Answered step by step

Verified Expert Solution

Question

1 Approved Answer

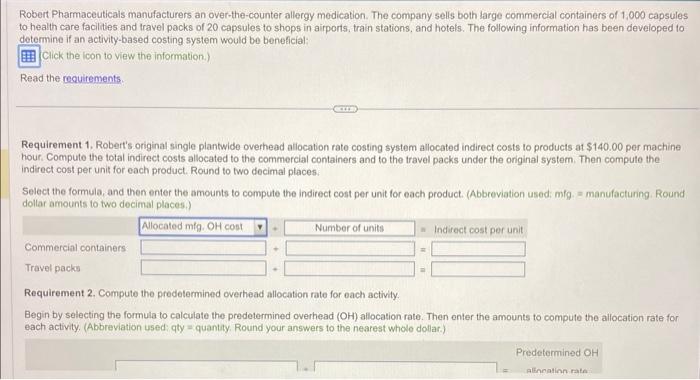

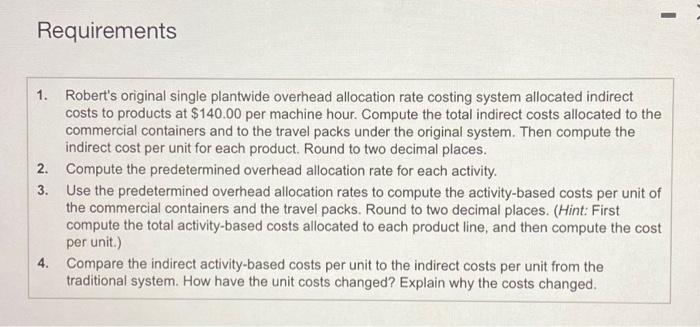

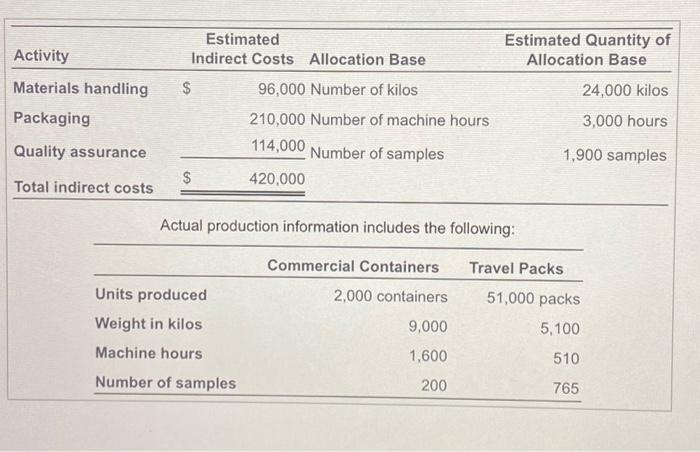

Robert Pharmaceuticals manufacturers an over-the-counter allergy medication. The company sells both large commerctal containers of 1,000 capsules to health care facilties and travel packs of

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Rethinking Audit Cultures ACritical Look At Evidence Based Practice In Psychotherapy And Beyond

Authors: Lucy King

1st Edition

1906254311, 978-1906254315