Question: Show that B is priced according to the CAPM. b) Suppose the risk-free rate is 5%. How much of security F is included in the

Show that B is priced according to the CAPM.

b) Suppose the risk-free rate is 5%. How much of security F is included in the market portfolio M? Briefly explain.

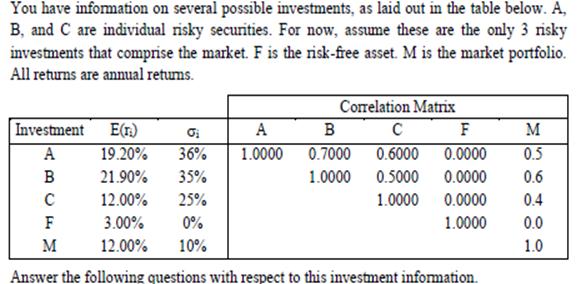

You have information on several possible investments, as laid out in the table below. A, B, and C are individual risky securities. For now, assume these are the only 3 risky investments that comprise the market. F is the risk-free asset. M is the market portfolio. All returns are annual returns. Investment E(r) A B C F M Correlation Matrix C 0.6000 1.0000 0.5000 1.0000 A B 1.0000 0.7000 F 0.0000 0.0000 0.0000 1.0000 19.20% 36% 21.90% 35% 12.00% 25% 0% 3.00% 12.00% 10% Answer the following questions with respect to this investment information. M 0.5 0.6 0.4 0.0 1.0

Step by Step Solution

3.53 Rating (160 Votes )

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts