Research in Federal Taxation

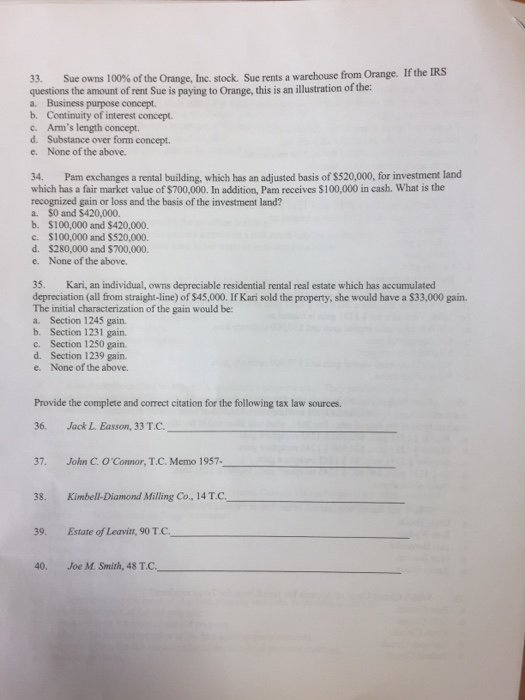

33. Sue owns 100% of the Orange, Inc. stock. Sue rents a warehouse from orange. If the IRS questions the amount of rent Sue is paying to Orange, this is an illustration of the: a. Business purpose concept. b. Continuity of interest concept. c. Arm's length concept. d. Substance over form concept. e. None of the above. 34. Pam exchanges a rental building. which has an adjusted basis of $520,000, for investment land which has a fair market value of$700,000. In addition, Pam receives S100,000 in cash. What is the recognized gain or loss and the basis of the investment land? a. S0 and $420,000. b. S100,000 and $420,000. c. $100,000 and $520,000. d. S280,000 and $700,000. e. None of the above, 35. Kari, an individual, owns depreciable residential rental real estate which has accumulated (all from straight-line) of$45,000. If Kari sold the property, she would have a $33,000 gain. The initial characterization of the gain would be: a. Section 1245 gain. b. Section 1231 gain. c, Section 1250 gain. d. Section 1239 gain. e. None of the above. Provide the complete and comect citation for the following tax law sources. 36, Jack L. Easson, 33 T.C. 37. John C. O'Connor, T.C. Memo 1957 38. Kimbell-Diamond Milling Co., 14 T.C. 39. Estate of Leavitt, 90 T. 40. Joe M. Smith, 48 T,C, 33. Sue owns 100% of the Orange, Inc. stock. Sue rents a warehouse from orange. If the IRS questions the amount of rent Sue is paying to Orange, this is an illustration of the: a. Business purpose concept. b. Continuity of interest concept. c. Arm's length concept. d. Substance over form concept. e. None of the above. 34. Pam exchanges a rental building. which has an adjusted basis of $520,000, for investment land which has a fair market value of$700,000. In addition, Pam receives S100,000 in cash. What is the recognized gain or loss and the basis of the investment land? a. S0 and $420,000. b. S100,000 and $420,000. c. $100,000 and $520,000. d. S280,000 and $700,000. e. None of the above, 35. Kari, an individual, owns depreciable residential rental real estate which has accumulated (all from straight-line) of$45,000. If Kari sold the property, she would have a $33,000 gain. The initial characterization of the gain would be: a. Section 1245 gain. b. Section 1231 gain. c, Section 1250 gain. d. Section 1239 gain. e. None of the above. Provide the complete and comect citation for the following tax law sources. 36, Jack L. Easson, 33 T.C. 37. John C. O'Connor, T.C. Memo 1957 38. Kimbell-Diamond Milling Co., 14 T.C. 39. Estate of Leavitt, 90 T. 40. Joe M. Smith, 48 T,C