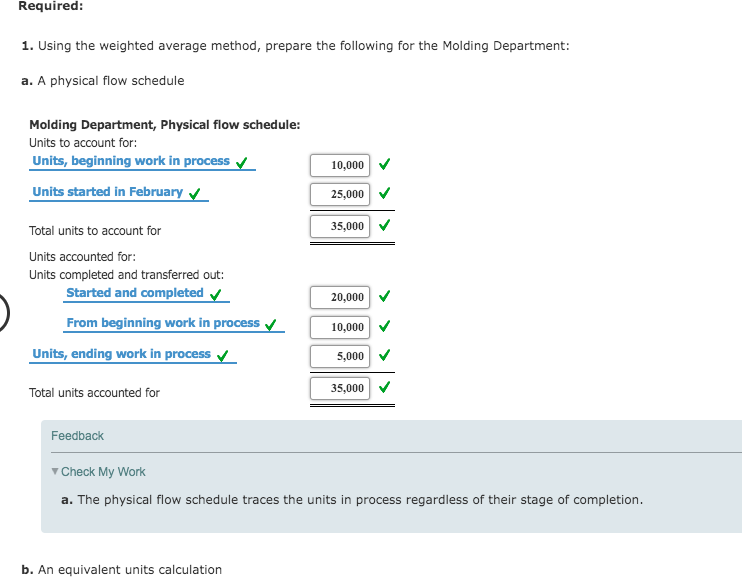

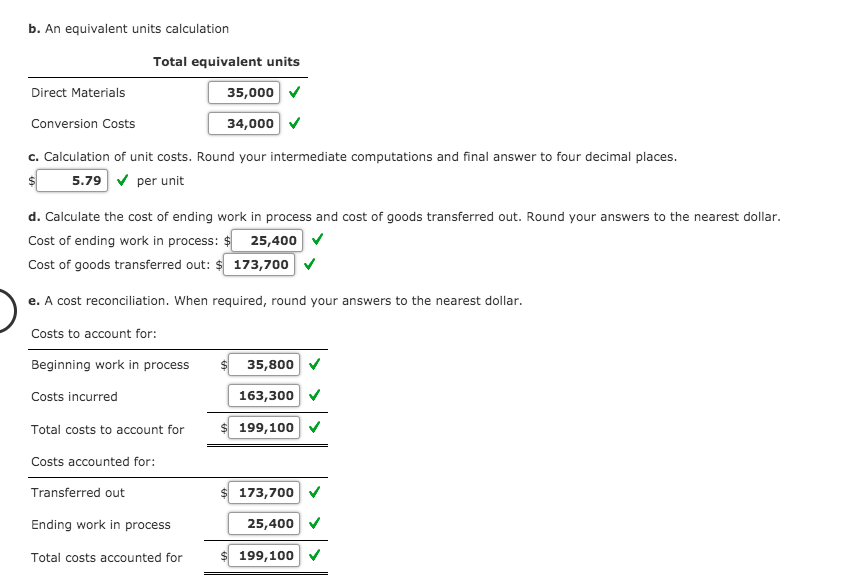

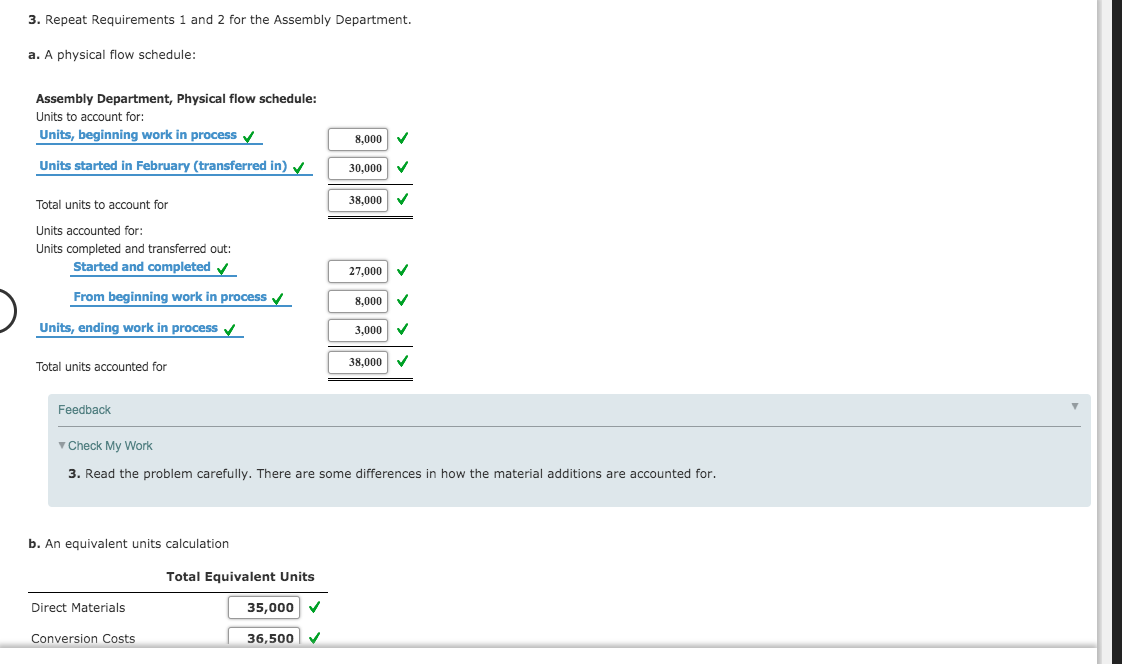

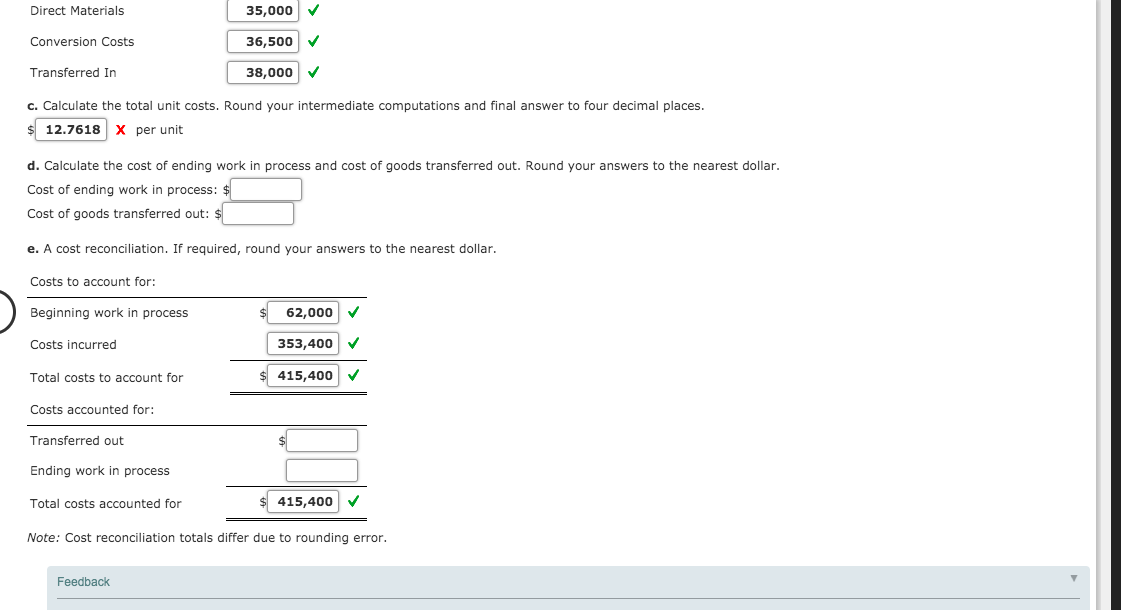

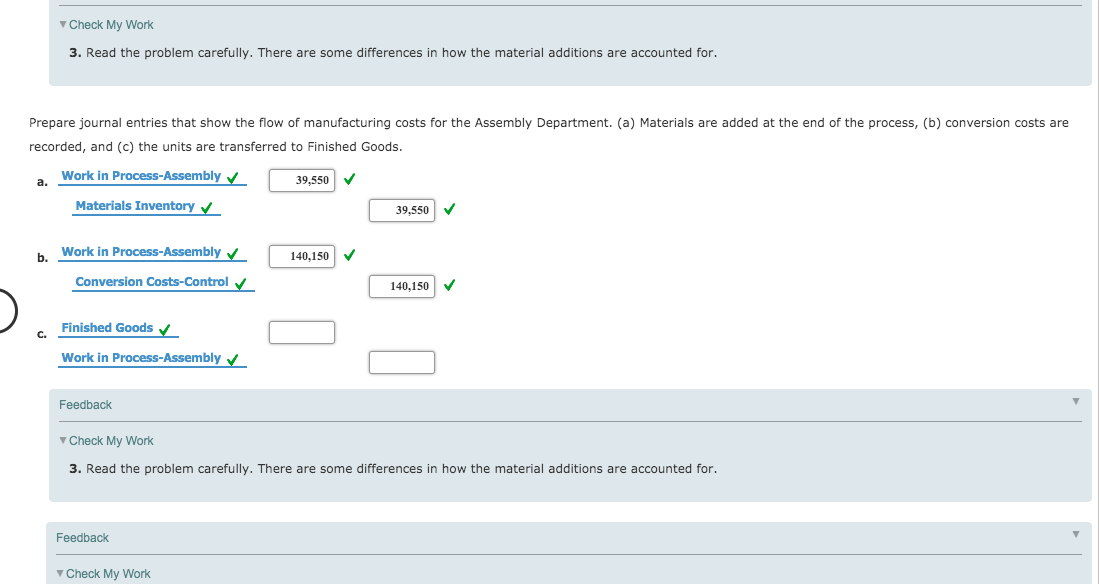

Required: 1. Using the weighted average method, prepare the following for the Molding Department: a. A physical flow schedule Molding Department, Physical flow schedule: Units to account for: Units, beginning work in process 10,000 Units started in February 25,000 35,000 Total units to account for Units accounted for: Units completed and transferred out: Started and completed 20,000 From beginning work in process 10,000 Units, ending work in process 5,000 Total units accounted for 35,000 Feedback Check My Work a. The physical flow schedule traces the units in process regardless of their stage of completion. b. An equivalent units calculation b. An equivalent units calculation Total equivalent units Direct Materials 35,000 20 Conversion Costs 34,000 c. Calculation of unit costs. Round your intermediate computations and final answer to four decimal places. $ 5.79 per unit d. Calculate the cost of ending work in process and cost of goods transferred out. Round your answers to the nearest dollar. Cost of ending work in process: $ 25,400 V Cost of goods transferred out: $ 173,700 e. A cost reconciliation. When required, round your answers to the nearest dollar. Costs to account for: Beginning work in process $ 35,800 163,300 Costs incurred Total costs to account for $199,100 Costs accounted for: Transferred out $ 173,700 25,400 Ending work in process Total costs accounted for $199,100 2. Prepare journal entries that show the flow of manufacturing costs for the Molding Department. (a) Materials are added at the beginning of the process, (b) conversion costs are recorded, and (c) units are transferred to the Assembly Department. When required, round your answers to the nearest dollar. Work in Process-Molding 56,400 V Materials Inventory 56,400 Work in Process-Molding b. 106,900 Conversion Costs-Control 106,900 Work in Process-Assembly 173,700 Work in Process-Molding 173,700 Feedback Check My Work 2. An example of journal entries showing the flow of costs is illustrated above Exhibit 6.5. 3. Repeat Requirements 1 and 2 for the Assembly Department. a. A physical flow schedule: Assembly Department, Physical flow schedule: Units to account for: Units, beginning work in process 8,000 Units started in February (transferred in) 30,000 38,000 Total units to account for Units accounted for: Units completed and transferred out: Started and completed 27,000 From beginning work in process 8,000 Units, ending work in process 3,000 Total units accounted for 38,000 Feedback Check My Work 3. Read the problem carefully. There are some differences in how the material additions are accounted for. b. An equivalent units calculation Total Equivalent Units Direct Materials 35,000 Conversion Costs 36,500 Direct Materials Conversion Costs 35,000 36,500 38,000 Transferred In c. Calculate the total unit costs. Round your intermediate computations and final answer to four decimal places. $12.7618 x per unit d. Calculate the cost of ending work in process and cost of goods transferred out. Round your answers to the nearest dollar. Cost of ending work in process: $ Cost of goods transferred out: $ e. A cost reconciliation. If required, round your answers to the nearest dollar. Costs to account for: Beginning work in process Costs incurred $ 62,000 353,400 $ 415,400 Total costs to account for Costs accounted for: Transferred out Ending work in process Total costs accounted for $415,400 V Note: Cost reconciliation totals differ due to rounding error. Feedback Check My Work 3. Read the problem carefully. There are some differences in how the material additions are accounted for. Prepare journal entries that show the flow of manufacturing costs for the Assembly Department. (a) Materials are added at the end of the process, (b) conversion costs are recorded, and (c) the units are transferred to Finished Goods. Work in Process-Assembly 39,550 Materials Inventory 39,550 h Work in Process-Assembly 140,150 Conversion Costs-Control 140,150 Finished Goods Work in Process-Assembly Feedback Check My Work 3. Read the problem carefully. There are some differences in how the material additions are accounted for. Feedback Check My Work Required: 1. Using the weighted average method, prepare the following for the Molding Department: a. A physical flow schedule Molding Department, Physical flow schedule: Units to account for: Units, beginning work in process 10,000 Units started in February 25,000 35,000 Total units to account for Units accounted for: Units completed and transferred out: Started and completed 20,000 From beginning work in process 10,000 Units, ending work in process 5,000 Total units accounted for 35,000 Feedback Check My Work a. The physical flow schedule traces the units in process regardless of their stage of completion. b. An equivalent units calculation b. An equivalent units calculation Total equivalent units Direct Materials 35,000 20 Conversion Costs 34,000 c. Calculation of unit costs. Round your intermediate computations and final answer to four decimal places. $ 5.79 per unit d. Calculate the cost of ending work in process and cost of goods transferred out. Round your answers to the nearest dollar. Cost of ending work in process: $ 25,400 V Cost of goods transferred out: $ 173,700 e. A cost reconciliation. When required, round your answers to the nearest dollar. Costs to account for: Beginning work in process $ 35,800 163,300 Costs incurred Total costs to account for $199,100 Costs accounted for: Transferred out $ 173,700 25,400 Ending work in process Total costs accounted for $199,100 2. Prepare journal entries that show the flow of manufacturing costs for the Molding Department. (a) Materials are added at the beginning of the process, (b) conversion costs are recorded, and (c) units are transferred to the Assembly Department. When required, round your answers to the nearest dollar. Work in Process-Molding 56,400 V Materials Inventory 56,400 Work in Process-Molding b. 106,900 Conversion Costs-Control 106,900 Work in Process-Assembly 173,700 Work in Process-Molding 173,700 Feedback Check My Work 2. An example of journal entries showing the flow of costs is illustrated above Exhibit 6.5. 3. Repeat Requirements 1 and 2 for the Assembly Department. a. A physical flow schedule: Assembly Department, Physical flow schedule: Units to account for: Units, beginning work in process 8,000 Units started in February (transferred in) 30,000 38,000 Total units to account for Units accounted for: Units completed and transferred out: Started and completed 27,000 From beginning work in process 8,000 Units, ending work in process 3,000 Total units accounted for 38,000 Feedback Check My Work 3. Read the problem carefully. There are some differences in how the material additions are accounted for. b. An equivalent units calculation Total Equivalent Units Direct Materials 35,000 Conversion Costs 36,500 Direct Materials Conversion Costs 35,000 36,500 38,000 Transferred In c. Calculate the total unit costs. Round your intermediate computations and final answer to four decimal places. $12.7618 x per unit d. Calculate the cost of ending work in process and cost of goods transferred out. Round your answers to the nearest dollar. Cost of ending work in process: $ Cost of goods transferred out: $ e. A cost reconciliation. If required, round your answers to the nearest dollar. Costs to account for: Beginning work in process Costs incurred $ 62,000 353,400 $ 415,400 Total costs to account for Costs accounted for: Transferred out Ending work in process Total costs accounted for $415,400 V Note: Cost reconciliation totals differ due to rounding error. Feedback Check My Work 3. Read the problem carefully. There are some differences in how the material additions are accounted for. Prepare journal entries that show the flow of manufacturing costs for the Assembly Department. (a) Materials are added at the end of the process, (b) conversion costs are recorded, and (c) the units are transferred to Finished Goods. Work in Process-Assembly 39,550 Materials Inventory 39,550 h Work in Process-Assembly 140,150 Conversion Costs-Control 140,150 Finished Goods Work in Process-Assembly Feedback Check My Work 3. Read the problem carefully. There are some differences in how the material additions are accounted for. Feedback Check My Work