Answered step by step

Verified Expert Solution

Question

1 Approved Answer

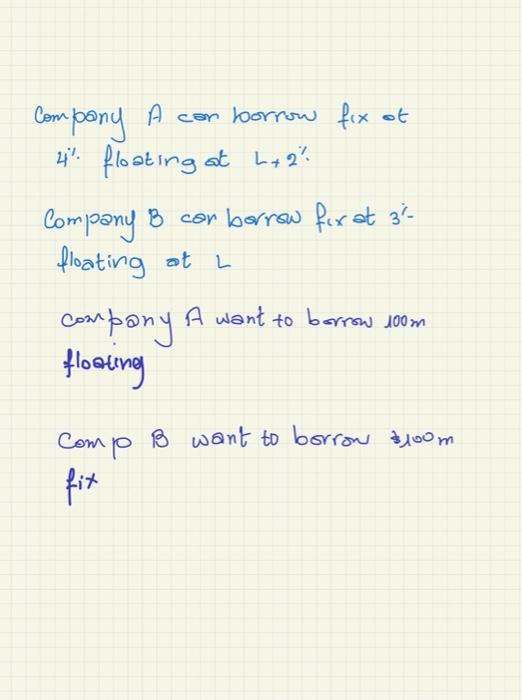

risk management ompany A con borrow fix ot 4. floating at h+2 Company B can borrow for at 3% floating at L Company floating A

risk management

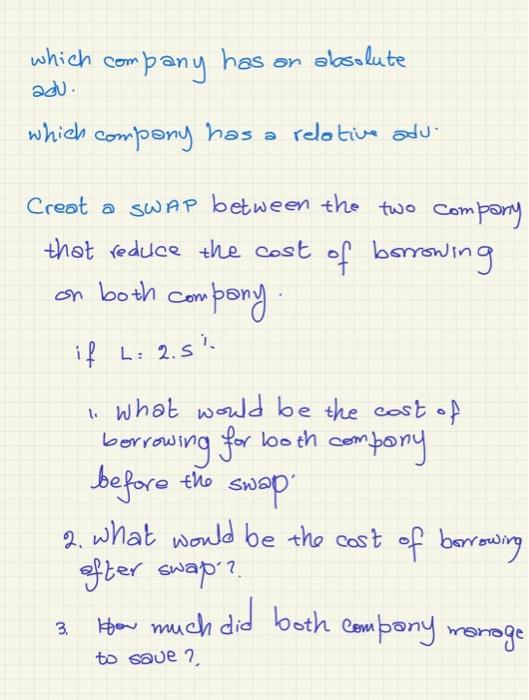

ompany A con borrow fix ot 4. floating at h+2 Company B can borrow for at 3% floating at L Company floating A want to borrow 100m Comp B want to borrow $100m fix which com company adu has an absolute which company has a relative adu. Creat a swap between the two com! company that reduce the cost of borrowing on both com company if : 2.si 1. What would be the cast of borrowing for both company before the swap 2, what would be the cost of borrowing after swap? How much did both company manage 3. to save Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction To Derivatives And Risk Management

Authors: Robert Brooks, Don M Chance, Roberts Brooks

8th Edition

0324601212, 9780324601213