Answered step by step

Verified Expert Solution

Question

1 Approved Answer

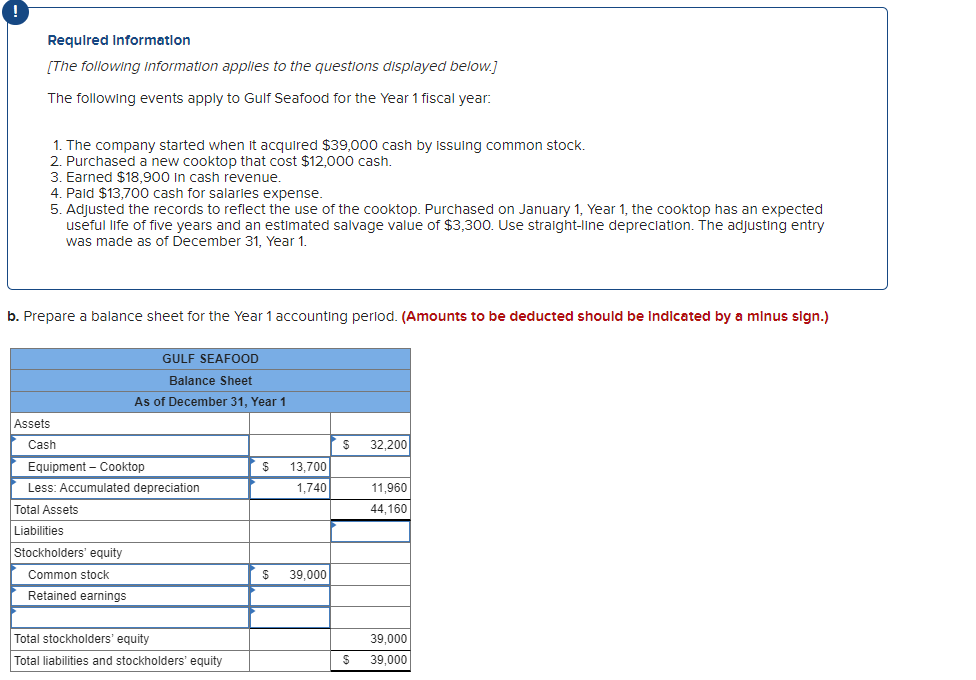

Required Information [The following information applles to the questions displayed below.] The following events apply to Gulf Seafood for the Year 1 fiscal year: 1.

Required Information [The following information applles to the questions displayed below.] The following events apply to Gulf Seafood for the Year 1 fiscal year: 1. The company started when it acquired $39,000 cash by issuing common stock. 2. Purchased a new cooktop that cost $12,000 cash. 3. Earned $18,900 in cash revenue. 4. Pald $13,700 cash for salarles expense. 5. Adjusted the records to reflect the use of the cooktop. Purchased on January 1, Year 1, the cooktop has an expected useful IIfe of five years and an estimated salvage value of $3,300. Use straight-IIne depreciation. The adjusting entry was made as of December 31, Year 1. . Prepare a balance sheet for the Year 1 accounting perlod. (Amounts to be deducted should be Indicated by a minus sign.)

Required Information [The following information applles to the questions displayed below.] The following events apply to Gulf Seafood for the Year 1 fiscal year: 1. The company started when it acquired $39,000 cash by issuing common stock. 2. Purchased a new cooktop that cost $12,000 cash. 3. Earned $18,900 in cash revenue. 4. Pald $13,700 cash for salarles expense. 5. Adjusted the records to reflect the use of the cooktop. Purchased on January 1, Year 1, the cooktop has an expected useful IIfe of five years and an estimated salvage value of $3,300. Use straight-IIne depreciation. The adjusting entry was made as of December 31, Year 1. . Prepare a balance sheet for the Year 1 accounting perlod. (Amounts to be deducted should be Indicated by a minus sign.) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Guide To The National Initiative For Cybersecurity Education NICE Cybersecurity Workforce Framework 2.0 Internal Audit And IT Audit

Authors: Dan Shoemaker, Anne Kohnke, Ken Sigler

1st Edition

0367658623, 978-0367658625