Question

QUESTION: PLEASE ANSWER THIS QUESTION AND EXPLAIN. I HAVE TRIED THIS QUESTION 6 TIMES AND HAVE GOTTEN THE WRONG ANSWER EACH TIME. THE CURRENT ANSWER

QUESTION:

PLEASE ANSWER THIS QUESTION AND EXPLAIN. I HAVE TRIED THIS QUESTION 6 TIMES AND HAVE GOTTEN THE WRONG ANSWER EACH TIME.

THE CURRENT ANSWER I HAVE IS $13,984. Please show me what I am doing wrong using the parameters I am using. T should equal 30. t=30?

FORMULAS:

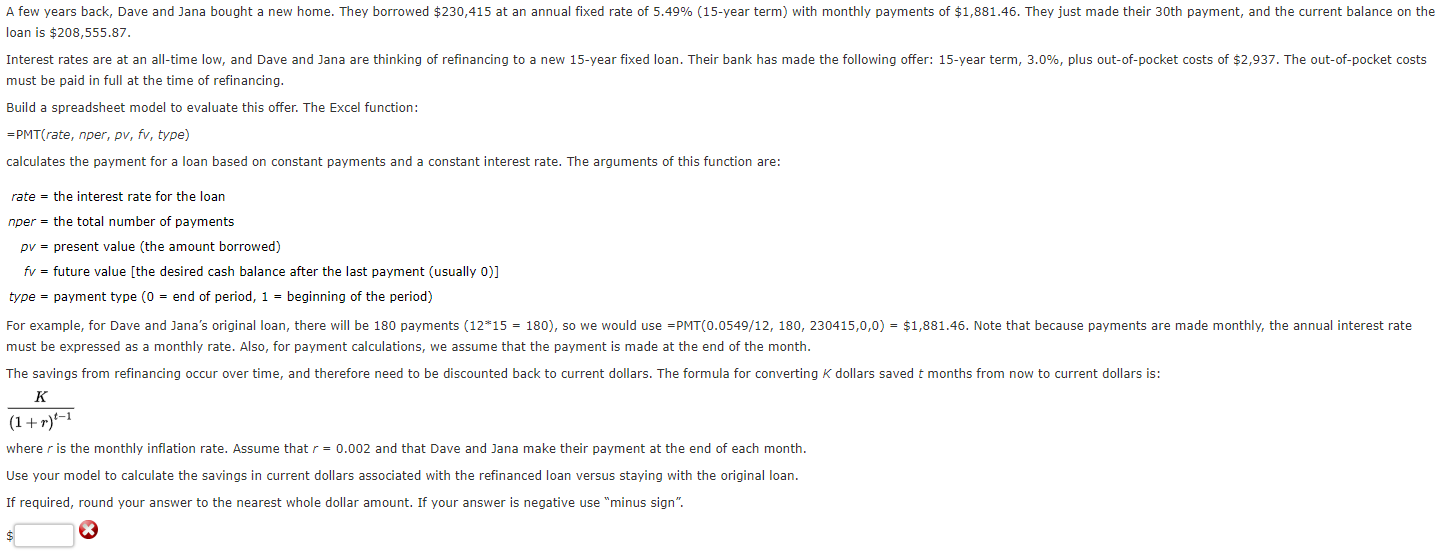

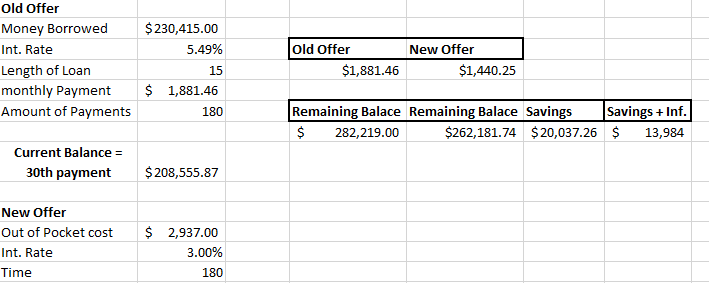

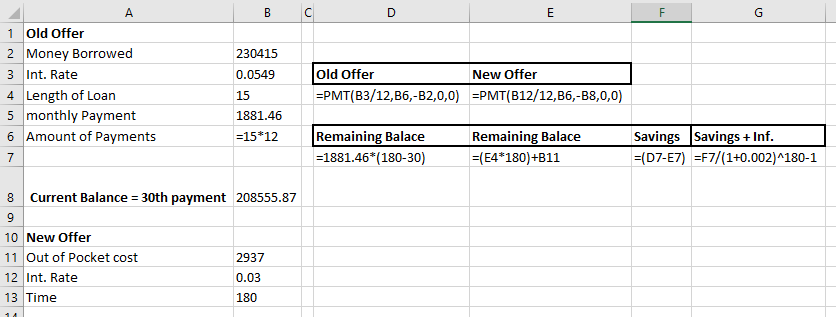

A few years back, Dave and Jana bought a new home. They borrowed $230,415 at an annual fixed rate of 5.49% (15-year term) with monthly payments of $1,881.46. They just made their 30th payment, and the current balance on the loan is $208,555.87. Interest rates are at an all-time low, and Dave and Jana are thinking of refinancing to a new 15-year fixed loan. Their bank has made the following offer: 15-year term, 3.0%, plus out-of-pocket costs of $2,937. The out-of-pocket costs must be paid in full at the time of refinancing. Build a spreadsheet model to evaluate this offer. The Excel function: =PMT(rate, nper, pv, fv, type) calculates the payment for a loan based on constant payments and a constant interest rate. The arguments of this function are: rate = the interest rate for the loan nper = the total number of payments pv = present value (the amount borrowed) fv = future value [the desired cash balance after the last payment (usually 0)] type = payment type (0 = end of period, 1 = beginning of the period) For example, for Dave and Jana's original loan, there will be 180 payments (12*15 = 180), so we would use =PMT(0.0549/12, 180, 230415,0,0) = $1,881.46. Note that because payments are made monthly, the annual interest rate must be expressed as a monthly rate. Also, for payment calculations, we assume that the payment is made at the end of the month. The savings from refinancing occur over time, and therefore need to be discounted back to current dollars. The formula for converting K dollars saved t months from now to current dollars is: K (1+r)-1 where r is the monthly inflation rate. Assume that r = 0.002 and that Dave and Jana make their payment at the end of each month. Use your model to calculate the savings in current dollars associated with the refinanced loan versus staying with the original loan. If required, round your answer to the nearest whole dollar amount. If your answer is negative use "minus sign". Old Offer Money Borrowed Int. Rate Length of Loan monthly Payment Amount of Payments $ 230,415.00 5.49% 15 $ 1,881.46 180 Old Offer $1,881.46 New Offer $1,440.25 Remaining Balace Remaining Balace Savings Savings + Inf. $ 282,219.00 $262,181.74 $20,037.26 $ 13,984 Current Balance = 30th payment $ 208,555.87 New Offer Out of Pocket cost Int. Rate Time $ 2,937.00 3.00% 180 B B C D E F G 230415 0.0549 1 Old Offer 2 Money Borrowed 3 Int. Rate 4 Length of Loan 5 monthly Payment 6 Amount of Payments 7 Old Offer New Offer =PMT(B3/12, B6,-B2,0,0) =PMT(B12/12,B6,-38,0,0) 15 1881.46 =15*12 Remaining Balace =1881.46*(180-30) Remaining Balace =(E4*180)+B11 Savings Savings + Inf. =(D7-E7) =F7/(1+0.002)-180-1 8 Current Balance = 30th payment 208555.87 9 10 New Offer 11 Out of Pocket cost 2937 12 Int. Rate 0.03 13 Time 180

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Structural Foundations Of Monetary Policy

Authors: Michael D. Bordo, John H. Cochrane, Amit Seru

1st Edition

0817921346, 978-0817921347