Answered step by step

Verified Expert Solution

Question

1 Approved Answer

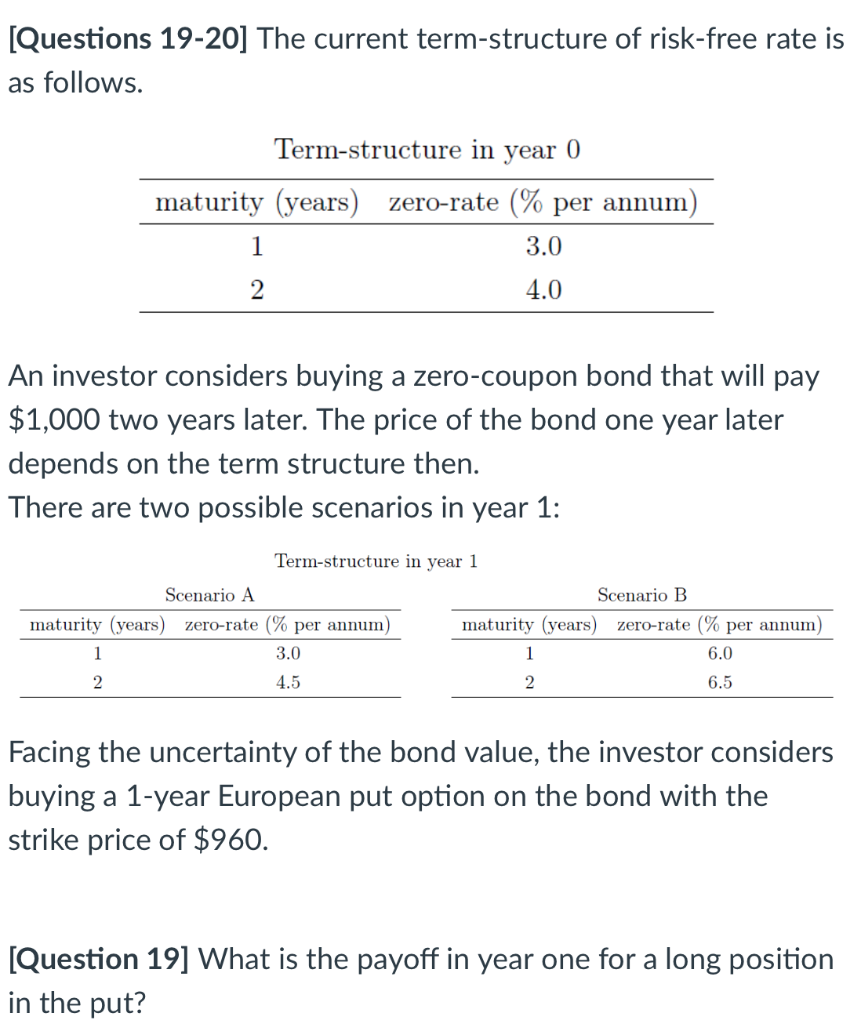

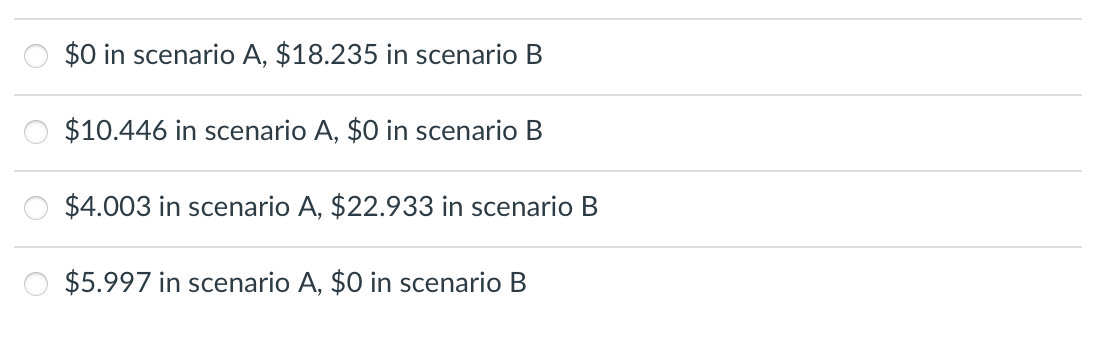

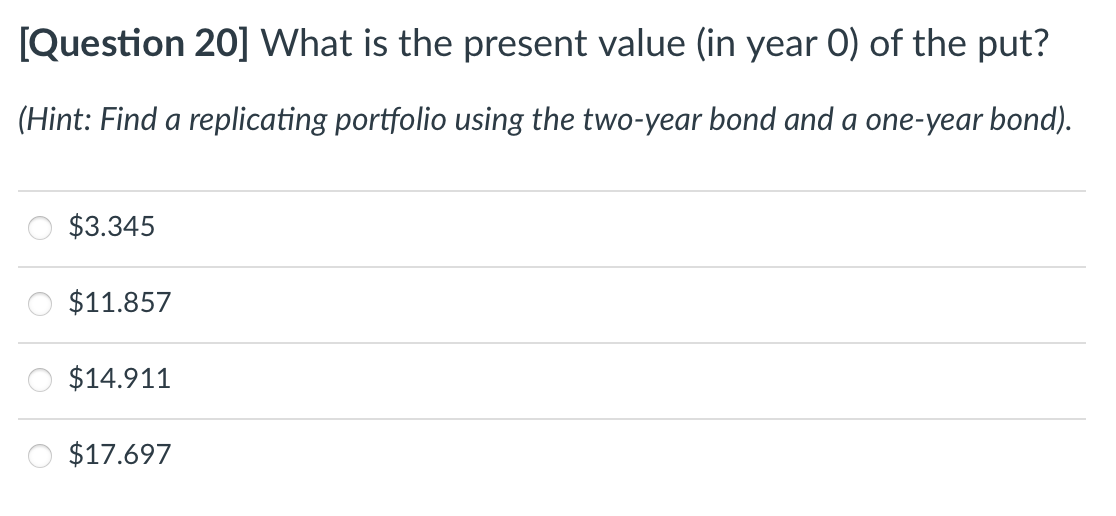

[Questions 19-20] The current term-structure of risk-free rate is as follows. Term-structure in year 0 maturity (years) zero-rate (% per annum) 1 3.0 2 4.0

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Ziglar On Selling The Ultimate Handbook For The Complete Sales Professional

Authors: Zig Ziglar

1st Edition

0785288937, 978-0785288930