Answered step by step

Verified Expert Solution

Question

1 Approved Answer

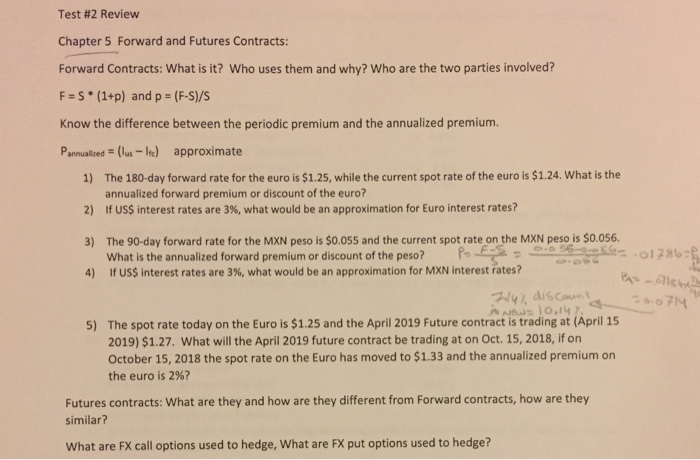

Show calculation Test #2 Review Chapter 5 Forward and Futures Contracts: Forward Contracts: What is it? Who uses them and why? Who are the two

Show calculation

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Impact Investing Instruments Mechanisms And Actors

Authors: Wolfgang Spiess-Knafl Barbara Scheck

1st Edition

3319665553,3319665561