Answered step by step

Verified Expert Solution

Question

1 Approved Answer

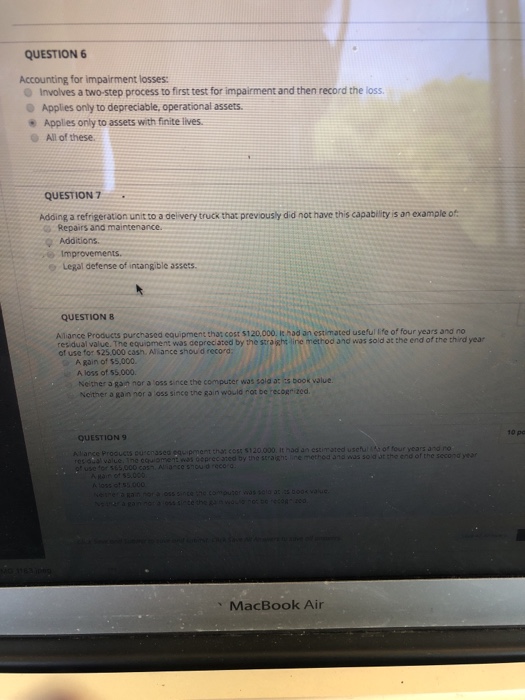

QUESTION6 Accounting for impairment losses: Involves a two-step process to first test for impairment and then record the loss. Applies only to depreciable, operational assets

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Using Equity Audits In The Classroom To Reach And Teach All Students

Authors: Kathryn B. McKenzie, Linda E. Skrla

1st Edition

141298677X, 978-1412986779