Answered step by step

Verified Expert Solution

Question

1 Approved Answer

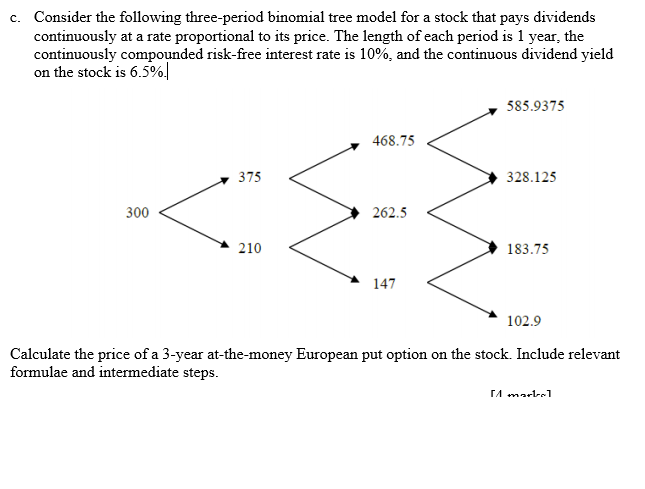

Show all the steps with formula please c. Consider the following three-period binomial tree model for a stock that pays dividends continuously at a rate

Show all the steps with formula please

c. Consider the following three-period binomial tree model for a stock that pays dividends continuously at a rate proportional to its price. The length of each period is 1 year, the continuously compounded risk-free interest rate is 10%, and the continuous dividend yield on the stock is 6.5%. 585.9375 468.75 M 375 328.125 300 262.5 210 183.75 147 102.9 Calculate the price of a 3-year at-the-money European put option on the stock. Include relevant formulae and intermediate steps. 11 mart 1Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Health Care Finance Basic Tools For Nonfinancial Managers

Authors: Judith J. Baker, R.W. Baker, Neil R. Dworkin

5th Edition

1284118215, 978-1284118216