Answered step by step

Verified Expert Solution

Question

1 Approved Answer

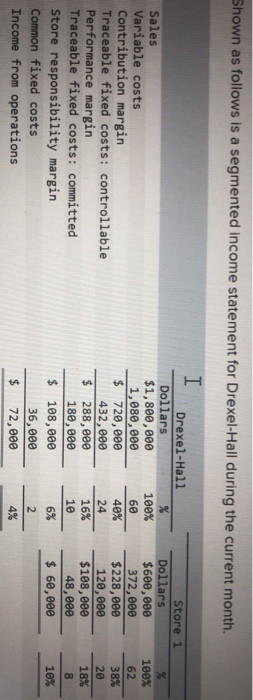

Shown as follows is a segmented income statement for Drexel-Hall during the current month. I 100% 62 38% Store 1 Dollars $600,000 372,000 $228,000 120,000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Frauds Of The Past Lessons For The Future A Student Led Journey Through The World Of Auditing

Authors: Dr. Manjari Sharma, Mr. Pragadeesh SP, Mr. Sivanaresh A

1st Edition

B0CGKRP289, 978-6206753247