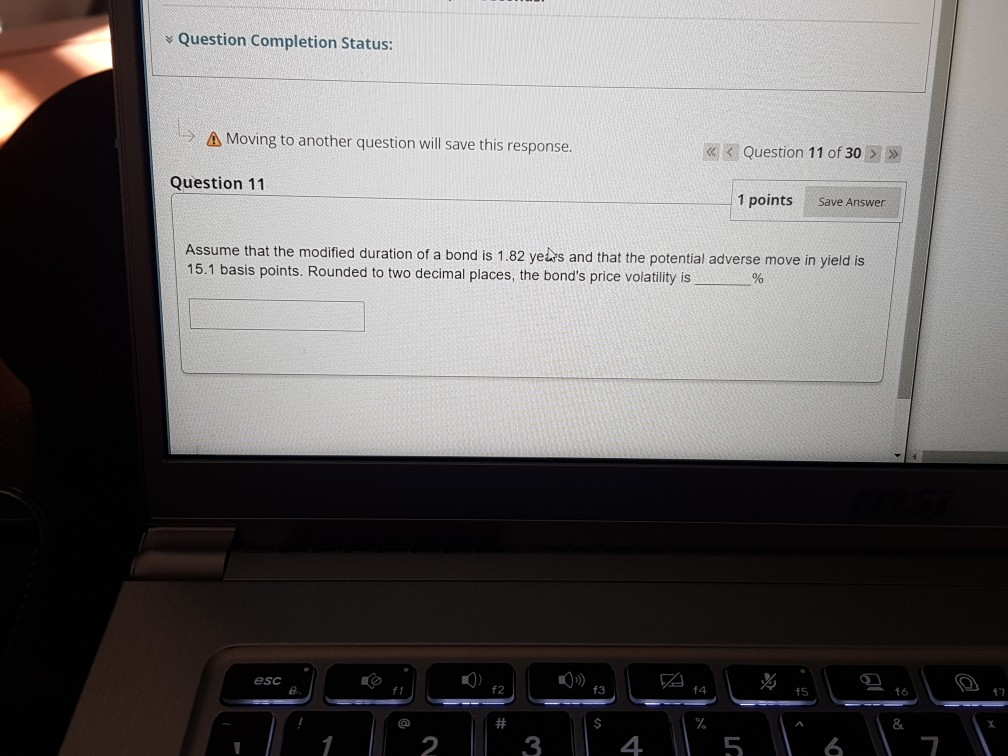

Question Completion Status: A Moving to another question will save this response. >> Question 11 1 points Save Answer Assume that the modified duration of

Question Completion Status: A Moving to another question will save this response. >> Question 11 1 points Save Answer Assume that the modified duration of a bond is 1.82 years and that the potential adverse move in yield is 15.1 basis points. Rounded to two decimal places, the bond's price volatility is % esc 11 f2 13 14 15 7 # 5

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Ultra High Net Worth Bankers Handbook

Authors: Heinrich Weber, Stephan Meier

1st Edition

1905641753, 978-1905641758