Questions to Answer:

- Did Abby compute the cost of the Breeland Ltd. special order correctly before the weekend get-together? If not, how was her cost estimate and/or price determination flawed?

- Whose assessment of the costing of this special order do you believe is correctGeorge Smilees or Abby Conroys? That is, should Georges conversations with Josh impact Abbys cost estimate of the Breeland Ltd. special order? Explain your answer.

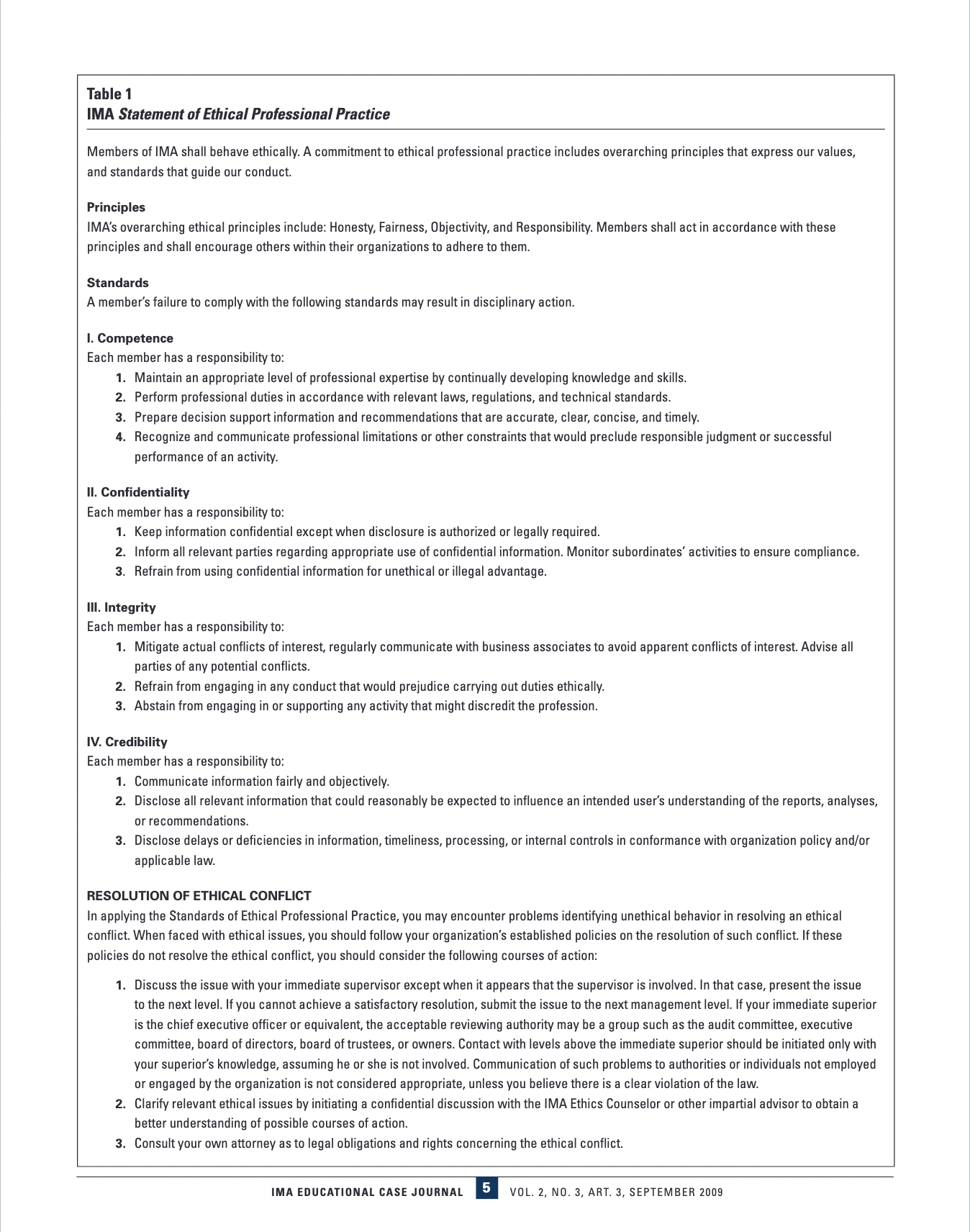

- Are there any ethical issues related to the cost determination on the Breeland Ltd. special order? If so, what issues are present? How should Abby resolve these conflicts? Should Abby go directly to Tom Brennen about this new development? How can Abby use the IMA Statement of Ethical Professional Practice as a guide for her actions?

- If Abby were to modify her original cost estimate of the Breeland Ltd. special order to include Joshs purchase of the remaining 10 gallons of XO-1600, what price determination would she have arrived at? What impact would that have had on Ace Fertilizers bottom line?

Alternatively, Abby would like to submit a revised quote to Breeland Ltd. if Josh's order is finalized within 20 days. Specifically, she would like to only bill Breeland Ltd. for 40 gallons of XO-1600, delete the disposal costs, and modify the organization-sustaining and profit on cost amounts. Josh would then be shipped the product and be billed for the cost of the 10 gallons of XO-1600. Contrary to George's suggestion, Abby believes that Josh should also be billed an appropriate organization-sustaining cost amount in addition to a profit on cost. Even these amounts, however, would result in a smaller profit margin for the special order and would not allow the company to meet its monthly profit goal. George Smilee seems adamant in his determination and has instructed Abby to develop a quote for Josh independent of the cost determination for the Breeland special order. George is meeting with Tom Brennen the first thing on Wednesday morning to get his approval and signature on the special order. Abby is contemplating what course of action she should take. She plans to rely, in part, on the guidance provided by the Institute of Management Accounting (IMA) in its Statement of Ethical Professional Practice, found in Table 1. Abby is wondering why George Smilee is not using this same guidance. She wonders if George would be taking a similar position if he also were a Certified Management Accountant (CMA). Toward the end of the day on Friday, Abby works up the following cost estimate and price determination for this special order: Abby discusses this estimate and price quote with George Smilee, who expresses preliminary approval. Abby fully believes that Breeland Ltd. will accept this price quote. All that is needed now is Tom Brennen's formal approval and signature. Before Abby and George leave for the weekend, they both concur that it is highly probable that Breeland's special order will be approved next week. Details as to production and completion dates will be finalized upon approval of the special order. The Weekend Family Get-Together. The Smilee clan has a gettogether planned for Saturday afternoon, and George informs Abby that he is really looking forward to it. Unfortunately, Abby has prior plans and cannot attend. This is a very special occasion for George's family, as Grandma Smilee has just turned 80 years old. The weather is just perfect for the gathering. George mingles with his family and is truly enjoying himself. After the meal and games, George spends some quiet time with his brothers. He is sharing some of the details of the special order for the solvent. When one of his brothers, Josh, hears George mention the chemical XO-1600, he becomes very interested. It turns out that he has recently been approached by a customer to manufacture a spray-on rust inhibitor that requires XO-1600 as an ingredient. The quantity needed for that order is 8 gallons, but Josh thinks he can convince the customer to expand his order to use all of the 10 gallons. Josh briefly walks away from the group, calls his customer, and confirms the order. Smiling, Josh informs George of the news. The two agree to finalize this arrangement later in the coming week. Josh's Project Price Determination. Early Monday morning, George goes to Abby's office to inform her of the development with Josh over the weekend. He explains Josh's intent to purchase the remaining 10 gallons of XO-1600. George indicates that the details of that agreement are to be finalized later in the week. Pausing for a moment to fully understand the details of this arrangement, Abby remembers and informs George that the price quote last Friday assumed that the extra 10 gallons would remain unused and would require disposal, and accordingly the order included the entire cost of the XO1600 plus the mandated disposal costs. Abby suggests that Breeland Ltd. be informed of a slight delay in the price quote and if Breeland agrees to the delay, then the initial order can be revised in light of Josh's forthcoming order. To Abby's surprise, George is very cold to the idea of delaying the initial order. George contends that as of today, there are no confirmed orders that would require the extra 10 gallons of XO-1600. In fact, there will be no confirmed orders until later this week, when Josh meets with George to finalize the weekend arrangement. Consequently, George maintains that the special order as presently priced should be forwarded to Tom Brennen for his approval and signature, and if and when a formal order is received from Josh, that order should simply include a prorated cost for the 10 gallons of XO-1600 plus a profit markup on cost. George, in fact, is elated and sees this as a windfall, as the 10 gallons of XO1600 can be billed twice and the billed disposal costs would not be incurred. This pleasant turn of events adds $93,600 ( $16,000 for the 10 gallons of XO-1600, $10,000 of eliminated disposal costs, $26,000 for organization-sustaining level activity costs, and $41,600 for markup on the cost of the 10 gallons of XO-1600) to the company's bottom line. Abby fully realizes that she had already developed the price quote for Breeland's order the week before, and George Smilee had expressed his approval. Since there were no confirmed orders existing at that time for the unused portion of the XO-1600, Abby, according to company policy, included the entire acquisition cost plus disposal costs in the cost estimate. Abby now knows that an order in all likelihood will be obtained within the 20-day disposal period for the remaining 10 gallons of XO-1600. Given this new information, Abby believes that her original cost estimate should be amended pending approval of a delay by Breeland Ltd. Ace Fertilizer Company: Ethical Cost Allocations and Price Determination Jerry Kreuze Western Michigan University INTRODUCTION Having a double undergraduate major in Accounting and Integrated Supply Management and an MBA from a renowned business school qualified Abby Conroy, CMA, for her position at Ace Fertilizer Company. She has been employed at Ace Fertilizer for the past three years, and is a highly respected employee. Her hard work and dedication to detail resulted in a series of rapid promotions. Currently, Abby is assistant director of manufacturing and is primarily responsible for special customer orders. Meeting the needs of customers in manufacturing special orders has become a very profitable portion of Ace's operations. These special orders sometimes complement, but more frequently are totally unrelated to, Ace's principal business of producing lawn and garden fertilizer. Ace Fertilizer actively seeks special orders in a highly competitive market, driven more by quality and on-time completion than price. Ace has established itself as an industry leader by consistently meeting customer expectations. The ability to meet the needs of customers through manufacturing special orders was the concept of Ace's founders, and now passive owners, James Stegink and Norman Light. Both have engineering degrees and are considered by many to be quite the "tinkerers." Abby reports to the director of manufacturing, George Smilee. The manufacturing operations are managed by Tom Brennen, the chief operating officer of Ace Fertilizer. In her role as assistant director, Abby is responsible for the design, bidding, manufacture, and ultimate delivery of special orders to customers. Abby develops and completes all special order contracts. George Smilee initials his approval of these contracts. Completed, initialed customer contracts then proceed to Tom Brennen for his ultimate approval and signature. All special orders at Ace Fertilizer follow a prescribed billing formula. These special orders, unless specific authorization is obtained from Tom Brennen himself, must be billed at 80 percent over the cost of the order. Tom Brennen rarely allows exceptions to this formula, as sufficient demand exists for Ace Fertilizer's operating capacity. Although Ace maintains an extensive raw materials inventory, on occasion these special orders require Abby to order materials specific to the order. These materials are acquired in the most economical order quantity available. The special order is billed for the entire cost of the specially ordered materials, even if unused quantities remain. Customers are given the option of keeping these unused materials, but virtually all companies decline. An exception to that policy is only allowed when another confirmed order exists when the initial order is signed that requires the use of those excess materials. In that case, Tom Brennen, as a matter of fairness, insists that the cost of those materials be prorated among special orders. What Abby likes especially about Ace Fertilizer is its family atmosphere. In fact, Abby has been invited several times by George Smilee to his family get-togethers. George is close to his family, most of whom live within a 10 -mile radius. The family has regular get-togethers attended faithfully by George and his two brothers. George's family has become very close since the untimely death of George's father last year. His brothers are all self-employed in a variety of businesses, and on occasion Ace Fertilizer does special orders for them. Abby has become very skilled at computing the cost of special orders. She fully realizes a special order includes a variety of costs, including direct and indirect costs. Abby knows that proper project cost determination mandates inclusion of all of these costs. DIRECT COSTS VS. INDIRECT COSTS Direct costs are those costs that are easily and conveniently assigned to a special order. Major direct costs for Abby are direct materials and direct labor. Direct materials are those materials that become an integral part of the finished product. Direct labor, sometimes referred to as "touch labor," includes the cost of those laborers who directly touch the product while it is being made. The wages of general production employees who are idled due to machine breakdown are classified as indirect costs. Direct costs are usually variable and change as production volumes change. Thus, direct materials and direct labor are typically variable costs. For special orders, some direct costs can be fixed, however. The costs (depreciation, electricity, and routine maintenance) associated with a machine dedicated to one product are direct costs of that product. Indirect costs cannot be easily and conveniently assigned to a special order. Rather, these costs are common costs, in that they are incurred to produce a variety of special orders. Maintenance costs of general purpose equipment, the supervisor's salary, and utilities are direct costs needed to produce special orders in general, but are indirect costs for a particular special order. Moreover, general production costs, including property taxes, insurance, lawn care, cafeteria costs, and miscellaneous supplies consumed in production are indirect costs properly allocated to special orders manufactured. ALLOCATION OF INDIRECT COSTS Abby could allocate indirect costs to special orders using a company-wide overhead rate. Frequently, these indirect costs are allocated by selecting an allocation base common to all of the company's products or services. Many companies base overhead allocations on direct labor-hours or machine-hours. Abby realizes, however, that this allocation process is troublesome as it is impractical to trace these costs to specific orders. Alternatively, Abby could allocate indirect costs to special orders using activity-based costing (ABC). Rather than simply allocating indirect costs among special orders using a company-wide rate, ABC acknowledges that not all costs are driven by output volume. As a result, information is available to help determine the most profitable special orders and customers, which activities and processes are value-added, and where efforts toward improvements can be made. Abby especially likes this latter approach when assigning indirect costs to special orders. BREELAND LTD. SPECIAL ORDER The Cost Estimate. Abby has received a request from Breeland Ltd. to produce a unique, somewhat unstable cleaning solvent for use in Breeland's specialized steel plating process. Ace Fertilizer is one of only a handful of companies across the country capable of producing such a solvent. The customer has a limited need for this solvent, and does not foresee requiring quantities of it beyond this special order. To produce this substance, Abby must purchase a specialty acid ingredient known as XO-1600. That substance is only available in 50 -gallon drums. The 50 -gallon drum costs $80,000. This special order will only require the use of 40 gallons. XO-1600 has a shelf life of only 20 days after the drum is opened. After those 20 days, the substance becomes very unstable and must be discarded. Because of the chemical nature of the substance, it requires proper disposal. Abby estimates the cost of this disposal at $10,000. Abby has checked existing, confirmed orders and found none that will require XO-1600 within the next 20 days. Inquiries with representatives at Breeland Ltd. reveal that they have no interest in taking possession of the unused gallons. Abby also determines that several other costs and activities will be associated with the completion of the special order for the solvent. These costs and activities are: 1. Direct materials, in addition to XO1600:$20,000. 2. Direct labor: $30,000. 3. Unit measure of special order: 4,000 gallons. 4. Number of batches for production: 4 (due to constraints during the mixing process). Using ABC at the beginning of the costing period, Abby arrives at the following costs for each of the five activity measures: a. Unit-level activities: $40 per unit of measure. b. Batch-level activities: $5,000 per batch. c. Product-level activities: $80,000 per project. d. Customer-related activities: $30,000 per customer. e. Organization-sustaining activities: 100% of direct materials, direct labor, unit-level activity costs, and batch-level activity costs. Table 1 IMA Statement of Ethical Professional Practice Members of IMA shall behave ethically. A commitment to ethical professional practice includes overarching principles that express our values, and standards that guide our conduct. Principles IMA's overarching ethical principles include: Honesty, Fairness, Objectivity, and Responsibility. Members shall act in accordance with these principles and shall encourage others within their organizations to adhere to them. Standards A member's failure to comply with the following standards may result in disciplinary action. I. Competence Each member has a responsibility to: 1. Maintain an appropriate level of professional expertise by continually developing knowledge and skills. 2. Perform professional duties in accordance with relevant laws, regulations, and technical standards. 3. Prepare decision support information and recommendations that are accurate, clear, concise, and timely. 4. Recognize and communicate professional limitations or other constraints that would preclude responsible judgment or successful performance of an activity. II. Confidentiality Each member has a responsibility to: 1. Keep information confidential except when disclosure is authorized or legally required. 2. Inform all relevant parties regarding appropriate use of confidential information. Monitor subordinates' activities to ensure compliance. 3. Refrain from using confidential information for unethical or illegal advantage. III. Integrity Each member has a responsibility to: 1. Mitigate actual conflicts of interest, regularly communicate with business associates to avoid apparent conflicts of interest. Advise all parties of any potential conflicts. 2. Refrain from engaging in any conduct that would prejudice carrying out duties ethically. 3. Abstain from engaging in or supporting any activity that might discredit the profession. IV. Credibility Each member has a responsibility to: 1. Communicate information fairly and objectively. 2. Disclose all relevant information that could reasonably be expected to influence an intended user's understanding of the reports, analyses, or recommendations. 3. Disclose delays or deficiencies in information, timeliness, processing, or internal controls in conformance with organization policy and/or applicable law. RESOLUTION OF ETHICAL CONFLICT In applying the Standards of Ethical Professional Practice, you may encounter problems identifying unethical behavior in resolving an ethical conflict. When faced with ethical issues, you should follow your organization's established policies on the resolution of such conflict. If these policies do not resolve the ethical conflict, you should consider the following courses of action: 1. Discuss the issue with your immediate supervisor except when it appears that the supervisor is involved. In that case, present the issue to the next level. If you cannot achieve a satisfactory resolution, submit the issue to the next management level. If your immediate superior is the chief executive officer or equivalent, the acceptable reviewing authority may be a group such as the audit committee, executive committee, board of directors, board of trustees, or owners. Contact with levels above the immediate superior should be initiated only with your superior's knowledge, assuming he or she is not involved. Communication of such problems to authorities or individuals not employed or engaged by the organization is not considered appropriate, unless you believe there is a clear violation of the law. 2. Clarify relevant ethical issues by initiating a confidential discussion with the IMA Ethics Counselor or other impartial advisor to obtain a better understanding of possible courses of action. 3. Consult your own attorney as to legal obligations and rights concerning the ethical conflict