Answered step by step

Verified Expert Solution

Question

1 Approved Answer

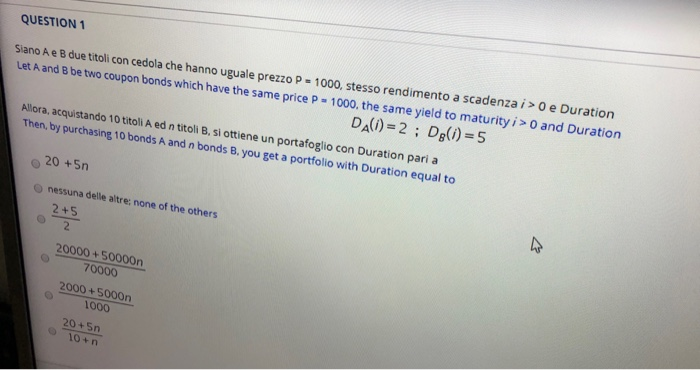

question is marked by blue. QUESTION 1 Siano A e B due titoli con cedola che hanno uguale prezzo P = 1000, stesso rendimento a

question is marked by blue.

question is marked by blue.Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Modern Auditing

Authors: Guadarshan S. Gill, Cosserat Graham, Leung Philomena, Coram Paul

5th Edition

0471340723, 978-0471340720