Question

Review the Deloitte Case study posted in the Discussion forum, titled: handout-skeptical-lens-part 2. Review each of the 3 case studies and choose the one you

Review the Deloitte Case study posted in the Discussion forum, titled: handout-skeptical-lens-part 2. Review each of the 3 case studies and choose the one you prefer to use for this assignment. Using the brief overview of the issue and the corresponding result, respond to the following items:

1. What is professional skepticism?

2. As an accountant, whether audit, tax, private accounting, or non-profit accounting, when or how might you have to apply professional skepticism in your future career?

3. Referring to one of the three cases, how did the auditors apply professional skepticism to the engagement? Refer to some of the talking points from Eric Lewis, CPA from EY (our guest speaker on Thursday, April 20th) about what professional skepticism is and how it is used in practice.

4. Assume, you were the auditor on the engagement, and you did not speak up or use professional skepticism. How might the results differed, and which stakeholders may have been negatively impacted by the lack of skepticism?

It is okay to use the first person. APA formatting is not required. Consider using at least 1 professional or scholarly article to support your points in addition to the Deloitte case study. Your responses to the items above, should be between 250-400 words. Focus on professional vs academic writing, i.e., quality writing over quantity.

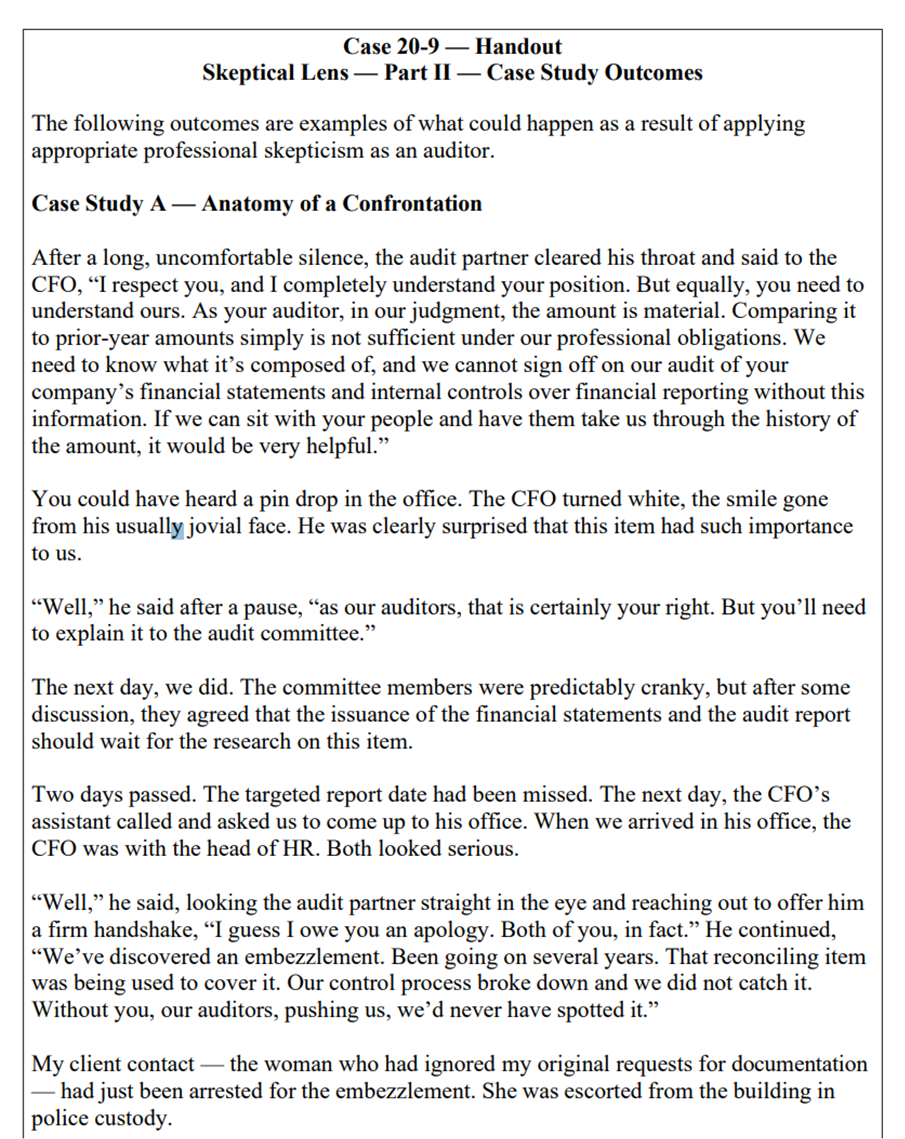

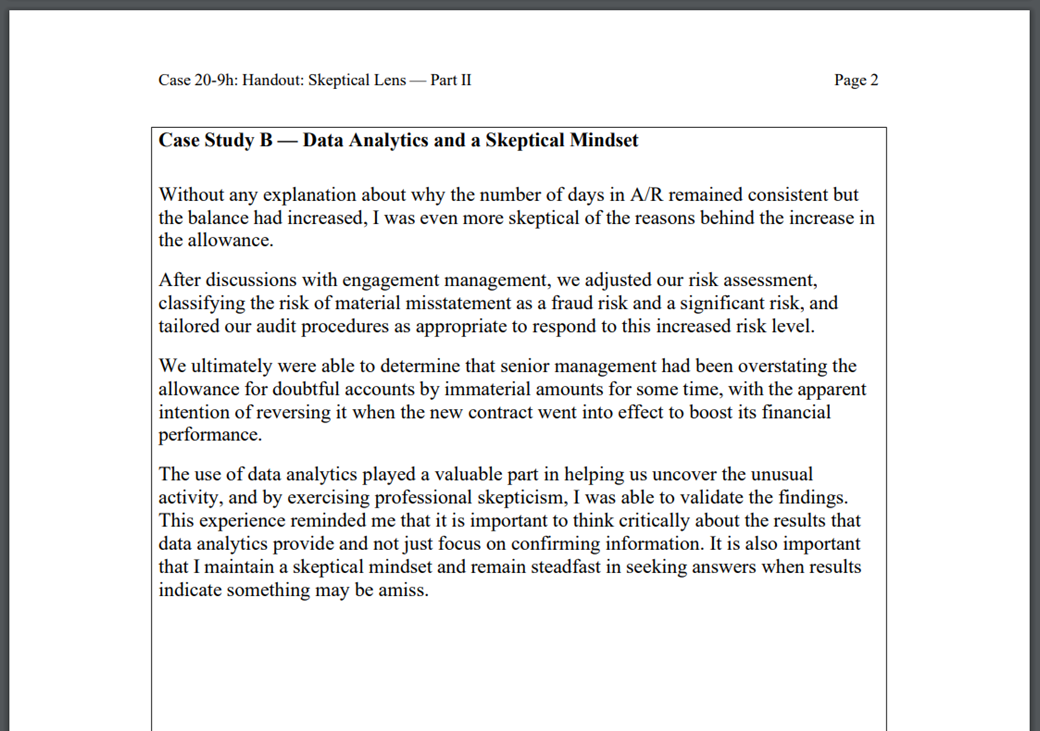

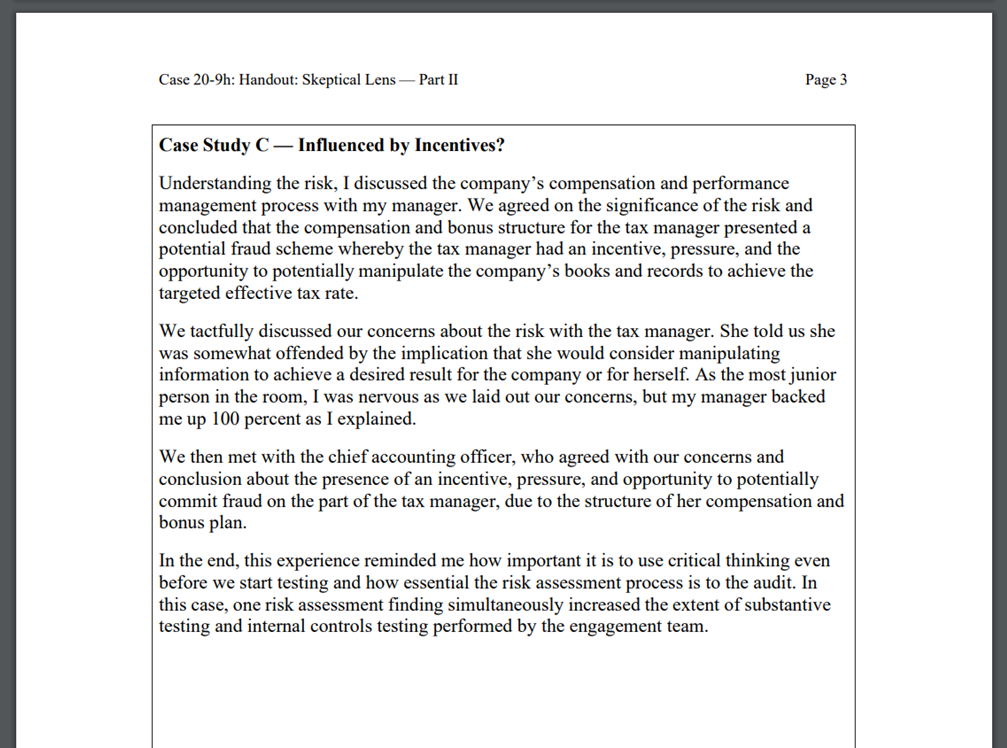

Case 20-9 Handout Skeptical Lens - Part II Case Study Outcomes The following outcomes are examples of what could happen as a result of applying appropriate professional skepticism as an auditor. Case Study A - Anatomy of a Confrontation After a long, uncomfortable silence, the audit partner cleared his throat and said to the CFO, "I respect you, and I completely understand your position. But equally, you need to understand ours. As your auditor, in our judgment, the amount is material. Comparing it to prior-year amounts simply is not sufficient under our professional obligations. We need to know what it's composed of, and we cannot sign off on our audit of your company's financial statements and internal controls over financial reporting without this information. If we can sit with your people and have them take us through the history of the amount, it would be very helpful." You could have heard a pin drop in the office. The CFO turned white, the smile gone from his usually jovial face. He was clearly surprised that this item had such importance to us. "Well," he said after a pause, "as our auditors, that is certainly your right. But you'll need to explain it to the audit committee." The next day, we did. The committee members were predictably cranky, but after some discussion, they agreed that the issuance of the financial statements and the audit report should wait for the research on this item. Two days passed. The targeted report date had been missed. The next day, the CFO's assistant called and asked us to come up to his office. When we arrived in his office, the CFO was with the head of HR. Both looked serious. "Well," he said, looking the audit partner straight in the eye and reaching out to offer him a firm handshake, "I guess I owe you an apology. Both of you, in fact." He continued, "We've discovered an embezzlement. Been going on several years. That reconciling item was being used to cover it. Our control process broke down and we did not catch it. Without you, our auditors, pushing us, we'd never have spotted it." My client contact - the woman who had ignored my original requests for documentation had just been arrested for the embezzlement. She was escorted from the building in police custody. Case Study B Data Analytics and a Skeptical Mindset Without any explanation about why the number of days in A/R remained consistent but the balance had increased, I was even more skeptical of the reasons behind the increase in the allowance. After discussions with engagement management, we adjusted our risk assessment, classifying the risk of material misstatement as a fraud risk and a significant risk, and tailored our audit procedures as appropriate to respond to this increased risk level. We ultimately were able to determine that senior management had been overstating the allowance for doubtful accounts by immaterial amounts for some time, with the apparent intention of reversing it when the new contract went into effect to boost its financial performance. The use of data analytics played a valuable part in helping us uncover the unusual activity, and by exercising professional skepticism, I was able to validate the findings. This experience reminded me that it is important to think critically about the results that data analytics provide and not just focus on confirming information. It is also important that I maintain a skeptical mindset and remain steadfast in seeking answers when results indicate something may be amiss. Case Study C - Influenced by Incentives? Understanding the risk, I discussed the company's compensation and performance management process with my manager. We agreed on the significance of the risk and concluded that the compensation and bonus structure for the tax manager presented a potential fraud scheme whereby the tax manager had an incentive, pressure, and the opportunity to potentially manipulate the company's books and records to achieve the targeted effective tax rate. We tactfully discussed our concerns about the risk with the tax manager. She told us she was somewhat offended by the implication that she would consider manipulating information to achieve a desired result for the company or for herself. As the most junior person in the room, I was nervous as we laid out our concerns, but my manager backed me up 100 percent as I explained. We then met with the chief accounting officer, who agreed with our concerns and conclusion about the presence of an incentive, pressure, and opportunity to potentially commit fraud on the part of the tax manager, due to the structure of her compensation and bonus plan. In the end, this experience reminded me how important it is to use critical thinking even before we start testing and how essential the risk assessment process is to the audit. In this case, one risk assessment finding simultaneously increased the extent of substantive testing and internal controls testing performed by the engagement team

Case 20-9 Handout Skeptical Lens - Part II Case Study Outcomes The following outcomes are examples of what could happen as a result of applying appropriate professional skepticism as an auditor. Case Study A - Anatomy of a Confrontation After a long, uncomfortable silence, the audit partner cleared his throat and said to the CFO, "I respect you, and I completely understand your position. But equally, you need to understand ours. As your auditor, in our judgment, the amount is material. Comparing it to prior-year amounts simply is not sufficient under our professional obligations. We need to know what it's composed of, and we cannot sign off on our audit of your company's financial statements and internal controls over financial reporting without this information. If we can sit with your people and have them take us through the history of the amount, it would be very helpful." You could have heard a pin drop in the office. The CFO turned white, the smile gone from his usually jovial face. He was clearly surprised that this item had such importance to us. "Well," he said after a pause, "as our auditors, that is certainly your right. But you'll need to explain it to the audit committee." The next day, we did. The committee members were predictably cranky, but after some discussion, they agreed that the issuance of the financial statements and the audit report should wait for the research on this item. Two days passed. The targeted report date had been missed. The next day, the CFO's assistant called and asked us to come up to his office. When we arrived in his office, the CFO was with the head of HR. Both looked serious. "Well," he said, looking the audit partner straight in the eye and reaching out to offer him a firm handshake, "I guess I owe you an apology. Both of you, in fact." He continued, "We've discovered an embezzlement. Been going on several years. That reconciling item was being used to cover it. Our control process broke down and we did not catch it. Without you, our auditors, pushing us, we'd never have spotted it." My client contact - the woman who had ignored my original requests for documentation had just been arrested for the embezzlement. She was escorted from the building in police custody. Case Study B Data Analytics and a Skeptical Mindset Without any explanation about why the number of days in A/R remained consistent but the balance had increased, I was even more skeptical of the reasons behind the increase in the allowance. After discussions with engagement management, we adjusted our risk assessment, classifying the risk of material misstatement as a fraud risk and a significant risk, and tailored our audit procedures as appropriate to respond to this increased risk level. We ultimately were able to determine that senior management had been overstating the allowance for doubtful accounts by immaterial amounts for some time, with the apparent intention of reversing it when the new contract went into effect to boost its financial performance. The use of data analytics played a valuable part in helping us uncover the unusual activity, and by exercising professional skepticism, I was able to validate the findings. This experience reminded me that it is important to think critically about the results that data analytics provide and not just focus on confirming information. It is also important that I maintain a skeptical mindset and remain steadfast in seeking answers when results indicate something may be amiss. Case Study C - Influenced by Incentives? Understanding the risk, I discussed the company's compensation and performance management process with my manager. We agreed on the significance of the risk and concluded that the compensation and bonus structure for the tax manager presented a potential fraud scheme whereby the tax manager had an incentive, pressure, and the opportunity to potentially manipulate the company's books and records to achieve the targeted effective tax rate. We tactfully discussed our concerns about the risk with the tax manager. She told us she was somewhat offended by the implication that she would consider manipulating information to achieve a desired result for the company or for herself. As the most junior person in the room, I was nervous as we laid out our concerns, but my manager backed me up 100 percent as I explained. We then met with the chief accounting officer, who agreed with our concerns and conclusion about the presence of an incentive, pressure, and opportunity to potentially commit fraud on the part of the tax manager, due to the structure of her compensation and bonus plan. In the end, this experience reminded me how important it is to use critical thinking even before we start testing and how essential the risk assessment process is to the audit. In this case, one risk assessment finding simultaneously increased the extent of substantive testing and internal controls testing performed by the engagement team Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cloud Computing Data Auditing Algorithm

Authors: Manjur Kolhar, Abdalla Alameen, Bhawna Dhupia, Sadia Rubab, Mujthaba Gulam

1st Edition