Answered step by step

Verified Expert Solution

Question

1 Approved Answer

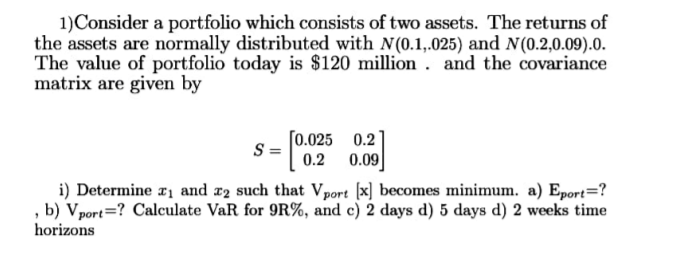

R = 1 & N(0.1, 0.025) 1)Consider a portfolio which consists of two assets. The returns of the assets are normally distributed with N(0.1,.025) and

R = 1 & N(0.1, 0.025)

1)Consider a portfolio which consists of two assets. The returns of the assets are normally distributed with N(0.1,.025) and N(0.2,0.09).0. The value of portfolio today is $120 million and the covariance matrix are given by [0.025 0.2 S= 0.2 0.09 i) Determine 11 and 12 such that Vport [x] becomes minimum. a) Eport=? ; b) V port=? Calculate VaR for 9R%, and c) 2 days d) 5 days d) 2 weeks time horizons 1)Consider a portfolio which consists of two assets. The returns of the assets are normally distributed with N(0.1,.025) and N(0.2,0.09).0. The value of portfolio today is $120 million and the covariance matrix are given by [0.025 0.2 S= 0.2 0.09 i) Determine 11 and 12 such that Vport [x] becomes minimum. a) Eport=? ; b) V port=? Calculate VaR for 9R%, and c) 2 days d) 5 days d) 2 weeks time horizonsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started