Answered step by step

Verified Expert Solution

Question

1 Approved Answer

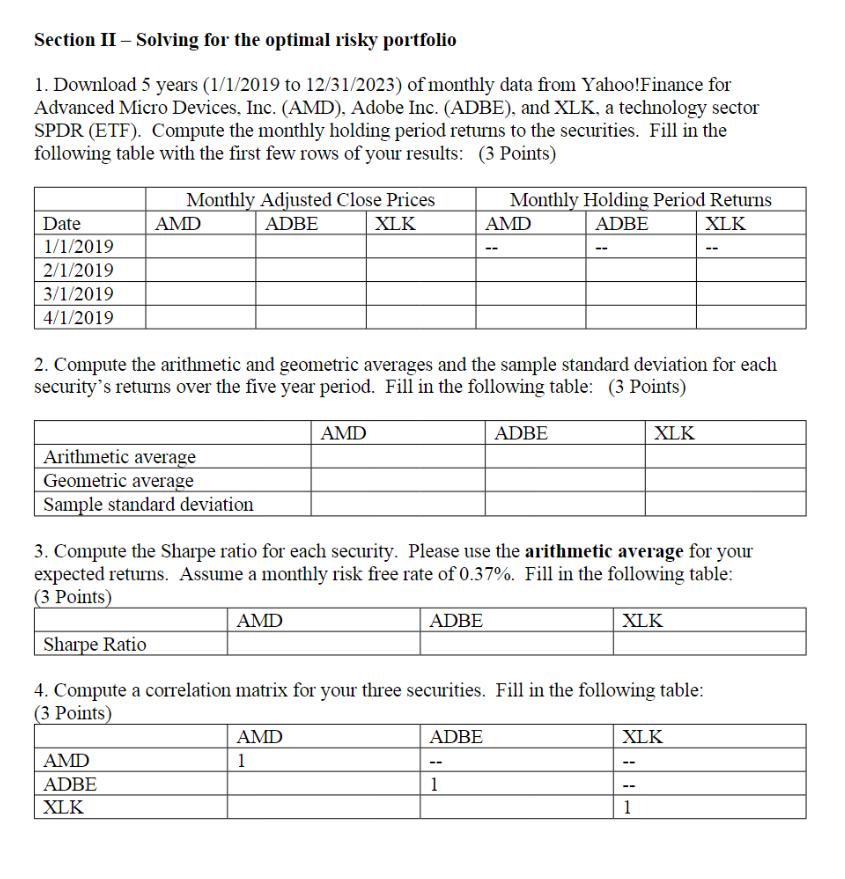

Section II - Solving for the optimal risky portfolioSection II - Solving for the optimal risky portfolio Download 5 years ( 1 / 1 /

Section II Solving for the optimal risky portfolioSection II Solving for the optimal risky portfolio

Download years to of monthly data from Yahoo!Finance for

Advanced Micro Devices, Inc. AMD Adobe Inc. ADBE and XLK a technology sector

SPDR ETF Compute the monthly holding period returns to the securities Fill in the

following table with the first few rows of your results: Points

Compute the arithmetic and geometric averages and the sample standard deviation for each

securitys returns over the five year period. Fill in the following table: Points

Compute the Sharpe ratio for each security. Please use the arithmetic average for your

expected returns. Assume a monthly risk free rate of Fill in the following table:

Points

Compute a correlation matrix for your three securities Fill in the following table:

Points

Download years to of monthly data from Yahoo!Finance for

Advanced Micro Devices, Inc. AMD Adobe Inc. ADBE and XLK a technology sector

SPDR ETF Compute the monthly holding period returns to the securities Fill in the

following table with the first few rows of your results: Points

Compute the arithmetic and geometric averages and the sample standard deviation for each

securitys returns over the five year period. Fill in the following table: Points

Compute the Sharpe ratio for each security. Please use the arithmetic average for your

expected returns. Assume a monthly risk free rate of Fill in the following table:

Points

Compute a correlation matrix for your three securities Fill in the following table:

Points

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Oxford Handbook Of Entrepreneurial Finance

Authors: Douglas Cumming

1st Edition

0195391241, 978-0195391244