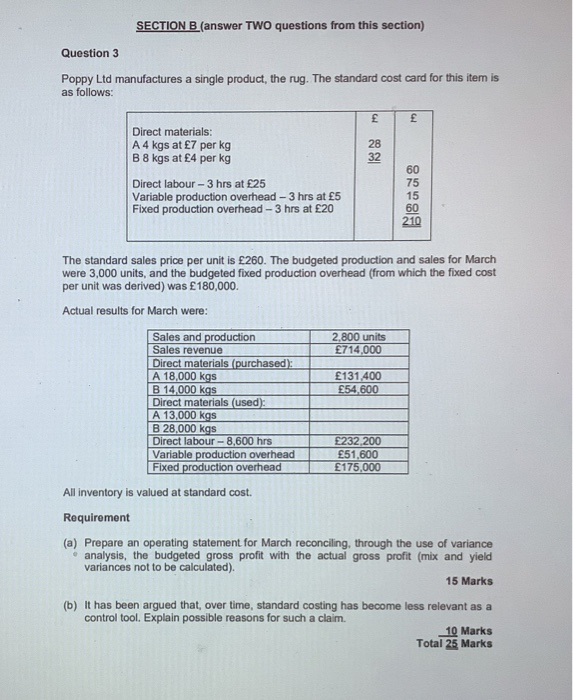

SECTION B (answer TWO questions from this section) Question 3 Poppy Ltd manufactures a single product, the rug. The standard cost card for this item is as follows: 28 32 Direct materials: A4 kgs at 7 per kg B 8 kgs at 4 per kg Direct labour - 3 hrs at 25 Variable production overhead - 3 hrs at 5 Fixed production overhead - 3 hrs at 20 60 75 15 60 210 The standard sales price per unit is 260. The budgeted production and sales for March were 3,000 units, and the budgeted fixed production overhead (from which the fixed cost per unit was derived) was 180,000. Actual results for March were: Sales and production 2,800 units Sales revenue 714,000 Direct materials (purchased): A 18,000 kgs 131,400 B 14,000 kgs 54,600 Direct materials (used): A 13,000 kgs B 28.000 kgs Direct labour -8,600 hrs 232,200 Variable production overhead 51,600 Fixed production overhead 175,000 All inventory is valued at standard cost. Requirement (a) Prepare an operating statement for March reconciling, through the use of variance analysis, the budgeted gross profit with the actual gross profit (mix and yield variances not to be calculated). 15 Marks (b) It has been argued that, over time, standard costing has become less relevant as a control tool. Explain possible reasons for such a claim. 10 Marks Total 25 Marks SECTION B (answer TWO questions from this section) Question 3 Poppy Ltd manufactures a single product, the rug. The standard cost card for this item is as follows: 28 32 Direct materials: A4 kgs at 7 per kg B 8 kgs at 4 per kg Direct labour - 3 hrs at 25 Variable production overhead - 3 hrs at 5 Fixed production overhead - 3 hrs at 20 60 75 15 60 210 The standard sales price per unit is 260. The budgeted production and sales for March were 3,000 units, and the budgeted fixed production overhead (from which the fixed cost per unit was derived) was 180,000. Actual results for March were: Sales and production 2,800 units Sales revenue 714,000 Direct materials (purchased): A 18,000 kgs 131,400 B 14,000 kgs 54,600 Direct materials (used): A 13,000 kgs B 28.000 kgs Direct labour -8,600 hrs 232,200 Variable production overhead 51,600 Fixed production overhead 175,000 All inventory is valued at standard cost. Requirement (a) Prepare an operating statement for March reconciling, through the use of variance analysis, the budgeted gross profit with the actual gross profit (mix and yield variances not to be calculated). 15 Marks (b) It has been argued that, over time, standard costing has become less relevant as a control tool. Explain possible reasons for such a claim. 10 Marks Total 25 Marks