Answered step by step

Verified Expert Solution

Question

1 Approved Answer

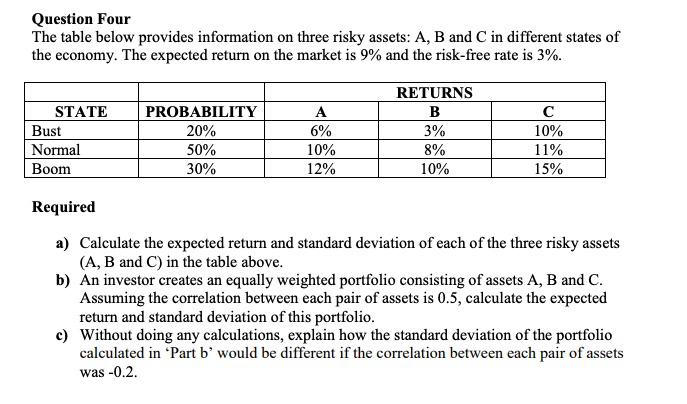

Question Four The table below provides information on three risky assets: A,B and C in different states of the economy. The expected return on the

Question Four The table below provides information on three risky assets: A,B and C in different states of the economy. The expected return on the market is 9% and the risk-free rate is 3%. Required a) Calculate the expected return and standard deviation of each of the three risky assets (A,B and C) in the table above. b) An investor creates an equally weighted portfolio consisting of assets A,B and C. Assuming the correlation between each pair of assets is 0.5 , calculate the expected return and standard deviation of this portfolio. c) Without doing any calculations, explain how the standard deviation of the portfolio calculated in 'Part b ' would be different if the correlation between each pair of assets was -0.2

Question Four The table below provides information on three risky assets: A,B and C in different states of the economy. The expected return on the market is 9% and the risk-free rate is 3%. Required a) Calculate the expected return and standard deviation of each of the three risky assets (A,B and C) in the table above. b) An investor creates an equally weighted portfolio consisting of assets A,B and C. Assuming the correlation between each pair of assets is 0.5 , calculate the expected return and standard deviation of this portfolio. c) Without doing any calculations, explain how the standard deviation of the portfolio calculated in 'Part b ' would be different if the correlation between each pair of assets was -0.2 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Multinational Business Finance

Authors: David K. Eiteman, Arthur I. Stonehill, Michael H. Moffett

12th Edition

0136096689, 978-0136096689