Answered step by step

Verified Expert Solution

Question

1 Approved Answer

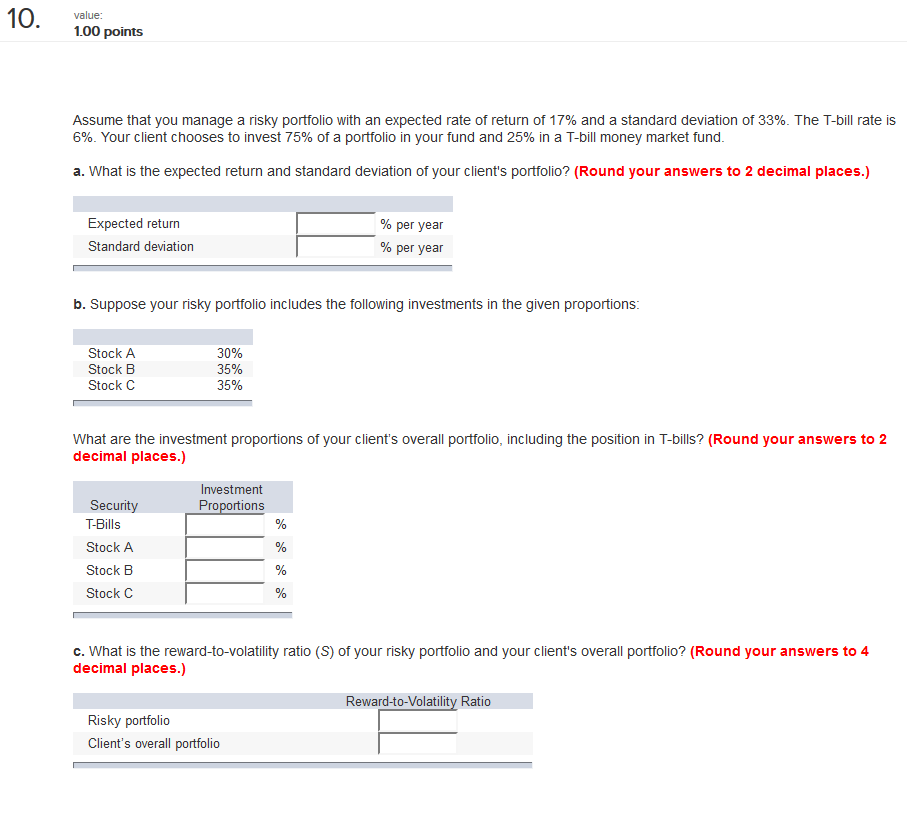

Show all work please. 10. value: 1.00 points Assume that you manage a risky portfolio with an expected rate of return of 17% and a

Show all work please.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options Trading 12 Books In 1 Elevate Your Profits Erase Risks The Definitive Guide From Rookie To Top 1 Trader

Authors: Warren Ray Benjamin

1st Edition

979-8860106413